The Mason Stevens OCIO international equity sector review has just been completed. This was a focused review of who we believe to be the best managers in market across the international equity asset class. This review has in turn informed decisions around managers on the Mason Stevens High Conviction List (HCL). The below article is an excerpt from this review and we discuss some key considerations around alpha generation for your international equities, and where some of the best opportunities lie.

How do you like your Alpha?

Do you expect Alpha from your international equity portfolio? If so, where is it coming from?

The first of these questions is an important one to ask as a baseline, especially in an increasingly concentrated market, where the US constitutes about 70% of global equities, and within the S&P500 the Magnificent 7 stocks (Amazon, Apple, Google, Meta, Microsoft, NVIDIA and Tesla) make up about 30% of the US market. Given this concentration and the level of analyst coverage of both this market and these stocks, it could be argued to be a highly efficient market where passive investing works best.

This dovetails into one of the well documented challenges with active management, which is to actually generate alpha. The majority of active managers do not outperform their benchmarks over time. Historically, this was to a large degree to be expected given fund managers constituted the majority of any given asset class. In such a scenario, mathematically there would inevitably be a significant percentage of active managers who underperformed the market before fees, and an even greater percentage after fees. This point however, has really been highlighted with the huge growth in passive investing, which has offered lower fees and the ability to beat the majority of active managers after fees.

At Mason Stevens we believe there is alpha to be found via active management, but that it requires a highly focused approach in identifying the managers that have and will continue to generate excess returns. This focused approach is effectively likely to represent the top quintile of managers over the long-term. We have a process that through both quantitative and qualitative analysis, we believe more consistently identifies active managers who outperform and/or meet their investment objectives. At the same time we always retain the flexibility to allocate to more passive solutions where we lack conviction in actively managed options available in any given segment or style.

If there is an ability to identify managers with genuine investment skill, the question then becomes ‘where do you expect your alpha to come from?’.

Geography, industry sector, factor (value, growth etc.), thematics and individual stock selection are all sources of potential alpha. In terms of these sources, how consistent, how repeatable, and how many are achievable in one portfolio are all questions that need to be asked when assessing a manager, and when determining what you expect from your international equity portfolio.

Historically, a large degree of focus when considering international equities managers has been on exposure to specific factors. This may for example be represented by an investment philosophy or style that favours value or growth. We can use these two factors to explore some of the opportunities and risks here. The below charts look at three distinct periods and the performance of the value and growth indices in these eras.

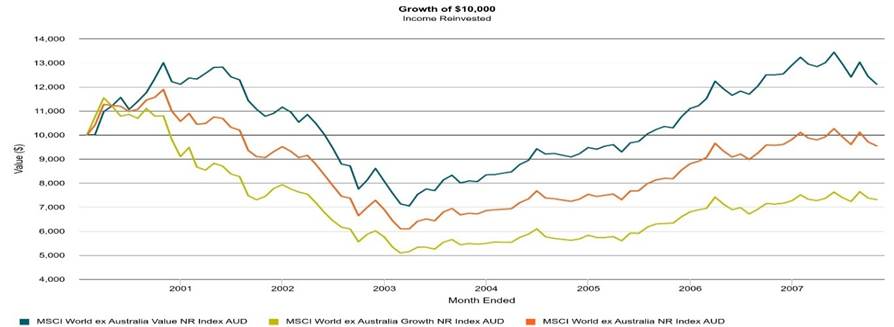

Chart 1: Value Significantly Outperforms Growth Between the Dotcom Bubble and the GFC

