Gold has been used as a store of wealth since 700 BC when Lydian merchants began producing gold coins.

Since then, the world has changed dramatically and with it, the utility of gold. Gold however, can still be used to maintain an individual’s purchasing power, and potentially diversify investment portfolios.

Whilst demand for gold is led by several factors, it often performs well in periods of high inflation and risk-off markets. That being said, in our view, there is room for physical assets in portfolios during most stages of the cycle.

Gold differs from many other assets, in so far as it is not income paying. Its pricing is derived through the benefits of owning the asset for diversification and speculation rather than demand for the physical assets underlying use in jewellery and circuitry.

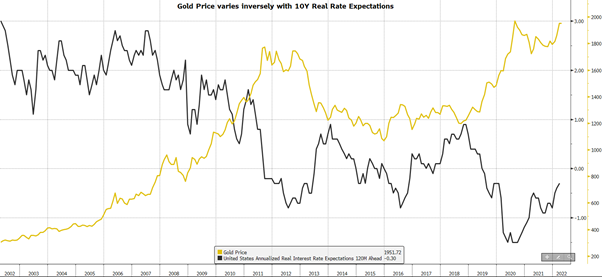

Importantly gold tends to exhibit an inverse relationship with real interest rates due to the opportunity cost borne by the lack of income generation.

Source: Bloomberg, as at 21/April/2022

Where is gold sitting currently?

We saw a strong rally in gold from the start of the COVID-19 pandemic as it thrived on the uncertainty and investors looked to protect their portfolios.

The price retreated in 2021 as real yields began to increase from negative levels. Additionally, investor sentiment increased with COVID vaccines, economies reopening, and a strong rally in global equities.

Despite the fact that real yields continued to increase, the start of 2022 saw gold spike once again with a risk-off sentiment due to the Russia-Ukraine war, high levels of inflation and the fears of a possible incoming recession.

The most notable of these risks is the uncertain duration and severity of the Russia-Ukraine war.

Impact of Inflation

The topic on everyone’s minds now is inflation.

You only need to go as far as the supermarket or petrol station to experience it.

There is supply-led inflation from multiple sources including the dramatic increase in the price of oil and worker shortages in industries depleted by lockdowns.

The US is currently experiencing the highest level of inflation since 1982, with CPI increasing 8.5% Y/Y from March figures.

Australian inflation is yet to be reported for this quarter, but the last reading was an increase of 3.5% Y/Y.

Analysis from the Perth Mint shows “the gold price in Australian dollars has on average risen by just over 20% in nominal terms in years local inflation was 3% or higher.”

How much will this inflation affect the price of gold?

Whilst inflation is high relative to the experience of the last decade, we are also experiencing a shift in monetary and fiscal policy.

The Fed have moved to a hawkish stance and have clearly shifted from an easing policy to a tightening policy, with many other central banks expected to follow suit.

In March, the Fed increased the Fed Funds Rate from 0-0.25% to 0.25-0.5% band, and current market pricing is for further increases of 2.25% over the remaining 6 policy meetings of the calendar year.

The rapid pace projected for these rate hikes is an attempt to stabilise inflation and inflation expectations as well as remove the emergency accommodation policy response to the COVID-19 pandemic.

In our view, stability in financial markets and an increase in real yields are both potential negatives for the price of gold.

This effect is twofold as a rise in real interest rates also increases the opportunity cost of holding gold which already provides no income and has a carry cost due to storage and insurance.

Gold as an indicator

Another reason to focus on gold in the current climate is as an indicator on the health of the economy.

There are several key indicators derived from the gold price, one of which is the copper-to-gold ratio.

This may seem like a rather strange metric to use as an economic indicator, but when broken down its use is very apparent.

Demand for copper is highly sensitive to changes in economic activity and gold, and as pointed out earlier, thrives on uncertainty in the markets.

Copper is a primary material in many industries including automotive, industrial and transport. Because of this, as economic activity picks up, the demand for copper increases. As economic conditions deteriorate, economic activity decreases, projects are put on hold or cancelled forcing raw material orders to do the same and so the demand for copper will decrease.

The ratio can be used as a leading indicator of the health of the economy as it compares growth to risk. It has an inverse relationship with US Treasury bonds and has proven to provide indications of recessions in the past.

Historical copper/gold ratio with recession bands

Source: Bloomberg

Closing Remarks

At current levels gold is close to peak levels of the last twenty years. Not surprisingly the sector has outperformed materially in the recent past. For those investors who have enjoyed this rally, now may be the time to consider taking some profits.

The most likely catalyst in our view for gold to rally from here would be risk lead, such as a supply shock or demand shock. From a geopolitical standpoint clearly escalation of the Russia/Ukraine war could also be another key driver of outperformance.

Source: Bloomberg

For those investors who would like an ETF Gold exposure our preferred instrument is VanEck Gold Miners ETF(GDX.ASX) for producer exposure or GOLD.ASX for the asset itself. For individual stock options, the two largest on the ASX are NewCrest Mining(NCM.ASX) and North Star Resources(NST.ASX). JP Morgan has an overweight rating on NCM and neutral on NST.

Regardless of your thoughts on investing in gold at this time, it is useful to keep an eye on its price and metrics derived from this as a guide to market conditions.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.