We are coming close to finalising our Growth Alternatives Sector Review and we thought it timely to share some of our thoughts and key considerations. This is arguably the most challenging sector across asset classes to review, and yet also potentially the most rewarding in terms of being additive to your portfolios.

What are Growth Alternatives?

At Mason Stevens we allocate up to 20% into Growth Alternatives within our Flagship Portfolios. So what are Growth Alternatives and why do we allocate such a significant weight to them? We classify Growth Alternatives as any strategy with equity like growth objectives, but with low correlation and market beta to both equities and bonds. This encompasses a very wide and eclectic range of investment managers and strategies, and understanding whether you are dealing with a genuine alternative to traditional asset classes is not always straightforward. There are however, a small handful of key markers to provide guidance which we will go through further in this article. Some well recognised strategies in this asset class include:

Global Macro – these strategies look to typically take both long and short position across a range of asset classes, aiming to profit from broad market swings caused by political, economic, or market events.

Long/Short – These are strategies that typically actively manage their overall net exposure to equities markets while also going both long and short individual stocks. Market neutral strategies that aim for a net 0% exposure to markets are in the broad same family of strategies, however, can also be classified as defensive alternatives depending on levels of leverage used.

Private Equity (PE) – investment of equity capital in private companies not listed on a public exchange. While PE is obviously equity and could therefore be classified as equity at an asset class level, the low correlations and market beta of PE when compared to public markets leads us to classify it as a Growth Alternative allocation.

Trend Following – Also known as Commodity Trading Advisors (CTAs), these strategies look to go both long and short across a range of asset classes based on short-medium term price momentum.

Multi Strategy – These can be varied in their approach, but will typically have some combination of the above discreet strategies in one portfolio.

This list is not exhaustive but captures the main strategies available to advisers in the local market.

What role should they play in portfolios?

Within the context of a multi-asset portfolio, an allocation to a strongly performing Growth Alternatives sleeve will typically significantly enhance the risk adjusted return of the portfolio over time. The low market correlation and beta will reduce overall portfolio volatility, while still providing equity like returns over the longer term.

