What is Private Credit?

Private Credit broadly refers to debt financing provided by non-bank lenders to borrowers who typically either do not have access to bank financing or prefer not to use it. These loans are not publicly traded and are to varying degrees illiquid in nature.

Private Credit managers can be institutional investors, such as super funds and insurance companies, private equity firms, and alternative investment managers. These lenders may offer customised terms and structures that can be more flexible than those of traditional bank loans, including consideration around areas such as maturities, collateral, and covenants.

To provide some further definition in this space, see below for some broad sub-sectors –

Private Corporate Debt – The private equivalent of publicly traded Corporate Bonds

Private Residential Property Debt – Typically mortgage-backed securities purchased from non-bank lenders via warehouse structures.

Private Corporate Property Debt – This takes the form of both direct commercial property and development lending, as well as commercial mortgage-backed securities.

Specialist finance – Typically Asset Backed Securities that might be in areas such as insurance or motor vehicle finance.

Strong Growth

Both locally and overseas we have seen significant growth in Private Credit in recent years as highlighted below –

Source: Goldman Sachs

There have been two key drivers to this growth –

1. Banks increasingly stepping away from middle market lending. With enhanced capital requirements and risk weightings applied to certain assets banks hold on balance sheet, banks have increasing shied away from lending to SMEs. This has created demand from corporates for alternative sources of funding as they look to grow their businesses. As a result, Private Credit providers have look to fill this void and been able to in large part drive attractive terms with their lending.

2. The other factor has been ultra-low interest rates, which meant that up until 2022, there was a search for yield across markets. In this environment private credit funds targeting returns of cash + 4% and higher have been seen to be very attractive.

What are the potential benefits of an allocation to Private Credit?

Diversification within the defensive allocations of your portfolio

As outlined above, Private Credit typically operates where public markets do not. While there is some crossover, a Private Credit strategy will therefore give you exposures that you won’t typically have in your traditional Investment Grade and High Yield credit funds. In particular, from a local perspective, the access to middle market lending provides exposure to sectors that aren’t as well represented at the top end of the resource and financials heavy Australian market.

Higher Target Returns

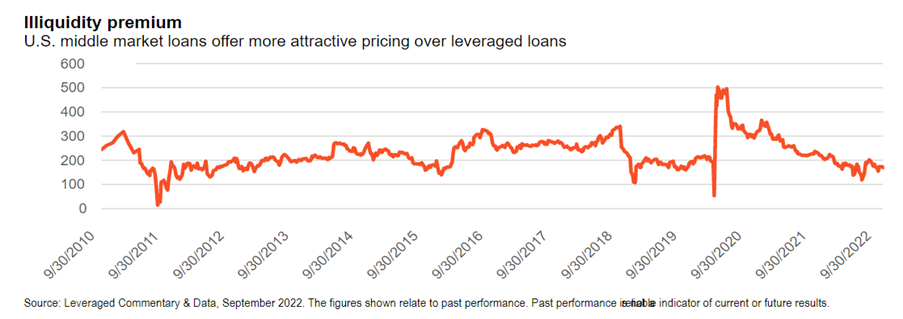

Private Credit strategies should and typically do target higher returns than traditional credit funds. This should be expected given most strategies operate in the illiquid, sub-investment grade space and therefore need to offer these higher levels of compensation. This is underpinned by the fact that most corporates and debtors in this space can’t get bank lending, and so are prepared to pay higher interest rates for their funding. See below for an illustration of that illiquidity premium in the US, where there is a deeper, more mature private credit market.

Capital Structure and Controls

With Private Credit typically operating in the sub-investment grade space, managers will generally look to improve the risks of their investments by sitting up high in the capital structure of those entities that they lend to. The greatest security is typically attained by being Senior Secured, which places you ahead of other more subordinated debt and equity and is backed by an asset that is pledged as collateral. Long-term average recovery rates on senior secured lending in the event of a default are circa 80%.

The other way on which managers seek to improve their risk profile are through covenants that are arranged as part of the loan. Private lenders will often seek covenants around things such as a cash balances, earnings, and debt levels. If companies breach these covenants during the life of the loan, the manager will typically have access to a range of remedies such as a higher interest rates or future royalties from the company.

Are there areas of concern?

That there has been a mini gold rush in Private Credit naturally means that it has attracted a broad spectrum of providers to the space. There are numerous managers that have been running for only a few years and have limited heritage as a private credit manager. That’s not to say that a number of these newer providers can’t ultimately be successful through time, but that as of yet they haven’t been tested through a cycle. What are the key things to consider in this case, when thinking about which managers to allocate to?

