By now, we are all used to hearing the same old stories – growing COVID-19 infections, the U.S. government’s newest stimulus bill, and the price of Bitcoin going up.

Whilst cryptocurrencies have been around for 10 years, several structural tailwinds have driven their meteoric rise over the past year.

These structural tailwinds – which have driven cryptocurrencies into mainstream financial markets – have been primarily centred around Bitcoin as a “digital gold”, provision of cryptocurrency related financial services, addition to corporate balance sheets, and inclusion in institutional investment mandates.

In the final note of a 3-part cryptocurrency series (see Part 1 and Part 2 to gain a better idea of the underlying technology), we will take you through the narratives which have driven valuations, and the landscape for investors wishing to add exposure to their portfolio.

Bitcoin as “digital gold”

2020 saw unprecedented amounts of monetary and fiscal stimulus in response to the COVID-19 pandemic, with investors worrying about inflation for the first time in many years.

These concerns drove investors towards inflation hedges – assets which maintain their purchasing power in inflationary environments.

For many investors in years gone past, such an allocation would involve the purchase of gold, given its scarcity and worldwide reputation as a store of value asset.

However, more and more investors have used Bitcoin as an alternative to gold, driving Bitcoin’s investment narrative towards acting as “digital gold”, as opposed to its capabilities as a global medium of exchange. This narrative shift has been driven by its store of value characteristics, which surpass gold from a technical standpoint – serving as a more portable, accessible and divisible asset.

Bitcoin can be held by anyone with a working internet connection, transferred around the world within seconds, and divided into one millionth of itself (also known as a “satoshi”).

On the other hand, gold is costly to store (requiring secure premises), and difficult to transact in small quantities.

This shift in narrative saw significant fund inflows into Bitcoin, adding credence to the whole industry, and providing greater exposure to other major cryptocurrencies such as Ethereum and Cardano.

Provision of cryptocurrency financial services

As it has become increasingly likely that cryptocurrencies will play a role in financial markets in the future, institutions have begun providing related financial services.

BNY Mellon, the world’s largest custody bank, announced in February of 2021 that they will provide custodial services for cryptocurrencies, with Deutsche Bank signalling their intentions to do so as well. Both announcements will open up institutional investment and provide greater legitimacy to the industry, through the greater trust investors have in these reputable institutions.

Payment platforms have also come to the party, with Paypal (NASDAQ: PYPL) announcing their provision of a custody solution, and integration into their payment networks, allowing their 286 million U.S. users to transact with up to 26 million merchants using select major cryptocurrencies. Paypal have also been actively seeking to expand their range of services and the geographies in which they are available, reportedly attempting to purchase Curv – a digital asset custody specialist. If Paypal is successful, we will likely see one of the first of many instances of global corporations purchasing cryptocurrency technology firms in a bid to fast-track the development of related services.

Mastercard (NYSE: MA) have also announced the plans to integrate major cryptocurrencies into their payment networks, with Visa (NYSE: V) indicating they will follow suit.

Addition of cryptocurrencies to corporate balance sheets

The last 12 months has also seen the addition of Bitcoin onto corporate balance sheets – a move pushed by its aforementioned store of value characteristics.

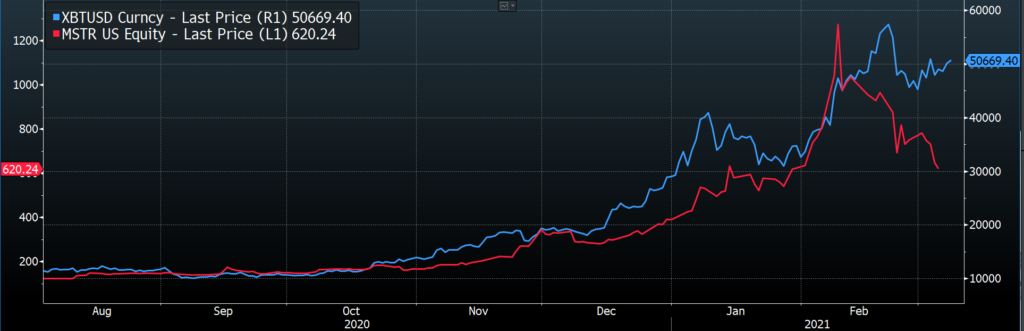

Major listed corporations such as Tesla (NASDAQ: TSLA), Microstrategy (NASDAQ: MSTR) and Square (NYSE: SQ) have all added Bitcoin to their balance sheet as an alternative to cash. This has brought attention to the space and provided more legitimacy for the industry given the material investments made by these institutions.

Whilst some of this decision making has been irresponsible – with Microstrategy even issuing convertible notes to purchase more Bitcoin, it represents a significant mentality shift towards cryptocurrency as a legitimate asset class.

Institutional inclusion of cryptocurrencies into investment mandates

In light of increased investor interest, institutions have begun to add cryptocurrencies into their investment mandates, ranging from life insurers such as MassMutual, to asset managers such as Blackrock, Ruffer and Guggenheim.

In previous years, such an inclusion would be hamstrung by public perception and regulatory hurdles, supporting the categorisation of cryptocurrencies as a new asset class in financial markets.

Cryptocurrencies will continue to become more relevant should they continue their integration into the global economy. Institutional take-up will continue to serve as the driving force behind valuations, given their key role in bringing cryptocurrency to the mainstream.

Methods of Investing

Now the most interesting part – how to get exposure.

