Industrial metals have historically held strong correlations with inflation, and with good reason.

In times of economic growth, consumers and businesses tend to feel more confident, and better equipped to spend money – whether this be through the purchase of a new home, car, mobile phone, or through the expansion of a business.

These purchases (which stimulate inflation) generally all require the same input during production – industrial metals.

Industrial metals are utilised in a number of a different ways, with none more prominent in our lives than through the smart phone or computer you may be reading this note on – which generally contain a variety of metals including Aluminium, Iron, Copper, Cobalt and Nickel.

Due to this correlation, industrial metals serve as one of the best performing inflation hedge assets, as well as an important bellwether for economic trends.

In today’s note, we will assess the 4 largest industrial metals, the forces of demand and supply which have defined their performance and the ways in which investors can gain exposure.

This marks the fifth note in our Inflation Series, having already written about:

Copper

Copper was one of the first metals to ever be extracted by humans, used first by the Sumerians for coins and ornaments sometime between 8000 B.C. and 5500 B.C.

In 1886, approximately 100 tons were used to create the Statue of Liberty, which at the time was the single largest use of copper in a structure. Originally, the statue was brown, but due to the oxidisation of the copper, it has since turned into its iconic green colour.

Since then, copper has taken on a myriad of use cases around the world, ranging from electrical equipment (wiring and motors), construction (roofing and plumbing) and industrial machinery (heat exchangers).

Given its broad-based use throughout the economy, copper is known as a leading indicator of economic activity, so accurate that it is often referred to as “Dr Copper” – the metal with a PhD in economics.

Copper has risen 99% in the past year, with the spot price recently reaching record highs due to demand driven by increased levels of manufacturing, primarily in China, who account for 43% of global imports (Reuters 2021).

Increased levels of infrastructure have been driven by private sector investments, fuelled by record low interest rates, and fiscal stimulus measures.

Going forward, demand will be driven by the decarbonisation of economies, with copper serving as a vital component in the production of renewable energy systems, given its position as the most efficient and cost-effective means of conducting electricity.

Demand is expected to be supported primarily by solar and wind power, as well as through the production of electric vehicles (EV), which Max touched on in his recent note.

As with many commodities, prices have also been affected by supply shortages, with the two largest producers, Chile and Peru (who account for approximately 40% of global supply) hit hard by the COVID-19 pandemic, as well as having social unrest and strikes.

Going forward, copper prices will be driven by the level of demand from the renewable energy and EV sector (who could potentially switch towards using aluminium), levels of infrastructure and the ability of supply chains to increase capacity.

Nickel

Nickel is used primarily to make stainless steel and other alloys stronger, and better able to withstand extreme temperatures and corrosive environments. It is used in harsh environments, such as power generation facilities, jet engines and in cookware.

Nickel, like most commodities, has enjoyed a strong past 12 months, rising 46% on the back of increasing demand, particularly through decarbonisation efforts. Nickel serves as a vital component within EV batteries, as well as in wind and solar power generation.

To comprehend the scale of expected demand over the next 10 years, we can look at Tesla’s current goal of producing 20 million cars a year by 2030, where the total nickel required would make up 31% of the global supply in 2019 (Tribeca 2021).

This figure of course does not include other EV producers, with the majority of new car production expected to be in the form of EVs by that point.

With new car production averaging 89 million per year over the past 3 years (Statista), it is obvious that dramatically increased supply would be required to meet this increased demand.

Whilst this assumes that the components of EV batteries would remain unchanged (which they are unlikely to do so), it still highlights the substantial supply gap present, and the price pressures which are likely to occur over the coming years.

Aluminium

Aluminium is one of the most diverse metals, used in a variety of ways due to its qualities of being lightweight, strong, corrosion resistant, durable and malleable.

Positive for the environment, but negative for spot prices, it is also 100% recyclable, and takes only 5% of the energy to recycle scrap aluminium, then what is required to produce new aluminium.

As with other industrial metals, aluminium has performed strongly, up 66% over the past year, with prices surging to multi year highs on the back of increased economic activity. Given its broad applications, in its use in transportation, construction, electrical equipment and consumer goods, demand will continue to rise as economic activity picks up.

Supply curtailments in China have also driven prices up, with their transition towards cleaner energy forcing the shutdown of production in Inner Mongolia, with fears of further production restrictions in the Xinjiang region.

Iron Ore

Approximately 98% of iron ore is used to make steel (Geoscience Australia), which is used widely in the construction of buildings, infrastructure, trains, cars and electrical appliances to name a few.

As Australians, we know more than anyone about the iron ore story – in the past year it has risen 152% and has provided a much-needed boost to Tuesday’s federal budget.

Prices have been primarily driven by increased demand out of China and supply shortages from Brazil, with the Vale tailings dam disaster in 2019 prompting mine closures for safety checks.

