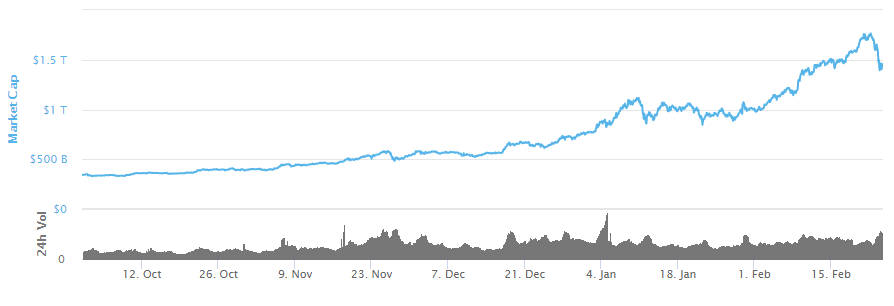

Cryptocurrencies are the talk of the town, with their total market capitalisation increasing from $344 billion USD on the first day of October 2020, to $1.46 trillion USD as of the 24 February 2021, representing a 324% increase over just 4.5 months.

Central to its growth has been a multi-faceted narrative driven by:

- Increased institutional acceptance (both in the form of investments and provision of services such as custody and payments)

- Worries of inflation following unprecedented levels of central bank intervention and budget deficit spending

- The addition of cryptocurrencies (primarily Bitcoin) to corporate balance sheets

- Favourable regulatory environment

Whether you believe in cryptocurrencies as a concept is becoming increasingly irrelevant, as a well-informed understanding will be essential for justifying their inclusion or exclusion from portfolios.

As part of the younger generation at Mason Stevens (both in age and by name), I’ll take you through a 3-part series over the next few weeks – delving into blockchain, cryptocurrencies and the investment landscape.

Blockchain

“Blockchain” has become a buzz word and is often thrown about without any real explanation as to why it is important. It was first created by a person (or a group of people) in 2008 – using the pseudonym Satoshi Nakamoto, to serve as the public transaction ledger for Bitcoin.

Since then, blockchain has expanded far beyond the cryptocurrency space, and has the potential to act as a foundational piece of technology for which our economic and social systems can be built on.

What is Blockchain?

Contracts and transactions serve as the basis for our economic and social systems. They set boundaries, protect existing assets, verify our identities and guide the actions we take.

However, as the world has become increasingly more digitised, the way in which we maintain administrative control has remained largely unchanged.

Blockchain provides a solution for this – allowing verified and permanent transactions between parties over an open, distributed ledger.

It acts as a transparent, decentralised and immutable database, recording transactional information in the most efficient manner possible.

It can be used without a centralised authority, and between individuals or entities who have no basis to trust each other.

It can issue, transfer and record ownership of the asset which the blockchain is based on and offers 24/7 settlement.

So, how exactly does a blockchain work?

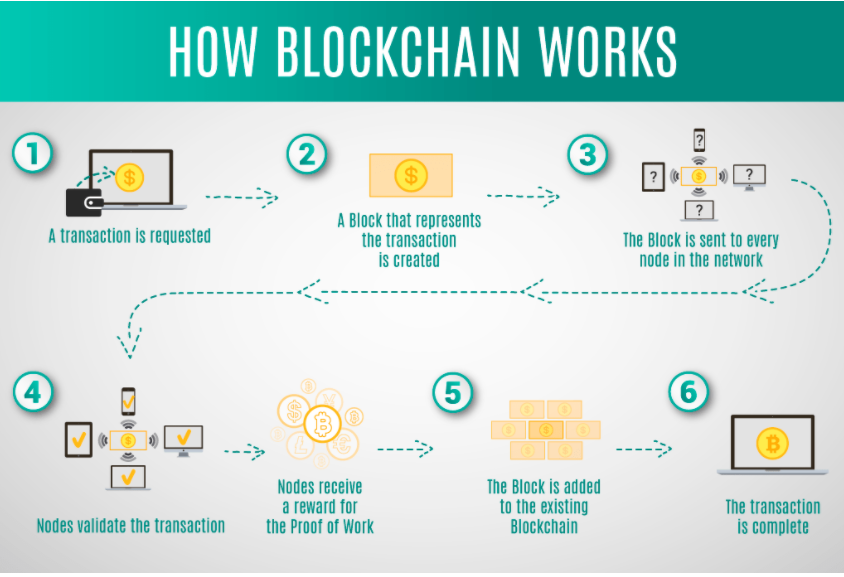

There are six steps which are involved in the functioning of a blockchain:

- A transaction is created – in the case of Bitcoin, this would involve entering in the quantity you would send, and the unique address to which it should go to (a unique 34-character key with a combination of letters and numbers).

- The block which represents the transaction is created on the blockchain.

- The block is sent to every node in the network – in the Bitcoin world, these nodes are also known as miners

- These nodes/miners validate the transaction – the method in which they do so differs between each blockchain, however most are built on proof of work (PoW). PoW involves the calculation of complex algorithms, with miners competing against each other on the basis of computational power (i.e. who can solve the algorithm first). Nodes then receive rewards for these efforts (which are paid for through transaction fees from the sender)

- Once validated, the block is then added to the blockchain. Each block contains three things – a timestamp, the transaction data within it, and a cryptographic “hash” of the previous block. These hash values are effectively “fingerprints” of the transactional data and involve the generation of a hash key (a 32-byte output), through taking the transaction data as an input. The moment the block is created, the hash is automatically generated, allowing the detection of any future alterations to the transactions within the block (and therefore making the blocks unchangeable). An important distinction to make is that the blockchain itself does not house the data – it houses the hash key which can be used to verify any data. This hash key also can’t be reverse engineered.

