In our FX outlook for 2021 published on 14 December 2020, we outlined that the USD would likely remain one of the most influential macro-economic factors for 2021 calendar year, due to its reserve currency status, dominance as the settlement currency for international trade and ability to affect the global price of money.

In that outlook we detailed how the USD acted as a safe-haven asset during H1 2020, as investors moved quickly into US treasury bond markets, which slowly receded during the remainder of the year as structural forces such as budget deficit spending, trade deficits, relative terms of trade and interest rate differentials returned as the main factors affecting currency exchange rates.

This risk-off/risk-on narrative returned in early January after the US Senate elections saw a “Blue Wave” outcome eventuate, which further extended the fears of a US sell-off from increased budget deficit spending.

So far so good for our outlook, where AUD/USD briefly touched 80c in early February and has continued to trade in a 76-78 cent range ever since.

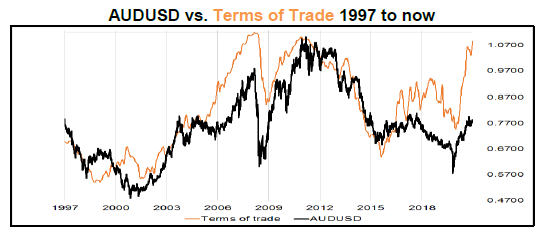

Terms of Trade

If the USD is still on a downward trajectory because of the twin deficits (budget and trade deficits) and where the increasing money supply is also seeing the USD being sold and reinvested around the globe, this sees the “terms of trade” increase in other nation’s economies that have material exposures to export industries.

Terms of trade refers to the ratio of export prices to import prices, where an increasing term of trade implies that a nation is receiving relatively more money for its exports, relative to its imports.

In Australia’s case, we generally have a rising terms of trade when our main exports – iron ore, mineral fuels, precious metals, meat, education, tourism – rally relative to other areas of the economy.

This makes intuitive sense where if Australian exporters are receiving more funds for their goods and services with respect to importers, there’ll be more buyers of AUD than sellers; which also becomes a self-fulfilling prophecy because fund managers and trading desks know of this relationship and so look to get ahead of it, making it come true.

Hence, a rising Australian terms of trade – or even an expected rising ToT – would normally be a buy signal for AUD/USD in the past.

However, this time around Australia’s terms of trade hasn’t seen a sharp increase in the AUD/USD exchange rate, which if it had, would see AUD/USD closer to 85-95c, rather than 76-78c.

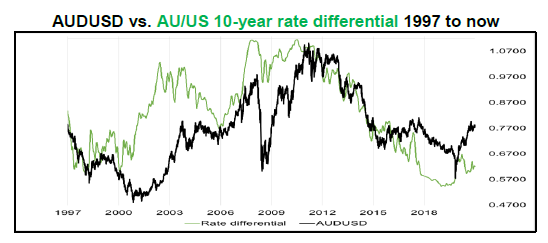

Interest Rate Differentials

The break-down in the relationship has only started occurring since March 2020, where the RBA began intervening in the Australian bond market through an asset purchase program, buying government bonds.

During this mid-month announcement, the RBA established the program to support this key asset class, by pegging 3-year government bond yields at 0.25%, which was later reduced to a target yield of 0.10% – both times to align the 3y government bond yield with the Overnight Cash Rate (OCR).

While this policy was effective in restoring trading activity to the Australian government bond market, which in-turn assisted the Australian corporate bond market, it has muted the transmission of fiscal and inflationary indicators within the economy.

Because the RBA’s asset purchase program is keeping Australian government bond yields artificially low, there’s been a muted transmission from the terms of trade leading to higher Australian bond yields.

Therefore, our outperformance in selling our export commodities abroad has not seen a move higher in bond yields, but also our AUD.

We view this below in comparing the AUD/USD exchange rate against the interest rate differential between Australian and US 10-year government bonds.

Normally, the rise in terms of trade would see higher prices lead to higher inflationary pressure, in turn leading to higher bond yields to compensate for the inflationary expectations.

This creates what is called a “carry trade”, where global fund managers will buy foreign currencies that earn them higher carry (income) compared to other currencies. This was all the rage in the 90s and 00s when currencies such as AUD, NZD, CAD, NOK were all high carry compared to USD, CHF or JPY.

