The capacity to self-custody cryptocurrencies generates an immeasurable opportunity for current, and potential market participants.

Through the removal of intermediaries, access to this section of capital markets is granted to anyone with a working internet connection, and some spare change.

Transaction costs are lower, product offerings will soon be broader, and markets can be more efficient and operate 24/7.

Whilst all of these factors contribute towards the valuation of the cryptocurrency industry, many investors do not care about the functional benefits of such an ecosystem, and merely want investment exposure to the asset class in the hopes of making capital returns.

This is understandable as the opposite side of the equation is increased levels of individual responsibility, where an estimated 2.78 million – 3.79 million Bitcoin (around a 5th of total supply) are estimated to have been lost by users, according to a study conducted by Chainalysis.

Luckily for investors, the space for managed cryptocurrency investment exposures is broadening, enabling inclusion of these products within more traditional investment platforms – like Mason Stevens.

Within our morning note series, we’ve canvassed a series of topics within the industry and the broader Web 3.0 space, including:

- Role of cryptocurrencies within investment portfolios

- 2022 market outlook

- The Metaverse

- Web 3.0

- Cryptocurrency regulation

- Centralised cryptocurrency exchanges

- Decentralised cryptocurrency exchanges

- Bitcoin and ESG

- Blockchain

- Basics of cryptocurrency (part 1, part 2)

As the topic of today’s note, we will discuss the ways in which investors can gain exposure to the cryptocurrencies through traditional investment platforms – like Mason Stevens.

Exchange Traded Funds (ETF’s)

Over the past two years, the growing acceptance from regulators has led to the emergence of several ETF’s which offer exposure to cryptocurrencies.

When we look at the available ETF’s, we can separate them into two buckets.

Spot based ETF’s

Several countries around the world have approved spot Bitcoin/Ethereum ETF’s in the past 2 years.

This is important, as spot ETF’s are required to hold the underlying asset – as opposed to futures ETF’s which only hold the futures contracts of the underlying asset (and are therefore subject to higher transaction costs, and decay due to contango).

As a result, spot ETF’s serve as the most efficient means of gaining direct cryptocurrency exposure in the market – given they will most closely track the underlying price of their respective cryptocurrency.

The most liquid of the spot cryptocurrency ETF’s are in Canada, where several options are available (FUM levels and MER’s may not necessarily be aligned, where the most capital has flowed to those who entered the market first):

| Name | Exchange | Ticker | MER | FUM ($, CAD), as of 11-Feb-22 |

| Purpose Bitcoin ETF | TSX | BTCC | 1.0% | 1.49bn |

| 3iQ CoinShares Bitcoin ETF | TSX | BTCQ | 1.0% | 1.13bn |

| Evolve Bitcoin ETF | TSX | EBIT | 0.75% | 133m |

| CI Galaxy Bitcoin ETF | TSX | BTCX | 0.4% | 495.2m |

| Fidelity Advantage Bitcoin ETF | TSX | FBTC | 0.4% | 30.8m |

| Name | Exchange | Ticker | MER | FUM ($, CAD), as of 11-Feb-22 |

| Purpose Ethereum ETF | TSX | ETHH | 1.0% | 396.6m |

| 3iQ CoinShares Ethereum ETF | TSX | ETHQ | 1.0% | 350.4m |

| Evolve Ethereum ETF | TSX | ETHR | 0.75% | 77.6m |

| CI Galaxy Bitcoin ETF | TSX | ETHX | 0.4% | 1.02b |

Futures based ETF’s

Several Bitcoin ETF’s were released in the US last year after the SEC finally granted approval after a years long process involving multiple applications from ETF providers.

However, the SEC were only willing to approve ETF’s which invest in Bitcoin futures – given they do not have oversight over spot Bitcoin markets (which they believe are vulnerable to manipulation).

The approved Bitcoin ETF’s are only able to source Bitcoin futures contracts from the Chicago Mercantile Exchange – where the CFTC has regulatory oversight.

Futures ETF’s are only appropriate in situations where it is not viable for the ETF provider to take physical delivery of the underlying asset – like oil.

For Bitcoin, such an arrangement means that investors will be exposed to the negative aspects of futures exposures – where they will likely underperform their spot based counterparts to the degree of 5-10%.

This underperformance is a result of the requirement of ETF providers to roll the longer dated futures contracts they hold (incurring transaction costs), whilst also historically trading at premiums to spot prices (also known as “contango”).

This arrangement will result in a sub-optimal outcome for investors, but will beneficial for the hedge funds who will be able to arbitrage the premium.

Indirect cryptocurrency ETF exposures

Investors also have access to ETF’s which offer exposure to securities which operate within the cryptocurrency industry – including cryptocurrency exchanges, Bitcoin miners, and other cryptocurrency service providers.

These ETF’s offer a more diversified exposure to the industry (but still remain strongly correlated to cryptocurrency prices).