There are a number of vehicles which can be used to get direct exposure to cryptocurrencies through financial markets.

Listed Trusts

Given the lack of approval from their respective securities commissions to operate under an ETF structure, passive cryptocurrency funds have had to trade mostly under listed trust structures. The most popular of these is the Grayscale Bitcoin Trust (GBTC), which is the largest Trust of its type in the world, with USD $31.2 billion AUM as at the 5 March 2021.

It is structured whereby accredited investors are able to buy shares of the fund directly at the value of the underlying Bitcoin in daily private placements but are only able to sell these on the secondary market to retail investors after a 6-month lockup period.

Secondary market investors are then able to trade these shares amongst themselves, with premiums and discounts to NAV indicating levels of demand and supply. Premiums have existed for prolonged periods, with this occurring due to the lack of competition in the market. It has been most prominent when there are significant shifts in demand and supply and has led to GBTC effectively functioning as a leveraged exposure to Bitcoin – trading at a premium when sentiment is positive, and a discount when sentiment is negative.

The premium to NAV has exceeded 100% since its inception, and more recently reached 40.18% on December 21.

However, since the 18 February listing of the Purpose Bitcoin ETF (TSE: BTCC), which is the world’s first “direct custody” bitcoin ETF, the GBTC premium has collapsed, reaching a discount of 11.92% on March 4.

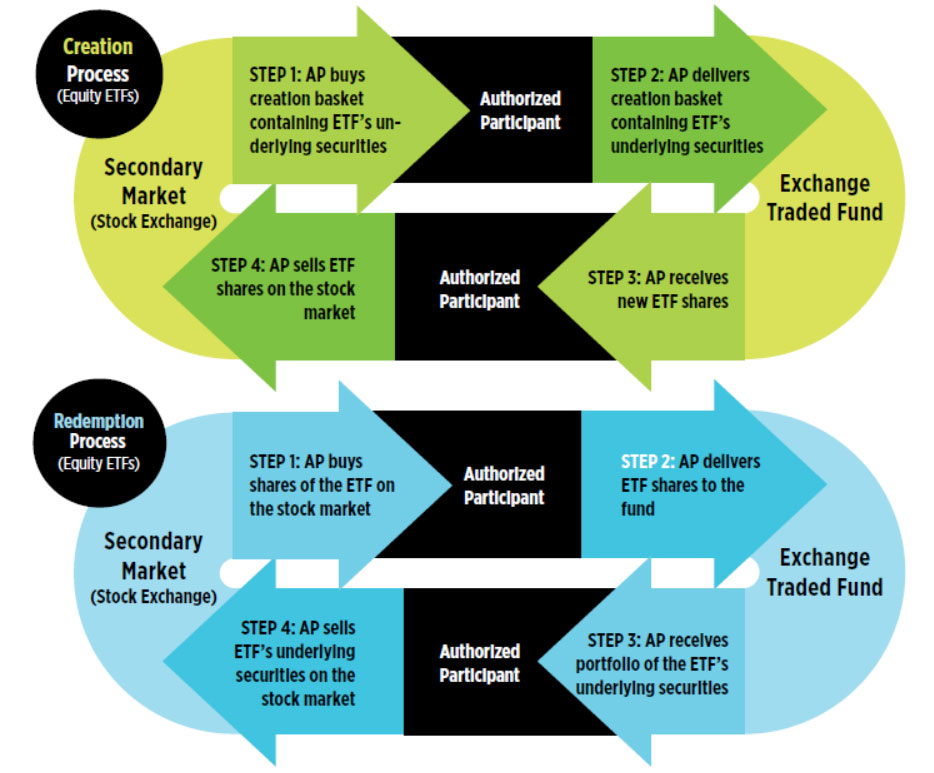

Exchange Traded Funds (ETFs)

Cryptocurrency ETFs offer a more accessible and efficient manner to gain exposure, with premiums to NAV typically corrected quicker than listed trusts, given the creation/redemption process.

For cryptocurrencies, ETF’s have been faced with regulatory hurdles for many years given their questionable position as an asset class.

The approval of BTCC by the Ontario Securities Commission was the first Bitcoin ETF approved in North America and served as a milestone through providing access to Bitcoin for investors both unable or unwilling to self-custody or invest in a trust structure.

The Ontario Securities Commission has also since approved a second Bitcoin ETF, Evolve Bitcoin ETF (TSE: EBIT), with two Ethereum ETF applications in progress as well.

In America, a bitcoin ETF looks likely, given President Biden’s pick to lead the SEC, Gary Gensler – a crypto advocate and someone who has a deep understanding of blockchain technologies.

In Australia, ASIC have only announced that they are not opposed to an ETF, however a listing would be likely, should other countries also grant approval.

Cryptocurrency stocks

Whilst this article has largely focused on the rise of Bitcoin and its associated securities, it does not mean that other major cryptocurrencies such as Ethereum have been left behind.

There are still significant investments in alternative cryptocurrencies, with Grayscale Ethereum Trust holding a respectable US $4 billion AUM.

Bitcoin ETF’s are likely to act as a precedent to enable similar investment products for other major cryptocurrencies.

The more investors are exposed to Bitcoin, the more likely it is that they will gain exposure to the wide ecosystem of cryptocurrencies.

All things considered, it is important to remember that cryptocurrencies are in their infancy – they’ve only existed for 10 years and are bound to face road bumps for years to come. They have the capacity to become a genuine part of asset allocation, however, prudent regulation is required to protect investors.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.