Co-Authored by Jacqueline Fernley, Chief Investment Officer & Liam Montgomery, Dealer

In an environment where higher inflation is more sustained, protecting and then growing the purchasing power of capital becomes the focus of portfolio positioning.

Equities are a claim on nominal growth and can therefore perform well in this environment, as long as hyper-inflation does not ensue.

With that said we continue to suggest investors’ focus on quality as a style as these businesses are more likely to be able to pass on higher input costs.

Inflation can be harmful particularly to some fixed income instruments.

Many investors buy fixed income securities because they want a stable income stream, which comes in the form of interest payments.

However, because the rate of interest, or coupon, on most fixed-income securities remains the same until maturity, the purchasing power of the interest payments declines as inflation rises.

Inflation can also adversely affect fixed-income investments in another way.

When inflation rises, interest rates also tend to rise.

When interest rates rise, bond prices fall.

Thus, inflation may lead to a fall in bond prices, potentially reducing total returns on bonds.

Consequently, in a rising inflation rate environment fixed rate bonds are unlikely to provide the ballast in an asset allocated portfolio, however, floating rate notes and inflation linked bonds can provide some protection in this environment.

In times of higher inflation, real assets can offer investors positive real returns, given often these assets have revenue which have automatic inflation protection.

Real assets as an asset class can therefore provide diversification and compelling real returns.

Therefore, as the topic of today’s note, we will explore the three main categories of real assets – real estate, infrastructure, and commodities; and the roles which they can play within investor portfolios.

Real estate

Unlike traditional investments, real estate assets are tangible: office buildings, warehouses, residential housing and stores.

Real estate helps to offer protection against inflation, as rental yield will often rise, especially in the case of commercial real estate where pricing escalators are often CPI + x%.

Therefore, in periods of high inflation you’re providing yourself with protection against inflation as inflation is inherently tied into the assets value.

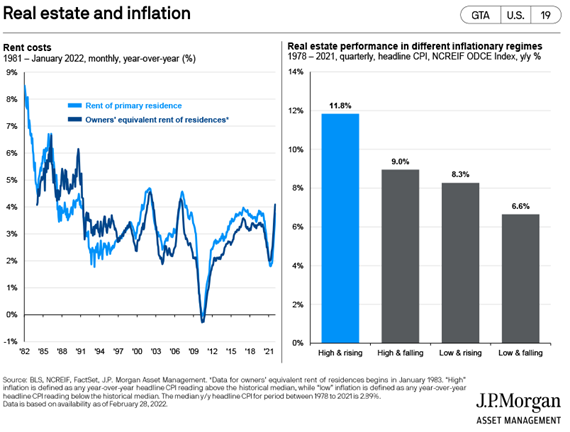

The chart below from J.P.Morgan Asset Management shows the historical relationship over time of rental yields and real estate performance through different inflationary regimes.

Chart 1: Real estate in inflationary settings

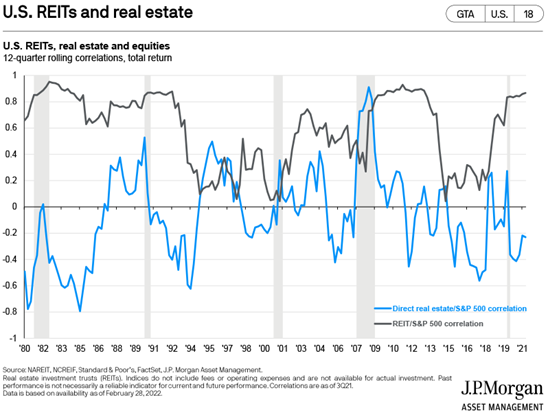

Importantly when accessing this asset class for correlation benefits, direct real estate provides the best source of non-correlated returns versus the list REIT sector as shown in the chart below from J.P. Morgan Asset Management.

Chart 2: Correlation between REITs and direct real estate

The nature -of the real estate asset universe is that REITs encompass some of the best ways to expose your portfolio to more direct income from real estate bar holding the properties yourself, unfortunately, this does mean that they have a higher level of correlation with the listed equities market.

Prologis (PLD:NYS) & Equinix (EQIX:NAS) offer single stock international exposure, while Goodman Group (GMG:ASX) & Scentre Group (SCG:ASX) offer domestic non office REIT exposure. These names are currently rated BUY from Citi and Goldman Sachs.