Because the RBA is manipulating Australian bond yields lower, the interest rate differential is still quite close.

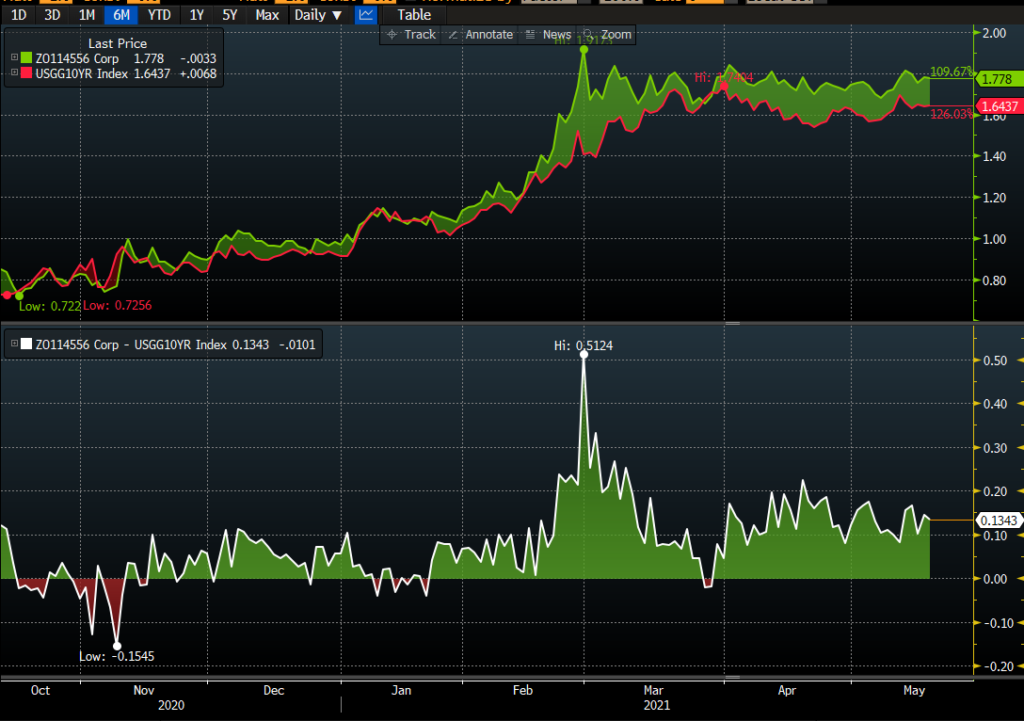

To look at this in closer detail, the below chart compares both AU and US 10-year government bonds (top panel), and the spread between them (bottom panel).

It’s no surprise then that when the AUD/USD reached its recent high of 80c, it was due to a recent high in the yield differential of 0.51%, in late February and early March.

Since then, the RBA has intervened with more bond purchases to flatten the Australian yield curve, promising more quantitative easing to come in their March 2021 policy meeting, which saw yields lower and the AUD/USD trade within the current 76-78c range.

Where to from here?

It becomes more obvious that the trajectory of the AUD/USD exchange rate is predicated on our relative central bank policies, where the RBA has been actively buying large portions of government bonds, to mute the possibility of a higher AUD.

This is also in keeping with their 1st mandate, to contribute to “the stability of the currency of Australia.”

In doing so, they are fulfilling their 1st mandate but also ensuring that a higher AUD doesn’t cause them to miss their inflation targeting goals as well.

That’s why it’s likely we see the RBA continue their dovish monetary policy, in response to the continued policy support from other global central banks, particularly the US Federal Reserve.

This will see the RBA extend their asset purchase program, likely for another 6 months but at a diminished amount, and only look to taper off completely when other central banks are doing so.

However, they may also seek to taper sooner, if we realise higher than expected domestic inflation through wage increases, though this remains unlikely.

This is why we expect that AUD/USD trades within a confined trading range of 76-79c until there’s sufficient central bank catalysts to move the AUD higher, or the USD materially lower.

We would expect the AUD to slowly appreciate towards an 80c level, and even higher, should the RBA look to taper their monetary policy accommodation, if inflation is seen to be above the target band for a prolonged period.

This is also why we’re continuing to remain hedged a large portion of our foreign currency exposure, where the AUD is the likely outperformer – depending on the currency pair.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.