Given the constrained universe of direct equity exposures, the underlying assets of each of these ETF’s are very similar – with differences primarily arising from whether or not these ETF’s allocate partially to direct cryptocurrency exposures, as well as the exchange (and therefore currency) investors can access them through.

| Name | Exchange | Ticker | MER | Direct Crypto Exposure? | FUM, as of 11-Feb-22 |

| Bitwise Crypto Industry Innovators ETF* | NYSEARCA | BITQ | 0.85% | No | $120m (USD) |

| Invesco Alerian Galaxy Crypto Economy ETF | NYSEARCA | SATO | 0.60% | Yes | $8.6m (USD) |

| Betashares Crypto Innovators ETF* | ASX | CRYP | 0.67% | No | $120.8m (AUD) |

| Cosmos Global Digital Miners Access ETF | CXA | DIGA | 0.9% | No | $2.4m (AUD) |

*BITQ and CRYP follow the same index

Source: Bloomberg

Listed Investment Trusts

Before the approval of Bitcoin and Ethereum spot ETF’s, Grayscale’s trusts acted as one of the only ways to gain exposure to cryptocurrency within listed securities markets – with the majority of AUM held in Bitcoin (GBTC) and Ethereum (ETHE) trusts.

They were able to play this role since their inception in 2013, through taking advantage of a loophole in US securities law and acting as a “side-door ETF”, creating new shares funded by accredited investors, who were then able to float these shares on OTC markets after a six month seasoning period (enabled through Rule 144).

However, unlike a traditional ETF model, there is no redemption mechanism to convert the shares back into cryptocurrencies – it is all one-way flow.

As a result, the price of Grayscale’s trusts is able to operate at a discount/premium to NAV – where the level of this discount/premium is determined by market demand.

When there were no other alternatives in the market, these products traded at healthy premiums given strong demand and the 6-month delay in adding more units – even reaching beyond 120% at times.

Hedge funds were able to profit handsomely from this fact through their role as accredited investors – creating shares in GBTC and ETHE, hedging their positions, and picking up the 10-120% premium 6 months after their investment.

However, once cheaper alternatives entered the market (where GBTC has a MER of 2% and ETHE has a MER of 2.5%), investors sought to allocate their capital elsewhere and subsequently reduced the upward pressure on the premium.

On top of this, hedge funds who were still within the 6-month seasoning period had excess shares to sell – adding unwanted supply to the market.

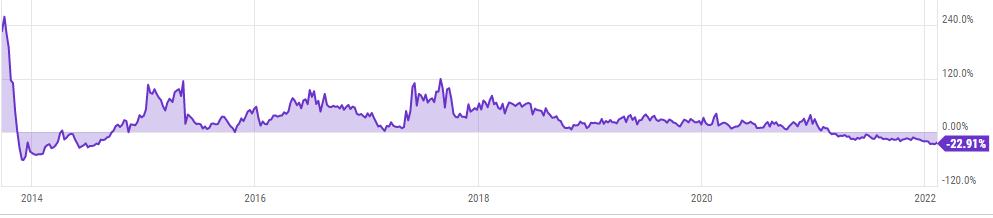

As a result, both trusts are now trading at heavy discounts to NAV, with GBTC trading at a 22.91% discount to NAV, and ETHE at a discount of 16.11% as of the 9th of February 2021.

Chart 1: GBTC discount/premium to NAV (as at 9-Feb-22)

Source: Ycharts

Chart 2: ETHE discount/premium to NAV (as at 9-Feb-22)

Source: Ycharts

Given both trusts make up the majority of the market, with GBTC’s AUM of USD$28.4bn and ETHE’s AUM of USD$9.7bn, the required demand to return to these Fund’s back to parity is unlikely to eventuate organically.

The only way in which they would return to parity would be if Grayscale conducted a redemption of shares (unlikely given their loss of revenue), or if they were successfully converted into ETF’s (Grayscale has lodged applications, but the view of many market participants is that this is unlikely to occur until 2023 or even beyond).

Therefore, an investment into these listed trusts (which have been the primary way for the majority of market participants to gain access) must consider these factors, where the discount to NAV can be viewed as both an investment opportunity, or a point of potential further underperformance.

Managed Funds

As investor demand has increased, so has the range of available products – with a plethora of cryptocurrency managed funds entering the market.

These managed fund structures are often inferior to listed ETF’s in passive investment strategies, due to reduced liquidity and increased security concerns (owing to reduced capacity to invest into appropriate infrastructure).

For investors who may be restricted to managed funds or AUD denominated investments, we offer the Monochrome Bitcoin Fund, which aims to solely track the price of Bitcoin with institutional grade custody and insurance policies.

Managed fund structures will also offer opportunities in the years to come, as investors seek to capture alpha in their investments and be exposed to more active portfolio management strategies.

Direct Equities

Finally, investors can access the cryptocurrency industry through direct equity investments.

These investments offer exposure to revenue generating companies in the industry, like cryptocurrency exchanges (NASDAQ: COIN), miners (NASDAQ: MARA), (NASDAQ: RIOT), (TSE: HUT), and cryptocurrency service providers (NYSE: SI), (TSE: GLXY).

It must be noted that these companies maintain strong correlations to underlying cryptocurrency prices, with some even housing significant amounts of cryptocurrencies on their balance sheet.

A Diversified and Balanced Approach

Whilst the investable universe of cryptocurrency related securities has grown over the past few years, investors must still take caution in selecting their exposures.

The cryptocurrency industry is still highly volatile and will likely continue to be for the years to come due to the fact that many cryptocurrencies still remain within price discovery phases.

The selection of investment exposures/vehicles should be scrutinised to a greater deal due to this volatility, as the scope of potential losses is far greater than most other securities.

However, the amount of attention given to the industry by notable investors/institutions should not be ignored, where a consideration of adding investment exposures should become more commonplace within asset allocation discussions.

Should you have any further questions or require any assistance in selecting the appropriate exposures, please reach out to your Mason Stevens representative.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.