Exposure to these are also available through ETFs such as the Vanguard Real Estate ETF (VNQ:ARC) & the Vanguard Australian Property Securities Index ETF (VAP:AXW).

Managed fund exposure can be sourced through the Quay Global Real estate Fund (APIR:BFL0020AU).

With that said our preferred exposure is via direct property deals rather than listed instruments given the correlation benefits.

Infrastructure

Infrastructure investing is becoming foundational in investment portfolios, providing opportunities for lower volatility returns that historically have low correlation to equities and bonds.

Globally governments have pledged their commitments to transitioning to a lower carbon world. Significant capital is finding its way into infrastructure as a consequence, especially renewable energy. This capital trend is also shifting toward social assets, essential services, waste management and other core infrastructure assets.

We expect core infrastructure assets to continue to serve as a lower-risk, more forecastable source of diversification and steady income (most from cash distributions) through their regulated frameworks, often correlated to inflation, government concessions and long-term contractual revenues with investment grade counterparties.

Infrastructure provides an opportunity for steady income through market cycles since the phase of an economic cycle generally doesn’t change water or electricity consumption.

Infrastructure assets are a way to gain exposure given their similar characteristics to that of fixed income in terms of their income stream.

Their necessity to society in the forms of utilities & transport mean they are valuable when looking to diversify a portfolio using real assets.

Historical performance of unlisted infrastructure funds highlights that annual returns on average nearly match that of equities while providing it at a significantly lower level of volatility and very low correlation to equities as well.

In the case of listed infrastructure, it’s evident how the impact of inflation has and will continue to be a tailwind to sector.

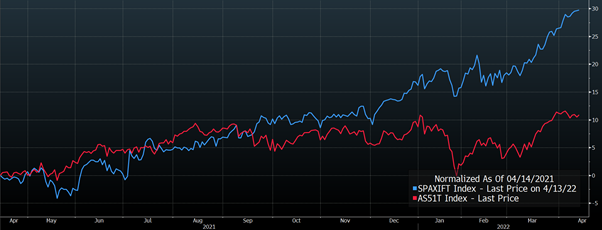

The below chart depicts the S&P/ASX Infrastructure total returns index (SPAXIFT) vs the ASX200 total return (AS51T).

What you can see, over the past few months as inflationary pressures have continued to rise with the SPAXIFT Index benefiting immensely from this, leading to significant outperformance when compared to the ASX200.

Chart 3: 1-year performance of SPAXIFT vs AS51T

Source: Bloomberg as at 14/04/2022

To gain exposure in the infrastructure space Transurban (TCL:ASX), and wider exposure can be gained through the iShares Global Infrastructure ETF (IGF:NAS). TCL is issued with a rating of buy at UBS.

The Lazard Global Listed Infrastructure fund (LAZ0014AU) is one way to gain exposure through managed funds.

Commodities

Historically, commodities have been one of the strongest performers during periods of low and rising inflation and are therefore often used to protect portfolios from the effects of inflation.

Commodities can be looked at in two different baskets, either hard or soft commodities.

Soft commodities are mainly food and agriculture related and will be the topic of a future note.

Hard commodities include energy, industrial and precious metals.

Within this note we focus on industrial metals as we will feature precious metals and gold in the coming weeks.

The interesting topic for debate is the impact the transition to a carbon-neutral world will have on the behaviour of commodities.

As climate change policies take priority, the demand outlook for industrial metals, such as copper, aluminium and lithium has improved.

For ESG focussed investors who choose to limit their exposure to energy, then industrial metals exposure may provide the inflation protection desired.

Gaining exposure in industrial metals can be done through diversified miners like RIO:ASX. Whilst they are not a straight industrial metal play, they still stand as one of the largest miners in the metals they do mine.

More extensive lithium exposure can be found in Pilbara Minerals (PLS:ASX), Allkem (AKE:ASX) or through the Battery Tech & Lithium ETF (ACDC:AXW). Lynas Rare Earths (LYC:ASX) also offers further exposure in the metal’s universe.

Exposure in a more direct form can be found through ETNs which invest purely in the futures markets:

- iPath Series B Bloomberg Copper Subindex Total Return ETN (NYSEARCA:JJC)

- iPath Series B Bloomberg Aluminum Subindex Total Return ETN (NYSEARCA: JJU)

Diversification

In conclusion, the benefits of investing in real assets are that they can provide stable income streams which are in part inflation protected. The diversification benefits that real assets can provide investors better risk-adjusted returns as a result of the low correlations with equities and bonds.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.