About ten years ago, a mentor of mine told me that bond markets are not supposed to be exciting.

That instead, they were meant to highly mathematical, detail-oriented markets for calculating lending rates to facilitate capital transactions between those with surplus capital, lending to those in deficit.

The basis for this point of view is that an exciting bond market is gyrating to sentiment and suggests a rapidly changing macro-economic circumstance, where returns may be positively or negatively impacted.

When we last provided detailed coverage of RBA cash rate pricing on 4/March, bond markets were as interesting then, as they are today. Quite a bit has changed in four days!

In that previous update, Russia/Ukraine had become influential for pushing bond yields down, whilst sustained inflation and the likely reaction function of central banks was the other key dynamic influencing yields.

The crux for Australia was that as a fairly small economy, our markets are heavily influenced by international factors, often ignoring our idiosyncratic differences.

Hence, when the market priced in an aggressive hiking cycle for the US Federal Reserve in response to >7% y/y headline inflation, it was no surprise that the Australian cash rate pricing began to rise almost in tandem.

The problem with this was that the market was ignoring the stark differences between Australian and US inflation pressures, which should result in a differently shaped yield curve, and different central bank responses.

Fast forward from last update to today, the dynamic hasn’t changed.

US cash rate expectations have increased even more, as have Australian, pushing bond yields even higher.

Pathway for the RBA

In the RBA’s latest Policy meeting on Tuesday, the RBA changed their tone by removing key references, which the market gauged as being decidedly more hawkish.

In particular:

- Dropped the “patient” references which had persisted for the past 4-5 meetings

- Final paragraph removed the long-cited commitment “to maintaining highly supportive monetary conditions.”

- The shift in tense from present to past infers the Board has already met one or more of its objectives

These changes notwithstanding, the Bank did retain their tentative commentary, where labour costs are forecast to pick up in a gradual fashion, over the coming months.

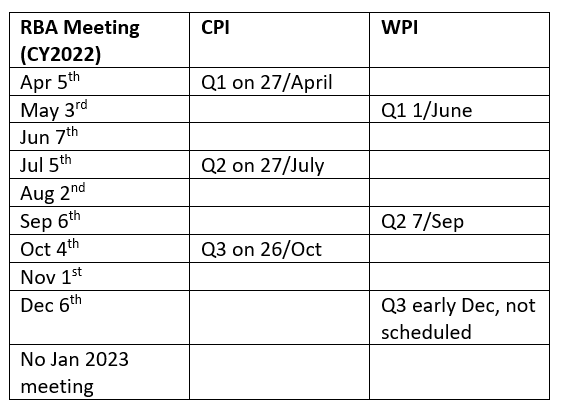

In terms of what that looks like from a data release calendar, the RBA is going to be focusing on the following key data releases, regarding both CPI and Wage Price Index (WPI):

Source: RBA, ABS

And therein lies the pathway for markets to price in (or not) RBA rate hikes for this year.

If Q1 CPI shows a continuance of the already higher-than-target inflationary pressure, a “sustained” pressure, this might be the green light required for the RBA to begin hiking in coming months.

If you’re in this camp, then the RBA’s May meeting is likely too soon, and they’d likely give some notice of impending rate hikes, signalling their June meeting as lift off.

If Q1 CPI isn’t enough to show sustained inflationary pressure, then likely we need to wait for the WPI data released on 1-June, where June 7th may either be a live month, or the RBA waits instead for July.

And if CPI and WPI aren’t red hot?

Then September-November becomes the live meeting.

RBA Pricing

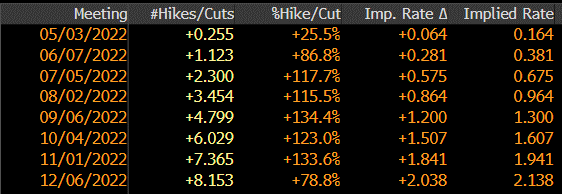

As for RBA cash rate pricing?

The market currently has forecast an increase of the cash rate from 0.10 to 2.15% by calendar year end.

Given the number of meetings in the RBA’s 2022 schedule, this would imply a near-certainty of a rate hike in June after a strong Q1 inflation print later this month, and then 25-50bp of rate hikes in every single meeting until year end.

