Capital markets exist to improve transactional efficiency, providing a venue to allow the transfer of capital between those who possess it, and those who demand it.

They serve a critical role, acting as a link between savers and investors, facilitating the economic growth which determines our relative levels of prosperity.

Their efficiencies are most commonly demonstrated through equity markets, where individuals and institutions can purchase a share of a company’s future earnings, in exchange for providing that company with capital to grow their business further, or to sustain existing business activities.

Whilst capital markets have enabled economic advancements which have significantly enhanced our standard of living, they aren’t perfect, requiring a multitude of investment bankers getting paid well above their productive contribution, and countless other front, middle and back-office staff to merely keep the system functioning.

Errors are commonplace, none more so than Citi’s USD$900m transfer gaffe to Revlon bondholders, and social outcomes are inequitable, exacerbating the already lopsided distribution of wealth in our society: with over 1.7 billion people remaining unbanked as of 2017 due to the significant barriers of entry into the financial services industry.

At the core of it, the problem lies in the trust required in intermediaries, who are often inefficient, prone to error and each carry a set of often exclusionary company policies required to ensure the maximisation of shareholder value (further enforcing wealth inequality).

Enter decentralised finance (also referred to as “DeFi”) to address this issue.

DeFi proposes to reinvent the financial system, replacing the need for intermediaries, and providing a means to facilitate the transfer of capital between individuals and institutions, in a trustless, efficient and secure manner.

In today’s note, we will examine the concept of decentralised finance – what exactly it is, how it can be used, and the way in which it can be assimilated into the future of financial markets.

Decentralised Finance (“DeFi”)

Earlier, I mentioned that DeFi was “trustless”, but what exactly does this mean?

In current centralised finance models (also referred to as “CeFi”), transactions require a trusted third party, who act as a bridge to facilitate transactions between two parties.

DeFi requires no such intermediary, enabling two parties to transact, who don’t know,or trust each other – hence it is trustless, as it removes this requirement of trust between multiple parties.

It operates on the blockchain, replacing intermediaries with smart contracts – which are self-executing contracts with terms and conditions written into their code.

Whilst we wont go into further detail on blockchain and cryptocurrencies in general, it is a topic we have touched on in the past, here, here and here.

How Does It Work?

An easy way to view the usefulness of DeFi is through looking at the act of borrowing and lending money through Aave – a leading DeFi protocol.

Aave facilitates borrowing and lending between individuals and institutions through a liquidity pool-based strategy, where rates of borrowing and lending between participants are determined by the relative amount of available liquidity in the pool.

Source: deFi.cx

In order to borrow, investors must first deposit their chosen collateral. In this example, we will deposit Ethereum (ETH), which currently has a loan to value (LVR) ratio of 80%, and we will use this collateral to borrow Tether (USDT).

USDT is a USD backed stablecoin, where each USDT token is pegged to the US dollar (where 1 USDT = 1 USD). The value of USDT is able to be pegged, given its issuer, Tether Limited, keeps 1 USD in custody for every token issued.

As of the writing of this note, investors can lend USDT to the liquidity pool at a rate of 2.97% p.a., or borrow at a rate of 3.77% p.a.

These borrowing and lending rates are determined by supply and demand, with rates going up or down according to the amount of available liquidity in the pool.

i.e. if 90% of the pool is being lent out, then borrowing rates will increase to incentivise existing debtors to repay debts, or disincentivise new investors from borrowing from the liquidity pool.

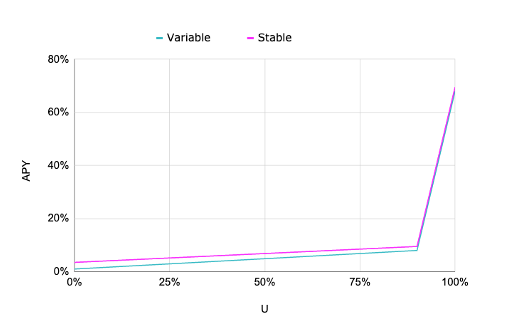

The relationship between existing available liquidity and interest rates is determined by the utilisation rate, which reflects the proportion of the liquidity pool which has been lent out.

Each cryptocurrency has a predetermined optimal utilisation, which in the case of USDT on Aave is 90%.

In the below graph, the relationship between utilisation (U) and the interest rate (APY) is relatively stable until it reaches its optimal utilisation rate.

Once it reaches this point, it increases significantly, given the suboptimal outcomes for borrowers and lenders should the utilisation rate approach 100%.

Source: Aave

Now if we step back into centralised financial models, we can look at the relative rates offering for borrowing and lending over the same 1-year period.

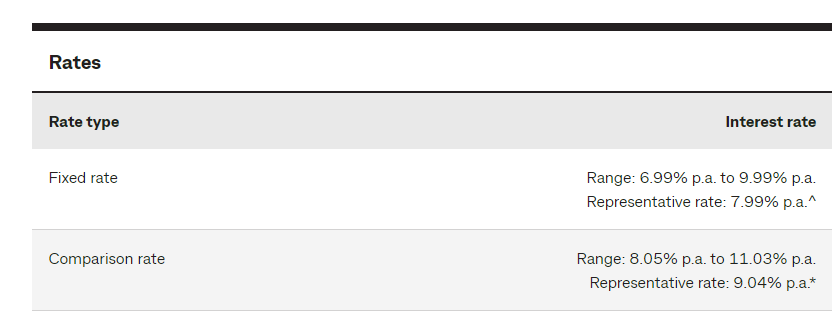

If I wanted to take out a secured automobile loan with CBA, I would be subject to paying between 6.99%-9.99% p.a.

