Soft commodities generally refer to agricultural goods that are grown, rather than extracted from the ground.

“Soft” referring to the tensile strength in comparison to harder commodities such as gold, platinum (precious metals) or iron, nickel and cobalt (industrial metals).

Truth be told, soft commodities are a subset of the commodity asset class that are less traded due to supply-chain nuances that provide significant insider knowledge, where industry insiders have more edge in trading and investing.

For example – what’s your edge in coffee bean markets compared to producers and suppliers of the product?

This relationship holds true, until times of stronger inflationary pressure – times like these.

This is our fourth note in our Inflation Series, having already written about:

We’re conscious that inflation is being seen in certain goods, and many of these are soft agricultural products.

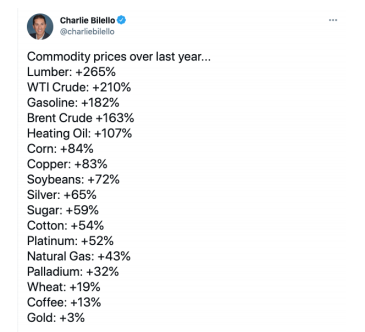

In the first note of the series on Inflation-linked bonds, we shared the following screenshot from Twitter, where ~half of the listed commodities are softs, that have appreciated greatly in the last 12 months.

You may look at this and think you’ve already missed the boat.

Here’s how the latest move looks in long-term context, where we chart the price of the Bloomberg Commodity Index (BCOM) over 60 years:

See that small uptick at the far right of the graph?

That’s it.

We’re a long way from the gains see in the 70s or 2005-2007 period.

Why Soft Commodities?

Softs commodities are as we originally stated – they’re generally “grown” commodities such as coffee, sugar, corn, wheat, soybeans, fruit (and juices) and livestock.

They’ve received less investment in recent years due to underperformance with respect to hard commodities, due to Chinese government infrastructure building initiatives, which have seen iron ore, steel, coal, copper, nickel and lithium out-performing.

The difference is that in 2021, price inflation and expectations of future inflation (higher prices) is based on consumer led demand, where households have received higher incomes due to stimulus, and stockpiled cash in the form of savings to weather the pandemic.

Now that we’re emerging on the other side of the pandemic, those savings may be reduced and the stimulus monies spent and most importantly, all at once when business inventories (supplies) are low.

This conflation of aggregate demand with reduced supply is already being felt in areas such as lumber, which Mike detailed in his lumber note on 3 May, but also in areas such as pet food as well.

If you remember the sudden surge in demand for toilet paper in Australian stores in March/April 2020, this scenario is of a similar nature, albeit less panicked than last year.

How to Invest?

There are three main ways to invest in soft commodities, with two more suitable to retail investors than the other (futures).

- Listed futures contracts

- Direct equities (think Bega or Inghams)

- ETFs and Managed Funds

Those are through listed futures – the realm of bank and hedge fund trading desks, agriculture sector corporates and farms; or through direct equities that have revenues from soft commodities (think Bega) or from ETFs and managed funds that provide exposure through fund structures.

Thematic ETFs

There are many ETFs that can provide exposure to the broader soft commodity industry:

VanEck Vectors Agribusiness ETF (NYSX: MOO) is a go-to of mine, whose performance is derived from agri-chemicals, livestock, fertilizers, seed and grain cultivation, and farming equipment. As at 31 March, its main exposure was to the USA (~56% of total exposure), which is a key recipient of the pent-up demand element, driving their prices higher than in other countries.

BetaShares Global Agriculture ETF (ASX: FOOD) is another ETF that tracks agricultural companies (ex-Australia), currency hedged. It provides a different type of exposure compared to MOO, with greater exposure to packaged food and meat, food trading companies and agricultural products.

In less detail, there’s also many commodity specific ETFs and ETNs available in US markets:

- Teucrium Corn Fund (NYSX: CORN)

- iPath Coffee Subindex Total Return ETN (NYSX: JO)

- iPath Sugar Subindex Total Return ETF (NYSX: SGG)

with many more available for those willing to look.

Managed Funds

If you’re more interested in Australian active fund managers, then we’ve recently interviewed Steve Jarrott, portfolio manager at Warrakirri, on our Mason Stevens Morning Call.

Warrakirri Diversified Agriculture Fund is a unit trust structure that could be seen as a nuanced agricultural property related investment, where the underlying exposure is to lease terms and agricultural tenants, producers of nuts, fruit vineyards, and livestock etc.

Direct Equities

If you’re more of a stock picker, then the ASX has a large range of companies with majority of revenues derived from agriculture. To name a few of the biggest:

- Incitec Pivot (ASX: IPL)

- Graincorp (ASX: GNC)

- Nufarm (ASX: NUF)

- Costa Group (ASX: CGC)

- Inghams Group (ASX: ING)

- Elders (ASX: ELD)

- Australian Agricultural Company (ASX: AAC)

- Select Harvests (ASX: SHV)

- Webster (ASX: WBA)

- Ricegrowers/Sunrice (ASX: SGLLV)

Closing Remarks

As an investor, I’ve always ascribed to the philosophy that it makes sense to invest in things that you regularly spend money on, with a certain portion of your portfolio allocated to growth areas that you’ll likely spend money on in the future.

From that perspective, soft commodities are a growth area where consumers are exhibiting pro-cyclical behaviour by increasing the rate of change in their consumption, coming out of a pandemic and recession.

And while we’re already seeing supply-chain disruption and under-supply, there’s an asymmetric return profile where prices could spike off a low base, where soft commodities provide rock-hard gains.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.