Or in total, +204bp of rate hikes forecast this year alone.

Source: Bloomberg, as at 6/April/2022

Quite a Backflip Predicted

This pricing contrasts with RBA forecasts published in the past 6 months, where the RBA underestimated the strength of the labour market rebound, as well as the higher wage price increases across both public and private sectors.

Considering where we started this year, the RBA had all but ruled out rate hikes in CY2022, where H2 2023 was considered the most likely time when conditions would be met.

For the RBA to begin hiking in June after no action to date, and then hike rates by ~200 bps in a six-month period, would be a staggering blow to their credibility, as well as a mental backflip.

For me, this would be a capitulation of the previous SoMP projections, and possible disregard of their well-regarded models that they’ve used for years.

OR

The market pricing may be too aggressive, using the US Fed’s rate hiking projections and then overlaying on the Australian market.

The latter sounds more credible in our view, where the RBA may well hike the cash rate to 2.0%, but less likely they do so in a 6-month period, where they don’t seem to be in a hurry. It is more likely in our opinion that they take a more considered approach over 12-18 months given Australian trimmed mean inflation isn’t drastically above their target level.

Investor Outcomes

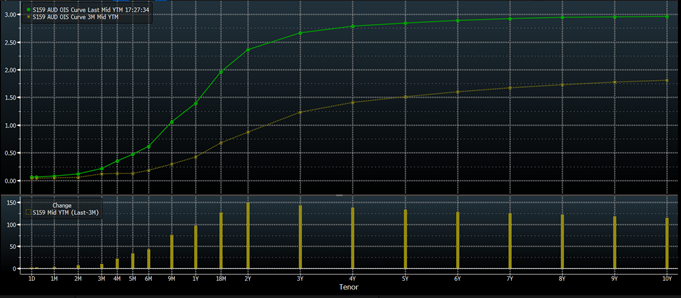

Looking back to look forward, the market has moved to price in an additional 70bp of rate hikes in the coming 6 months, compared to three months ago.

Over the next 2 years, an extra 150bp of rate hikes.

Source: Bloomberg, as at 6/April/2022

This eventuality is the reason we’ve spoken about bond markets far more this year than most years, where we’ve sought little to no interest rate duration (sensitivity), to not be adversely affected by higher bond yields (lower bond prices).

However, we’re finding we now disagree with market pricing, that rate hike forecasts are too aggressive, where the RBA is likely to be far slower and cautious in their hiking cycle than interest rate derivative and bond markets are pricing.

With this in mind, it’s likely that 18m-2y and possible 3-4y bond yields are slightly too high, where the average cash rate during that period will in our opinion be lower and therefore we expect yields in the “mid curve” to lower. For a retail investor this would imply buying fixed rate bonds in line with these tenors.

For a case study, for a portfolio I manage we recently purchased CBA’s latest Tier2/Subordinated AUD bond issue at primary tender, a bond callable in 5 years (April 2027), paying a fixed-rate coupon of 4.95% p.a.

This purchase was in part the high rate of return for a CBA AUD subordinated bond, where over a 5-year period one would expect 5y * 4.95% p.a. = 24.75% cumulative cash yield over the time frame, but also in part an articulation of the view that too aggressive cash rate forecasts (too high too soon) should see those “mid curve” bond yields slightly lower as well.

Moreover, this bond would be even more compelling if you believe that RBA pricing has gone too far and the cash rate may never move above 2% for the coming 1-2 years, let alone to 3% over the coming 3-4 years.

[Noting credit bond investing is far more involved than this simplified case study]

Closing Remarks

It’s likely the bond market remains “interesting” for most of this year, as price pressures remain elevated and investors seek higher compensation to maintain their purchasing power.

The RBA is caught in a unique situation where the market has priced in significant cash rate increases with little negative property, equity or FX market reaction so far, that could allow them to increase rates to more normalised levels, faster than they would have otherwise.

Maybe not 2% in 6 months, but a good way there.

However, like all institutions they will seek to maintain their credibility and likely keep using their own economic models, and not deviate too dramatically away from them, which will see rate hikes currently forecast to be pushed back or annulled entirely, bringing bond yields in the “mid curve” back down.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.