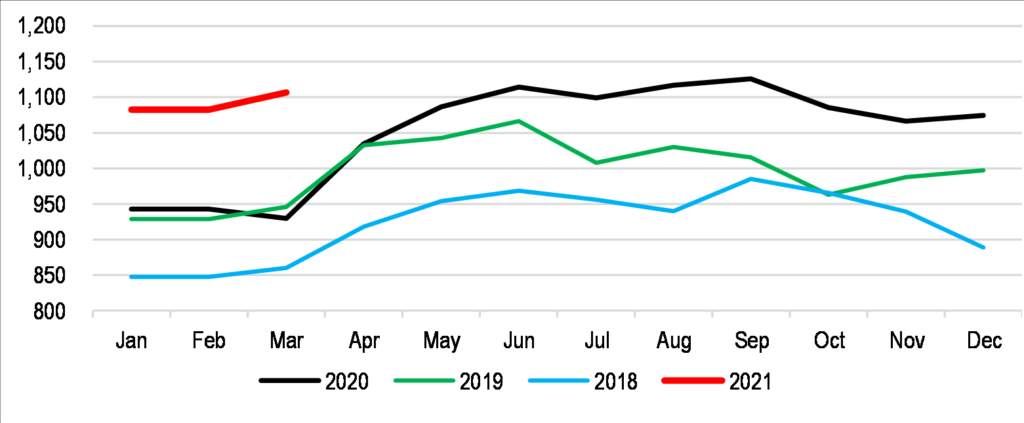

In the short term, valuations will continue to be driven by Chinese demand, which increased 19% YoY in March, and is forecast to grow by 3% in 2021 (JP Morgan).

Chinese annualised steel production

However, as Darren recently touched on in his Iron Ore note, Chinese environmental policy will likely curb demand over the medium-long term, with goals of peak steel emissions around 2025, and increased usage of scrap metal as opposed to iron ore. Moreover, if Brazilian supply continues to recover in line with guidance, price pressures will continue to be driven downward.

How to Get Long Industrial Metals

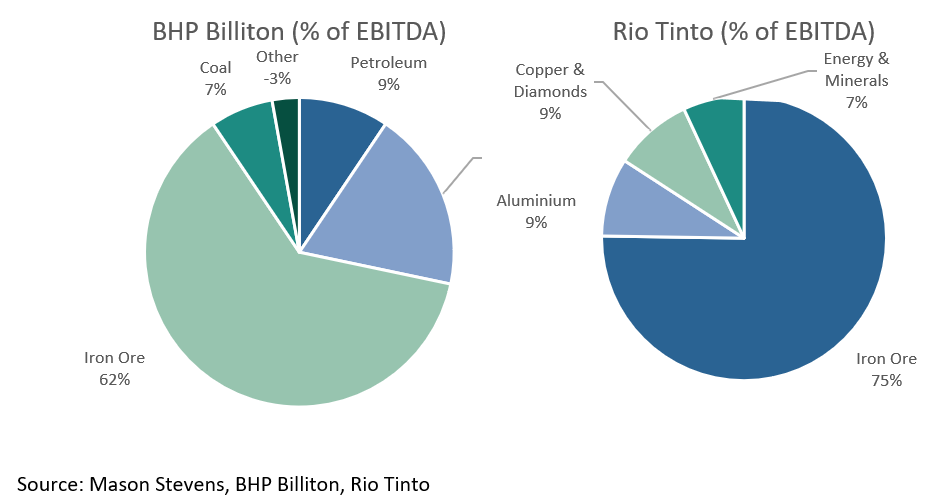

Whilst diversified miners like BHP and RIO have become a mainstay in equity portfolios, investing into a thematic or a specific commodity has been less common.

Investors can elect to gain exposure to specialised miners, like Fortescue (ASX:FMG) or Nickel Mines (ASX:NIC), however geopolitical risks and production capabilities (whether they produce low grade or high grade outputs) must be taken into consideration during security selection.

Investors can also deploy funds into diversified exposures such as BHP Billiton (ASX:BHP) and Rio Tinto (ASX:RIO), both of which derive revenue from a variety of resources.

Whilst both companies are not pure play industrial metal investments, they stand as some of the largest miners in the commodities they choose to mine.

Investors can also gain exposure to the underlying commodities themselves, through investing into ETN’s which invest purely in the futures markets, such as:

- iPath Series B Bloomberg Copper Subindex Total Return ETN (NYSEARCA:JJC)

- iPath Series B Bloomberg Nickel Subindex Total Return ETN (NYSEARCA: JJN)

- iPath Series B Bloomberg Aluminum Subindex Total Return ETN (NYSEARCA: JJU)

- Invesco DB Base Metals Fund (NYSEARCA:DDB)

It must be noted that as these ETN’s invest directly into futures markets, investors may be subject to contango or backwardation, where the forward price of the futures contract may differ to that of the spot price.

Given the variety of market and commodity specific risks, it is important for investors to understand the forces at play within their selected exposures.

Each industrial metal offers a different risk and return dynamic, with different sources of demand determined by their present and future use cases, and varying supply related factors, such as geopolitics, new mine establishment costs and environmental disasters.

In understanding these respective factors, one can better align their security exposures with their perspective on the global economy and have more informed decision making when entering or exiting a position.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.