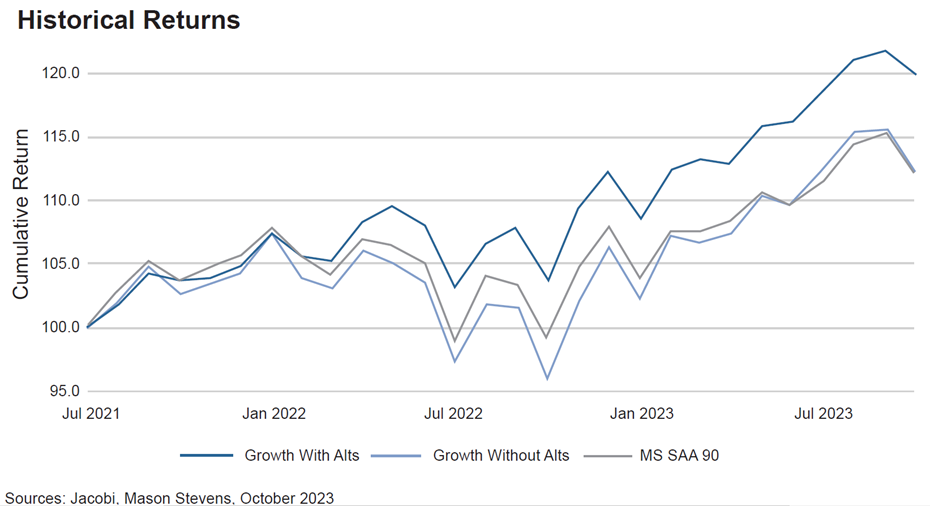

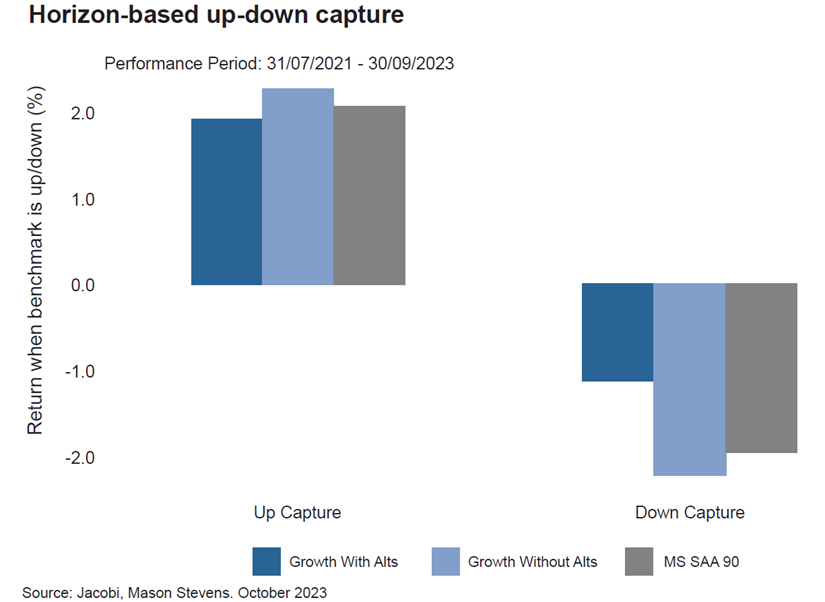

The below charts look at the back tested past performance* of our current Flagship High Growth portfolio, with and without Growth Alternatives.

As can be seen in this backtest the addition of Growth Alternatives has not sacrificed returns over time, in fact they have enhanced returns. Furthermore, and just as importantly, these enhanced returns have been delivered with significantly lower volatility and drawdown capture in the overall portfolio resulting in a consistently higher Sharpe Ratio.

* Past performance is not a reliable indicator of future performance and may not be achieved in the future.

Easy to say, hard to do

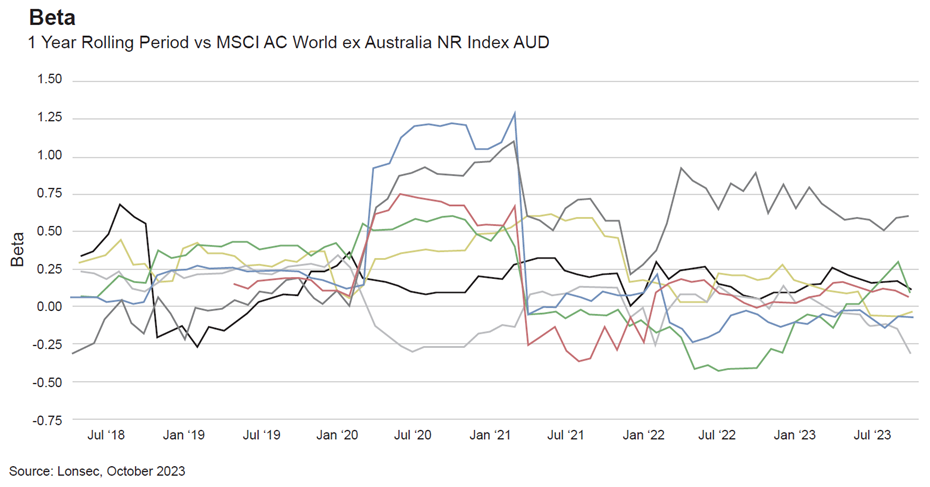

Adding alternatives into a portfolio has long been understood to improve the risk adjusted returns of a multi-asset portfolio, but the reality is that achieving this outcome in the Wealth space in the past decade or so has been easier said than done. The space is littered with strategies that haven’t necessarily done any major harm, but have certainly underwhelmed. Below is a chart of the equity market beta of a range of well-known Global Macro strategies available in market currently.

As can be seen, a number of the strategies have had significantly high equity market beta at times, approaching 1 or even exceeding 1, particularly at times when it has been least wanted i.e. March 2020, and the first half of 2022. On the other hand, there are a couple of strategies that have avoided significant levels of market beta over the past 5 years, which might put them in contention for your portfolio.

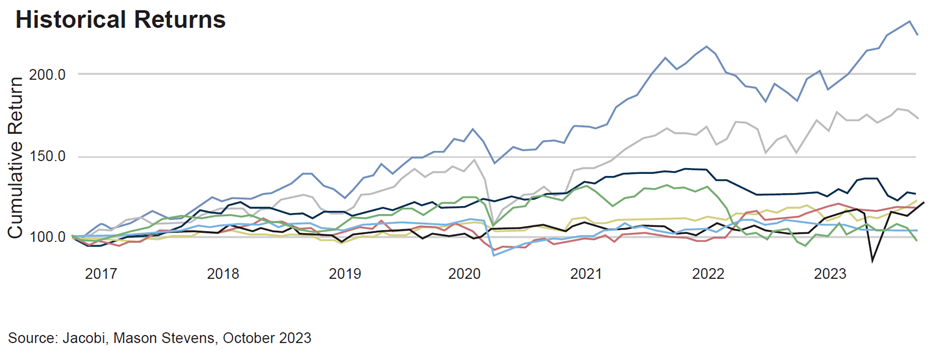

The kicker here, however, is that in all cases, whether they have been low or high market beta, this set of Macro funds have all failed to provide Equity like returns over the last 7 years, and indeed have generated returns either a bit below or a bit above cash. In the chart below the highest return line (in blue) represents global equities, while the second highest return line (in grey) is Australian Equities – the remaining lines are the aforementioned global macro funds.

