The capitalistic society which has propelled the human race to our current standard of living has been built upon the efficient allocation of resources, governed by the laws of supply and demand.

Capitalism is merit based, with the allocation of capital being determined by the needs and wants of individuals.

Elon Musk’s recent tweets over the environmental sustainability of Bitcoin have sparked a debate regarding the ESG credentials of Bitcoin, and whether or not it is an appropriate allocation of resources or capital.

However, the focus should not be on whether or not Bitcoin is environmentally friendly – it should be regarding whether we are willing to bear negative environmental externalities in return for the potentially positive benefits a non-state monetary authority/store of value asset would generate.

As in any discussion, context is key – where one must also consider the difference between emissions and energy usage, the ESG credentials of rival asset classes like gold, and the transition which the industry has been making in its pursuit towards becoming more environmentally sustainable.

So What Happened?

Over the last two weeks, the value of Bitcoin has fallen by 32%, wiping out over USD$345 billion in market capitalisation.

More broadly, the cryptocurrency market has fallen by over USD$700 billion, erasing all gains made since early March of this year.

Total Market Capitalisation of Cryptocurrency

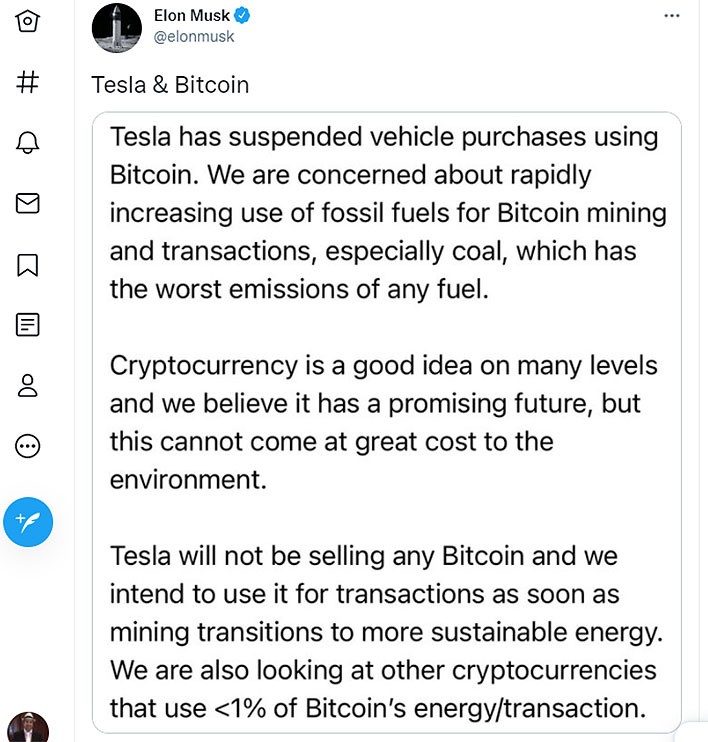

The beginnings of this drawdown can be traced back to one man – Elon Musk.

Tesla initially decided to invest $2 billion USD in cash reserves into Bitcoin and accept it as a mode of payment, however, Musk partially unwound this position, citing environmental concerns whilst removing Bitcoin as an accepted mode of payment.

Once the selloff began, it accelerated rapidly with over-leveraged positions quickly liquidated in futures markets.

If there is one thing we were reminded of during this crash, it’s to expect severe volatility in an unregulated market with high retail participation, and easily accessible opportunities to use 100x leverage.

Is Bitcoin Heating Up the Oceans?