Diversification

Either by design or because they are still in the early stages of FUM growth, many private credit strategies look particularly concentrated. This might be concentration in terms of holdings e.g. only having single digit or low double digit number of portfolio holdings. It is also often sector concentration, for example a strategy that just invests in the property sector.

As highlighted above there are approaches managers can take to minimise these risks in terms of being senior secured, strong covenants etc. However, it’s important to understand that this only reduces a degree of risk. Many of these strategies are highly concentrated, and it requires an appropriate assessment of whether the returns on offer are commensurate with this risk.

Liquidity

This is an illiquid investment class and the majority of holdings in most managers’ portfolios are not investments that could be readily sold ahead of maturity. This is not a problem in and of itself, but understanding this profile and ensuring a fund is structured accordingly in terms of any potential redemptions is important. A notionally more liquid offering may not actually be a positive because of the mismatch this creates in environment where a weight of clients look to liquidate holdings.

Valuations & Volatility

Private Credit investments are by definition not publicly traded, and the valuations for portfolio holdings in any given fund is determined by the fund manager. Many managers in this space value their holdings at par, unless there is an explicit impairment. Accordingly, you will often see a very steady and stable unit price for a given private credit fund. While this approach has a certain logic given these holdings are illiquid and there isn’t explicit public market pricing, it also has the potential to create a false sense of security around the risks in a sub-investment grade portfolio, and an adverse reaction to a change in the unit price if and when a meaningful impairment occurs. Conversely there are managers that are utilising a range of public and private reference points to mark to market the portfolio on a regular basis, providing in our view a better sense of portfolio valuation and conditioning clients to a degree of volatility. Wherever possible we believe this is a preferred approach.

Experience and Alignment

An additional and critical question to consider is the breadth and experience of the fund management team? Look to assess the degree of key person risk and whether the team have experience in this space through a full market cycle. Are the team well aligned to the end investors and relatedly how are any fees structured. We found there to be broad range of outcomes across the space.

Credit Quality

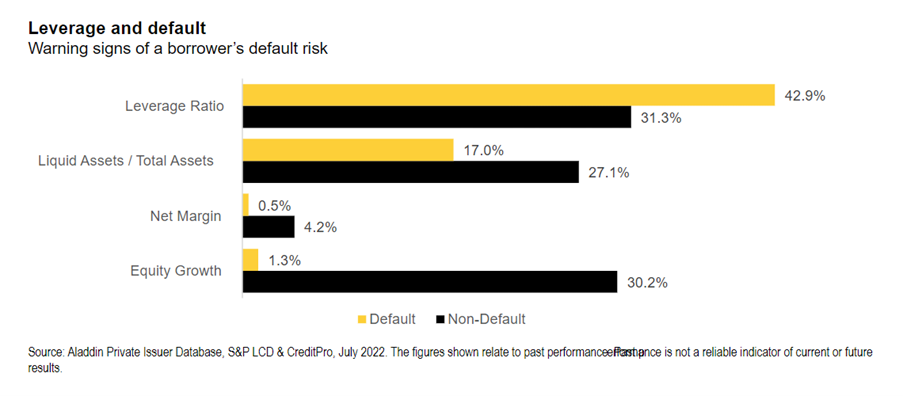

Getting an understanding of the underlying leverage of the portfolio holdings in a portfolio will provide a further lense on how much risk is embedded in a given strategy. While a fund may typically have senior secured exposures, if these exposures are in highly leveraged micro and small cap companies, there remains a meaningful risk of default as highlighted below –

Digging into the credit quality assessment a manager undertakes will provide a better sense of these underlying risks.

Direct Origination or Syndication?

Private Credit investors, depending on the size and scale they operate at, can choose to either originate their own loans or alternatively invest with other creditors in a syndicate. Direct origination enables you to control the terms of the loan including any covenants and the ongoing relationship with the debtor. With syndicates, there is a lower level of control in terms of what the loan looks like, but it can open up unique opportunities that may not be available to you as a single creditor. Both approaches can in fact be complimentary in a portfolio, but understanding which risks you are taking with your manager and the pay-offs involved are important.

Summary

A high-quality private credit manager can be an important source of additional returns and diversification within an overall portfolio. However, in a space that is by definition more opaque, it is important to do your due diligence. Virtually all Private Credit managers have done well from a relative performance perspective in recent years. As we approach a point in the economic cycle, however, where risks of a recession have become more elevated, it’s worth spending the time ensuring your private credit allocations are right-sized and with high-quality managers.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.