Each strategy here may have idiosyncratic reasons for this underperformance, but in aggregate it demonstrates how difficult Macro is to get right. This is not to invalidate Global Macro, but rather to emphasise the importance of casting the net wide to get the right manager. And in the instance you can’t find a manager you don’t have the highest conviction in then there is no imperative to allocate to the given sector.

Other Growth Alternatives strategies have had better performance in recent years, however, it remains a mixed bag, where manager selection has a material impact on outcomes. Fundamentally this is because Alternatives strategies are more reliant on manager skill than other asset classes. A typical equities or bond manager will generate the market return plus or minus a bit over time. Any underperformance vs the market will be disappointing but an underperforming active manager will likely still give you a meaningful real return over the long-term because of that market beta.

With many Alternatives strategies, however, there is no beta ballast to fall back on. Get more calls wrong than right and the outcomes are likely to be well below the investment objective and potentially below inflation over time.

Getting the manager right

Moreso than any other asset class, Growth Alternatives demands a focus on manager selection. If a manager is going to generate equity like returns and do it without meaningful equity market beta, it requires a level of investment skill that is not always easy to find. While there are no guarantees with any manager selection choice, testing and re-testing their approach and your assumptions are critical. With that said what are the key things to look for?

Have they identified an information edge and can they exploit it consistently?

Having a clear view on what makes a manager different from peers, how this is executed on, and how this logically should result in alpha generation is a central consideration when reviewing any manager. A manager should be able to clearly articulate what their competitive advantage is and how this will be maintained over time. If the explanation is not compelling or can’t be clearly understood, the strategy should be avoided.

Have they got a process that can evolve?

If there is some inefficiency in markets that a manager is exploiting, in the majority of cases it will be found by others eventually, and that alpha generation capability diminishes over time. Is there an acknowledgement or awareness of this and have they got an investment or research process that can evolve? Is there a team constantly researching that next potential source of alpha, and what is the process supporting this? Is there, for example, an investment process that incorporates Bayesian methods to adjust to new information? A manager should be able to provide you with a clear view on how they intend to maintain their information edge over the long-term.

How well do you understand their portfolio and exposures?

If you can’t get transparency on a managers portfolio holdings and exposures, look elsewhere. The fact that the approach might be more esoteric and complex than an equity or bond fund is all the more reason to make sure you have a clear picture of what they invest in and why. If the manager doesn’t provide this and you see a period of underperformance, on what basis will you continue to hold the investment other than simply trusting the manager? This ability to demonstrate transparency on holdings and exposures is also a baseline for getting comfort over the risk management processes and systems in place.

What are the fees?

Growth Alternatives will invariably be the most expensive part of your portfolio. The costs often involved in running a unique alternatives strategy plus the logic of a well aligned performance fee will see total cost ratios be north of 2% p.a. and sometimes as high as 4% p.a. No one especially likes paying these fees but if the after fee return meets the objectives then the strategy will justify its place in the portfolio. If it doesn’t however, you’re left with a high fee/low return allocation. This again just highlights the importance of getting the manager right.

Assess the full track record

If there is a track record over a reasonable timeframe, do the obvious in terms of assessing performance against risk and return objectives. Beyond that however, it’s important to assess the market correlations and beta over different times frames. Breaking this down into shorter as well and longer term time frames will provide a full picture as to not only how the manager has performed during different market conditions, but also how additive the strategy will be in your overall portfolio. Has it held up the portfolio when other parts of your portfolio were drawing down? Where there are anomalies or periods of underperformance, these are the areas to interrogate in more detail.

Summary

A high-quality Growth Alternatives allocation will be meaningfully additive to your overall portfolio. It will likely decrease portfolio volatility while potentially also enhancing returns. However, in an asset class that can be opaque, and where there isn’t necessarily any market beta to do the heavy lifting in delivering returns, it is critical you do your due diligence. As we approach a point in the economic cycle where risks of a recession have become more elevated, it’s worth spending the time working through the criteria outlined above to provide your portfolio with the best chance of success.

Written by Andrew Ash, Head of Manager Research

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.