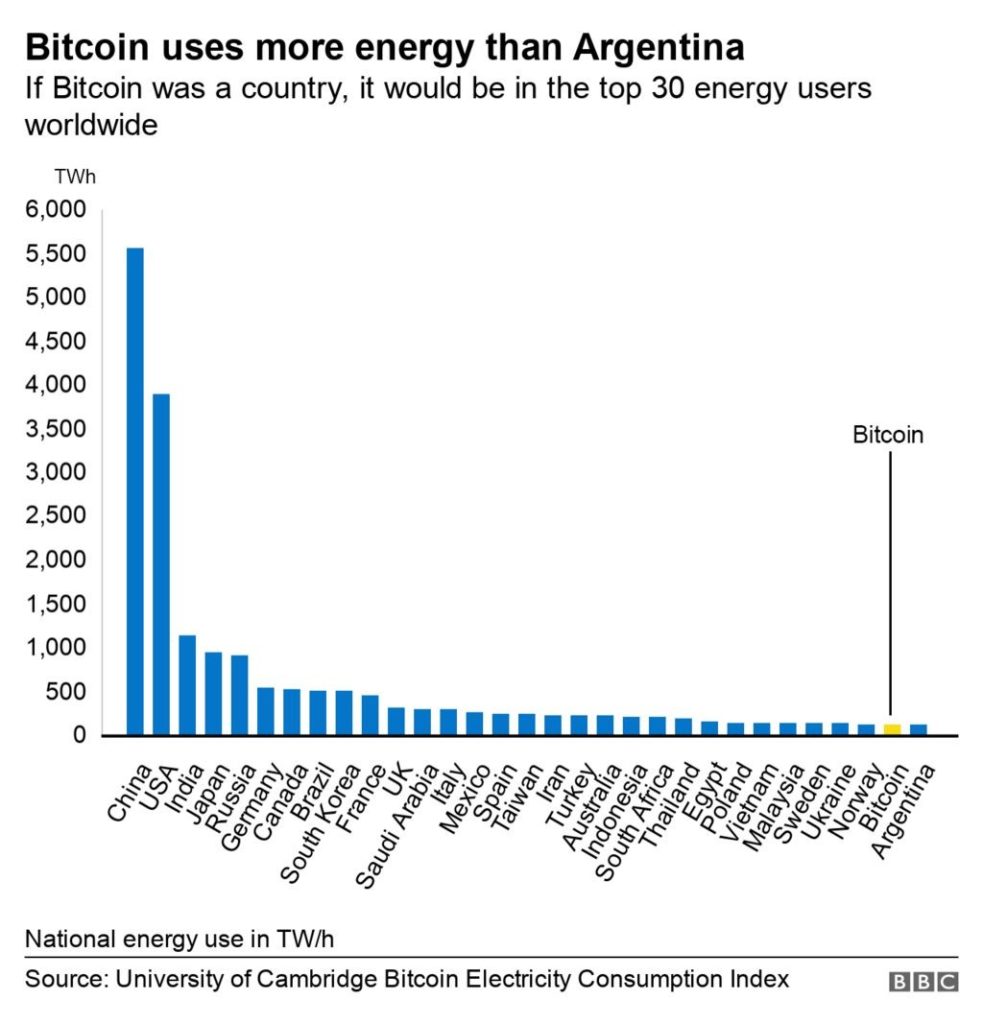

The environmental burden of Bitcoin mining has recently received intense scrutiny, using similar amounts of energy to countries such as Argentina and Norway.

However, context is required when looking at figures such as this – if Bitcoin was powered by 100% renewable energy sources, its impact on the environment would be relatively small.

Viewing Bitcoin mining in the chasm of energy usage is misleading – it’s all about emissions.

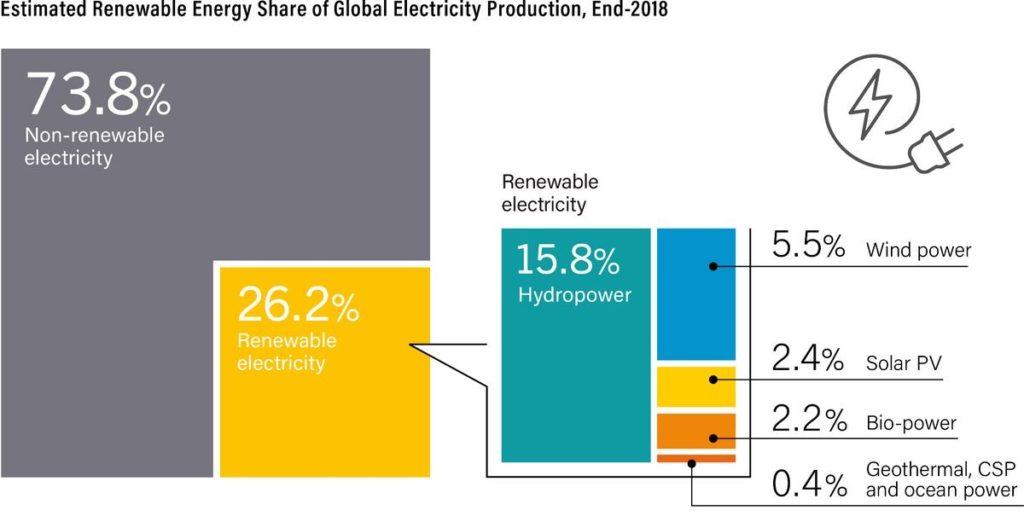

Currently, precise figures over the cumulative share of energy from renewable sources are unknown, however estimates range between 39% and 73%. The lower bound of estimate alone is more than two times the share of renewable energy used in the United States and 50% higher than the global proportion of renewable energy usage in 2018.

On an absolute basis, Bitcoin still uses a considerable amount on non-renewable energy, however this figure is set to improve, with market participants incentivised to do so given the relatively cheaper cost of renewable energy sources.

However, what is often missed is the capacity of Bitcoin miners to support the renewable energy sector, which is a sector Max has discussed recently in his solar and wind/hydro notes.

The main issue facing utility companies is the instability of energy production – where energy may only be generated during the day (solar) or during certain seasons in the year (hydro), and the inability to store surplus energy using current battery technology in a meaningful manner.

The largest cost associated with renewables, and in particular, hydroelectricity, is the initial construction costs.

Before renewable energy is added to the grid, there must be assurances that it will be utilised.