Whilst one could get much lower rates through banker relationships, you would be hard pressed to be able to find a 1-year loan available for under the 3.77% p.a. offered on Aave.

Source: CBA

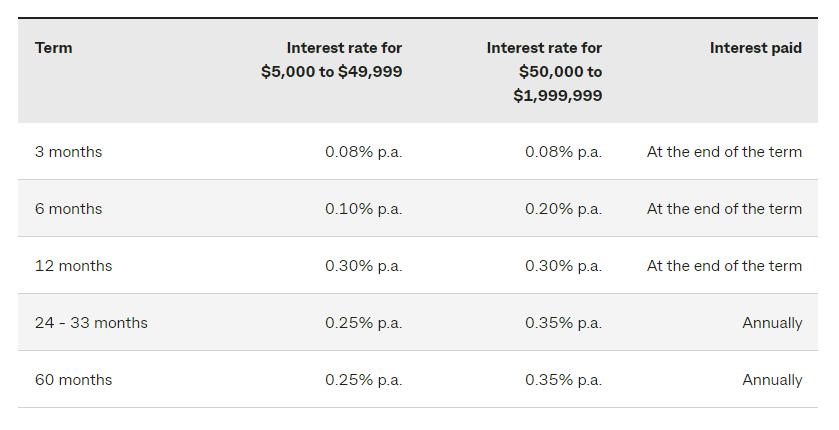

Similarly, if I wanted to be able to deposit money for 1 year – I would only be able to earn 0.30% over that same 1-year period, or potentially more with certain promotional offers made through savings accounts (which are subject to deposit limits and largely unavailable for significant balances).

Source: CBA

You might say that you would prefer to pay more/earn less given the reputation of CBA, where the government has an implicit guarantee on any deposits up to $250,000, however many other countries don’t afford this level of protection.

Moreover, there is no real counterparty risk with Aave – it is a decentralised protocol with no single point of failure, where transactions are governed purely by the lines of code written into smart contracts. It merely facilitates borrowing and lending between market participants, has no significant overhead costs, and is scalable.

It can offer better rates than centralised alternatives, given there is no intermediary which needs to take a spread of any borrowing/lending to account for risks, or pay for the costs of operating a bank.

Whilst this example may be slightly misaligned (given we have borrowed in USD, and lent in AUD), similar rates can be achieved through employing FX hedging on other decentralised derivatives platforms, or such a time in the future where AUD stablecoins have more liquidity.

What Can Be Decentralised?

Over USD$56bn is currently locked into a range of DeFi protocols, providing borrowing/lending services, decentralised cryptocurrency exchanges, insurance, payment networks and derivatives protocols.

Most relevant to our dealing within equity, FX and fixed income markets is Synthetix – a DeFi protocol which facilitates a decentralised exchange and provides synthetic asset issuance services.

Started by Australia’s own Kain Warwick, the protocol is the largest of its kind, and offers insight as to what one instance of blockchain integration into capital markets could look like.

Users are able to create and trade synthetic tokens which track the real-life price of assets – including a multitude of currencies (both fiat and cryptocurrency), gold, silver and more recently, equities like Apple and Tesla.

There is no underlying asset, so investors aren’t able to vote or receive dividends, however prices are accurate and provided by decentralised data services.

The value it offers is in its 24/7 markets with instant settlement, for a fraction of the cost of traditional markets given the lack of human input required.

Whilst Mason Stevens is unique in its offering across all equity, credit and FX markets, a regular investor would also find it hard pressed to invest into options beyond popular equity exchanges in Australia and the US, with limited scope to invest into currencies and more niche asset classes/geographies.

Is Decentralisation A Good Thing?

If regulators have found it hard dealing with concepts like Buy Now Pay Later, they will have a mountain to climb when it comes to attempting to regulate DeFi.

Historical regulatory models used for financial transactions primarily rely on the presence of an intermediary, for which there is none to regulate.

The anonymity of transactions and governance structures (where some protocols like Maker DAO implement changes proposed and voted on by token holders) also poses further questions, clouding the question of who and what to regulate.

Consumers are not granted the protections they are historically afforded, and little recourse is available should a client enter into a disadvantageous transaction.

However, the benefits of such a system are clear – significantly increased access to global capital markets, little barriers to entry (you only require an internet connection and capital), more competitive transactions, improved market efficiency, lower costs and higher levels of transparency.

Despite a 50% drawdown in the cryptocurrency market in recent months, the lack of disruption to the DeFi ecosystem highlighted the value which it can add, perfectly summarised by Cathie Wood:

“Can you imagine if equity and bond prices were cut in half?… I think we would be in a counterparty risk situation”

Growth prospects lie in more widespread adoption, which will require considerable levels of education, and also within the ability of Bitcoin to integrate smart contract technology through layer two protocols that would enable usage within the DeFi ecosystem.

Given their ability to boost standards of living and increase economic prosperity, capital markets will always continue to evolve as new technology sees the light of day.

Whilst we may not see DeFi in existence in 10-20 years time, it is almost guaranteed that its underlying processes will be integrated into traditional markets in some form.

As such, even if you do not believe in DeFi or cryptocurrencies in general, it is important to be aware of the innovations which will shape the financial systems of our future.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.