- The client receives the transaction.

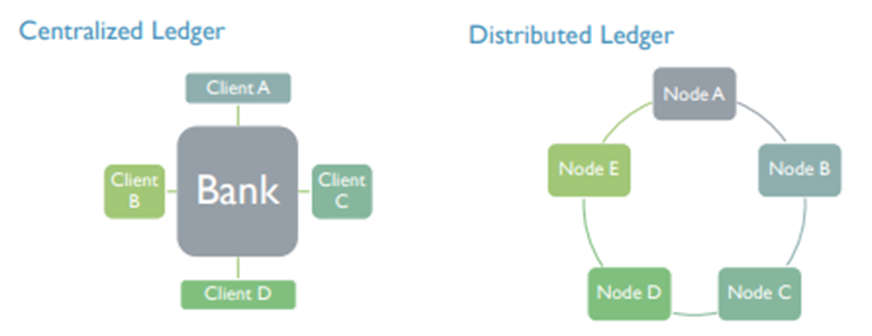

Now that we have gone over how the blockchain functions, we can focus on a potential real-world use case – the banking system.

In this situation, the centralised ledger represents a bank.

Clients depend on the bank to reconcile balances and must convince the bank to amend any discrepancies should they arise. The clients also rely on the banks employees to ensure their accounts remain functional and accurate, with some services only available to customers during business hours.

The bank is effectively the only “node” – they have control over transaction records and offer little transparency.

On the other hand, a distributed ledger is transparent and there is no central administrator. Transaction records and unit holdings are guaranteed to be correct. Transactions speeds vary only by the difficulty of the algorithms posed to miners, and by their hash power (power of computers used by miners).

Costs will theoretically be lower, given the removal of the cost intensive intermediary.

In this example, we use a bank – however blockchain can act in place of any sort of centralised authority, and can be used for property records, digital identity, supply chain management, capital markets, healthcare records and much more.

Along with verifying transactional data, blockchains can also integrate smart contracts – which are self-executing contracts with the terms of the agreement written into the lines of code.

An easy (but morbid) example of this would be a life insurance policy. Upon death, the provision of a notarised death certificate would then release the funds immediately to the designated beneficiaries.

Where to next?

I would assume that most of you would have heard the claim that blockchain technology will revolutionise the business world – and I hope by this point in the note you would start to believe it is a possibility.

For the believers, the only real question is, “When?”.

Blockchain is a foundational technology (Harvard Business Review) – and has the potential to reshape economic and social systems. As its implementation involves uprooting existing networks, implementation will be slow and gradual, and it may take decades for it to spread throughout all facets of society.

However, current use cases can be seen close to home, with CBA in conjunction with the World Bank, launching Bond-I (Blockchain Operated New Debt Instrument) – the world’s first bond to be created, allocated, transferred and managed through using blockchain technology.

Bond-I is able to offer improvements on existing practices, by automating processes through smart contracts, increasing efficiency through reduced administrative overhead, improved price transparency, and improved productivity through simplifying operational processes.

The CBA has since launched a second bond through Bond-I, with this technology having the potential to bring more transparency and reduce levels of fragmentation in capital markets.

Transmission Control Protocol/Internet Protocol (TCP/IP)

TCP/IP was introduced in 1972 as tool for researchers in the U.S. Department of Defence to communicate with each other and is a set of standardised rules that allow computers to communicate with each other over a public network. This was the first iteration of e-mail and is viewed as the foundational technology behind the internet (Harvard Business Review).

Prior to the creation of TCP/IP, telecommunications were based on circuit switching, where telecom service providers manually connected nodes between the two parties which were communicating.

TCP/IP revolutionised this process through digitising and breaking up information and sending this to any recipient on the network without the need for dedicated private lines.

Much like blockchain, it was a shared, open and decentralised public network.

Initially few saw the potential of TCP/IP, however over the 80s and 90s, its capabilities built out beyond email, eventually forming the basis for the World Wide Web.

Since the proliferation of global internet connectivity, businesses have revolutionised their respective industries – eBay with online auctions, Google with search engines and Skype with telecommunications.

All in all, it took TCP/IP 30 years to reshape the global economy – enabling e-commerce, efficient communication around the world and improving the standard of living for many.

This was the last major foundational technology to be implemented and offers an idea of long road which potentially lies ahead for blockchain implementation.

Investment opportunities

Whilst blockchain may be an exciting concept, it remains as a difficult thematic to invest into. As with the internet, the success of a company won’t be determined by the presence of a blockchain, but instead by how they choose to utilise it.

Companies like Amazon (AMZN) have succeeded not by simply conducting their business on the internet, but by providing the best selection, price and delivery options through the internet.

However, some ETF’s do exist, with the intention of tracking blockchain related companies:

Reality Shares Nasdaq NexGen Economy ETF (NASDAQ:BLCN)

BLCN aims to offer investors exposure to companies who are exposed to cryptocurrency and the blockchain. It tracks the Reality Shares Nasdaq Blockchain Economy Index – which is made up by stocks committing material resources to developing, researching, supporting, innovating or utilising blockchain technology. The index is weighted by a “blockchain score” which ranks the companies expected to benefit most from blockchain technology.

Amplify Transformational Data Sharing ETF (NYSE:BLOK)

BLOK is an actively managed fund with a strong focus on companies using blockchain technology, and as such represents more of a pure play blockchain investment relative to passive blockchain ETF’s. Top holdings for the ETF include Microstrategy (NASDAQ: MSTR, the first company to add BTC to their balance sheet) and Hut 8 Mining (TO:HUT, a Canadian BTC miner).

Next week, we will take an in-depth investigation of cryptocurrencies, their historical performance, and the narratives which have driven their current valuations.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.