Moreover, most renewable energy production is by nature, generated in remote areas, with battery technology unable to efficiently transport the majority of this into more urban areas.

This is where Bitcoin mining fits in – it can be mined anywhere in the world, with its location purely determined by the cost of electricity. Bitcoin mining is able to take up surplus energy on the grid (it is able to operate 24/7 – dependant only on the cost of electricity) and act as a consistent and reliable customer.

For example, in previous years, up to 50% of Bitcoin mining has occurred using hydroelectric energy in Sichuan during the rainy season, where in prior years, substantial amounts of surplus energy were wasted.

During dry seasons, the region only accounted for around 10% of global mining activities, with mining ‘rigs’ being transported to other areas of the country where energy was cheaper, highlighting the ability of Bitcoin mining to be geographically nimble.

In the near term, the recent mining ban in China is likely to improve the proportion of renewables used, with the majority of coal based mining residing in China.

Amongst other market participants, consciousness of the importance of renewable energy usage has been reflected through the creation of the “Bitcoin Mining Council”. This council is comprised of the largest North American miners and market participants like Elon Musk, who have all pledged to reduce emissions from mining activities, and to increase reporting transparency regarding energy sources.

Common misconceptions over the future of energy usage from Bitcoin must also be qualified.

Energy usage will not increase linearly or exponentially with price – in fact as time goes on, energy usage will likely decline relative to price, given the decentralised monetary policy built into Bitcoin.

Every 4 years, the rewards given to miners will halve, providing considerably less incentive to mine as approximately 80% of revenue is currently derived from block rewards.

However, this doesn’t mean that there will eventually be no miners left to validate transactions – Bitcoin’s protocol automatically decreases difficulty to incentivise miner participation.

All That Glitters is Not Gold

An analysis of the ESG credentials of Bitcoin must also be contextualised through assessing its competitors.

Gold, the asset class it supposes to replace, is one of the most destructive industries in the world – the creation of a single gold ring requires the displacement of over 20 tons of rock and soil, and often involves the use of mercury and cyanide, which can taint marine ecosystems downstream of mine sites (Earthworks).

Whilst movements towards “cleaner gold” have been made, it is almost impossible for mines to be environmentally sustainable. Emissions can be reduced through the use of cleaner energy; however, this can only be utilised if there are renewable energy sources in the region they choose to mine in.

All things considered; this shouldn’t be a discussion on whether we can justify such an environmental toll for a store of value asset. It may be the case that society values gold so much that it is willing to accept this trade-off, where this can serve as another example of an efficient allocation of resources.

Is Energy Usage Evil?

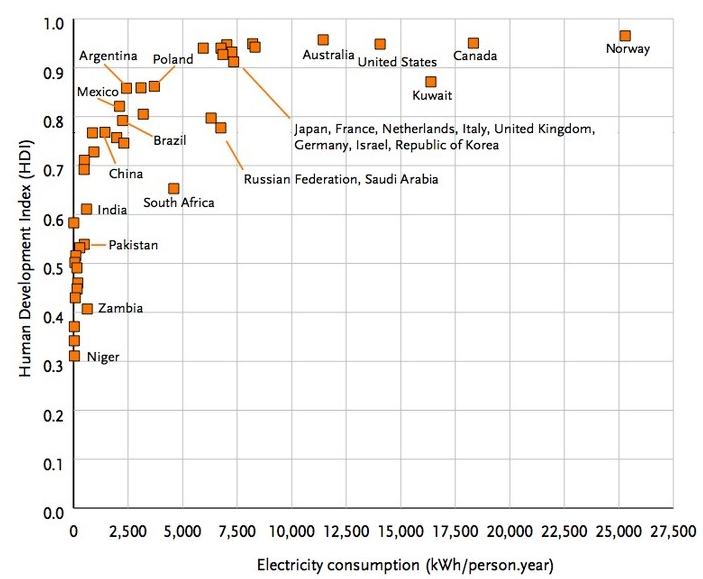

It has long been observed that those countries with the highest energy consumption per capita, are also those which are most prosperous.

It is important for society to scale up renewable energy sources as soon as possible, where we can expand upon our absolute energy production.

Energy consumption itself should not be viewed as a bad thing – it’s the energy source we use.

Regulations over Bitcoin mining can potentially play a role in determining the success of renewable energy companies.

Renewable energy providers in countries like China which have banned mining will face the consequences of the removal of an industry with consistent and flexible energy demand at scale.

To the Moon, Or To the Trash?

Bitcoin as an asset still remains incredibly risky, with the recent crash raising a series of question marks over the extreme volatility generated by relatively high rates of retail participation and easy access to leverage.

Moreover, the ability of one man to dramatically influence Bitcoin’s price action, and without any personal consequence, highlights the dangers of investing into a market with no central authority.

Investors must take extreme caution when evaluating the appropriateness of cryptocurrency for one’s portfolio and have an understanding that the safety guards which protect investors in traditional markets do not apply.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.