Growth investors have enjoyed a stellar decade, supported by an equity bull market and record low interest rates.

However, with increasing inflationary expectations and lofty growth stock valuations, investors have begun to rotate into other areas of the market.

We have recently covered the macroeconomic factors driving markets in great depth, including inflation (Inflation-linked Bonds, Lumber, Soft Commodities, Precious Metals, Industrial Metals), currency (Why the AUD Isn’t Higher) and economic outlook (Federal Budget, Australia’s Sovereign Credit Rating).

However, macroeconomic variables only make up one part of the decision-making process, with factor investing defining one’s security selection within industries and asset classes.

Following on from Jesse’s excellent introductory note yesterday, we will cover growth stocks, what drives their valuations and the case for further outperformance.

What is Growth Investing?

Growth investing involves selecting securities with a focus on capital returns (as opposed to income), and on those which are expected to grow above industry, or market wide averages.

Growth companies are typically smaller, less mature, and in the early stages of business life cycle – where revenues are growing, and profits are redistributed back into the business, as opposed to through dividends to shareholders.

What Influences Growth Investing?

Growth investors will typically place a greater emphasis on future earnings growth, as opposed to current intrinsic or book value, and as a result, trade on higher multiples of current earnings/revenue (higher P/E ratios) relative to more value-oriented companies.

Growth stocks have typically performed well in low interest rate environments, given there is a greater potential for higher earnings growth when costs of financing are lower.

Interest rates also factor into the way in which we value cash flows – where lower interest rates will mean that future cash flows are discounted at a lower rate – hence holding greater value.

As a result of having a greater focus on future earnings, growth stocks are often evaluated on the basis of their total addressable market (TAM), where value orientated stocks may be evaluated on the size of their current market.

Growth investors will also typically place greater emphasis on profit margins – where the ability of companies to turn revenue into profit can indicate the adequacy of management to manage expenses in the pursuit of expanding business activities.

Given their valuations are driven by forward looking earnings estimated, growth stocks are also vulnerable to market risk sentiment, and exhibit greater levels of volatility.

Can Growth Stocks Continue to Grow?

Many have forecasted that growth stocks are due for a period of underperformance, however select stocks are set to continue to be driven by the acceleration of work-from-home (WFH) and online shopping trends, generational technology developments such as cloud computing and artificial intelligence (AI), and decarbonisation efforts.

As the economy reopens, many, if not all workplaces will have more flexible working arrangements than before the pandemic, with those technology companies providing remote work software likely to continue to benefit. It is highly unlikely that workplaces will scale back WFH significantly, given the productivity and employee satisfaction improvement it has enabled.

Moreover, e-commerce has been ingrained into consumer habits, with improvements in the convenience and accessibility of logistics networks set to continue to enhance services, and profitability.

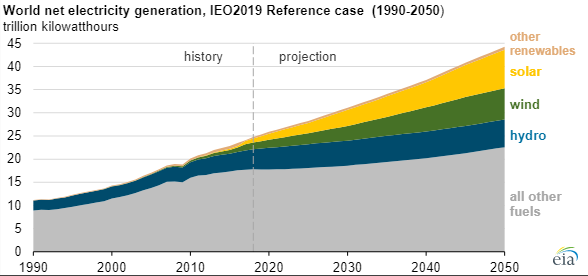

Furthermore, as governments grow decarbonising efforts, growth stocks in the energy sector should continue to outperform, with solar, wind and hydroelectric energy all set to increase their shares of global energy usage (which we discussed here and here).

Fossil fuel-based incumbents which previously made up a significant portion of the energy industry will suffer as investors continue to align ESG objectives within their investment decision making.

Will the Economy Grow Up and Move onto Value?

Since the beginning of the re-opening trade late last year, fund managers have been increasingly allocating funds away from growth and towards value.

GMO published an interesting chart, where the green and blue lines represent the cumulative performance of the Russell 1000 value index less the Russell 1000 growth index, making a parallel between current markets, and the run up to the dotcom bubble.

Admittedly, whilst cries of “this time it’s different” have almost always ended up poorly, one could surmise that growth stocks may continue to outperform over the short-medium term, assisted by structural tailwinds and generational technology developments.

Whilst value shares will eventually outperform for an extended period, investment decision making will not merely be a matter of picking growth or value, or even momentum or quality.

Certain value shares are likely to continue facing ESG headwinds, and certain growth shares will continue to outperform on the back of the aforementioned technology developments.

Careful security selection within asset classes or industries will become increasingly more important within our bifurcated markets, with a focus on strong fundamentals or growth prospects, sound business models, and skilful management likely to continue serving investors well.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.