Source: Lonsec

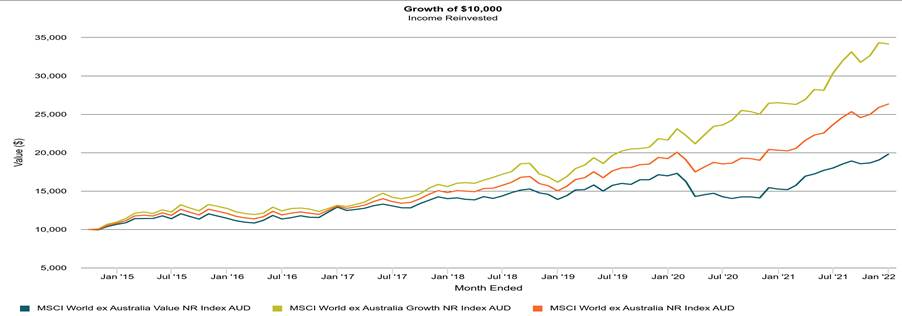

Chart 2: Growth Significantly Outperforms Value in The Era of QE And Ultra Low Interest Rates

Source: Lonsec

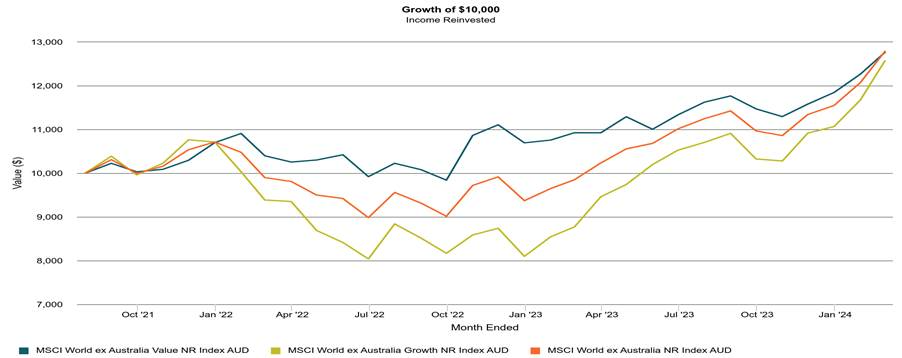

Chart 3: Value and Growth Share the Prize in the Two and a Half Years

Source: Lonsec

As can be seen from the above, allocating to these styles requires a degree of skill in terms of understanding the market regime you are in, the direction of inflation and interest rates, and therefore how you might allocate. A set and forget approach towards value or growth may result in a decade long period of underperformance.

If you do have a view, philosophy, or approach on the particular types of factors you want exposure to, or perhaps a manager that will take meaningful sector and geography positions, then there are relevant managers on our HCL. This includes high quality managers with long term track records of alpha generation, and importantly have the requisite fundamentals in place to continue generating excess returns.

Understanding, however, how these different approaches perform in different parts of the cycle and in different regimes is critical in better understanding when your alpha is likely to be generated, and just as importantly periods where you may underperform.

An alternative to this may be to seek out a core manager. Core managers by definition tend not to have any significant style biases, and importantly also don’t tend to take any meaningful country or sector bets. The best core managers generate consistent alpha predominantly via stock selection – effectively picking the best stocks within a given sector/geography.

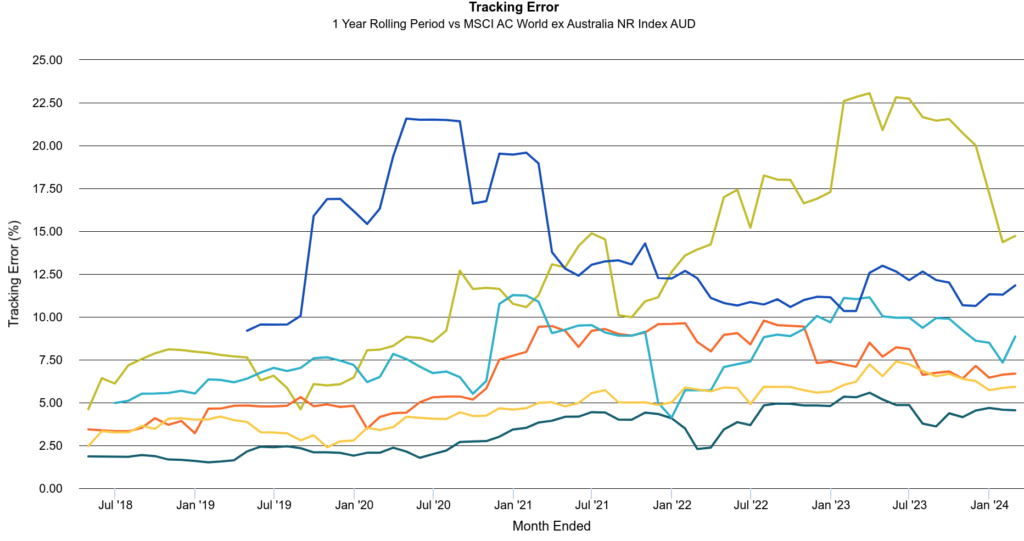

The below chart looks at the tracking error*, or the difference in performance vs the MSCI World, of a range of HCL managers. All have a particular style or factor focus, with the exception of the dark green line, which is one of our preferred core managers.

Chart 4: Core Manager Tracking Error vs Factor Influenced Managers

Source: Lonsec

As can be seen, the core manager’s tracking error is typically between 2.50%-5% on any given rolling 12 month basis. What this means it is unlikely to significantly underperform or outperform the market. The benefit of this type of strategy, if they can deliver alpha over time, is that you will get something that’s always reasonably close to the benchmark return and therefore adds a degree of predictability for your overall portfolio. If you’re understandably struggling to come to a strong view as to whether Magnificent 7 stocks truly represent a structural and productivity change in market, or instead are a bubble similar to the Dotcom bubble in the late 90s, then a core manager may be a sensible allocation in removing that question as a decision point and just focusing on delivering the benchmark return plus some alpha.

The downside of course is that you will largely own the market from a sector and geographical perspective and also track closely to the market during a large drawdown. This will differ from a higher tracking error manager who may be able to provide some meaningful downside protection in such an environment.

Alpha in Global Small Caps?

Unlike Australian small caps, where meaningful alpha is the norm, global small caps have been far more challenged in this regard historically. In the Australian market it’s not unreasonable to expect a team of 3-4 analysts to wear a lot of boot polish travelling around the country and doing deep, fundamental, company analysis, and from this effort develop insight and an information edge that results in alpha generation. In global small caps this clearly becomes a far greater logistical challenge. Even if a manager just focuses on the US there is a far greater number of stocks for a typically sized small cap team to cover. Obviously if you add other geographies this adds workload and complexity.

The past couple of years however, has seen a strong growth in global small cap managers with a meaningful alpha track record available in market. There are likely two main drivers of that. The first is a number of managers have pushed up into the SMID index – which includes mid-caps alongside smaller companies. This has enabled managers to focus more on well established, great companies that are relatively easier to do research and due diligence on, while at the same time still being small enough that they do not have the level of market coverage to make this space especially efficient i.e. alpha is readily available.

The second piece has been managers coming to market with a greater emphasis on quantitative analysis, for the majority if not all of their investment process. This in effect removes many of the workload and logistical challenges as mentioned in global small caps, while still looking to exploit market inefficiencies that are available.

The result of this is that there are reasonable handful of global small cap managers available now with reasonable track records of alpha generation. Our process has identified two standout managers in that regard.

Summary

Consistent alpha generation over the long-term is achievable in the global equities, however, it should never be considered a given or easy. As such defaulting to a low-cost, passive approach has a range of obvious benefits, and perhaps enables you to focus on other important areas of advice and portfolio construction. With that said, we believe that with the right focus and process your global equity allocation can be a source of alpha over time, and that an additional 1-2% p.a. compounded over the long-term makes a significant difference to client outcomes.

*Tracking error is measured as the standard deviation or volatility of excess returns versus a benchmark over time.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. The content of this article is of a general nature only and should not be construed as personal advice. It does not have regard to any individual’s personal objectives, financial situation, and needs. You should consider this information, along with all of your and your client’s other investments and strategies when assessing the appropriateness of the information to your or your client’s individual circumstances. Investment in securities including derivatives involves risks, as securities by nature can rise and fall. Past performance is not a reliable indicator of future performance. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.