One of the equity rotation plays of Q1 2021 was a shift from growth to value, which somewhat reversed over Q2 and Q3 as bond yields fell steadily as COVID-19 third wave infections grew.

As Mike noted yesterday, what we’ve seen during this reporting season has been the clear outperformance of growth over value, continuing the bond yield narrative as yields have fallen and had little reason to rise.

Certainly, when global central bankers are taking a softly-slowly approach to removing emergency monetary policy accommodation, then we’re not just in a “lower for longer” situation, but also in a “slower for longer” environment*.

As your scribe to provide today’s Utilities market update, I literally volunteered as it’s a particular industry that I resonate with, where the long lasting thematic of utilities has been their bond proxy like returns, and more lately, a thrust to decarbonise.

Before I jump into the utilities sector in depth, first I’d like to highlight that this is our fifth reporting season missive, where we’ve previously covered:

Utility in Portfolios

The utility sector is composed of four sub-industries: electricity, gas, water and multi-utility.

Historically there was a fifth sub-industry, independent/renewable, which has become an antiquated notion as renewable adoption has become mainstream and deeply embedded within nearly all energy supply-chains, with greater impetus going forward.

For this reason, it’s no surprise that earnings results featured progress towards renewable energy and talk of lowering carbon emissions and “net zero” targets.

I took note earlier this year when Ausnet (ASX: AST) reported their results noting that to have any chance of meeting Paris carbon reduction targets, our energy grid would need to electricify and decarbonise.

That new wind and solar farms would need be connected to the grid, and that the grid itself would need upgrades to become more resilient to accommodate the intermittent nature of some renewable energy generation, where this unregulated business is a growing component of many utility companies.

Otherwise, one of the main features of utility companies is their bond like (proxy) returns, where they’re generally large companies with large amounts of debt/equity, funding hard infrastructure assets, operating within government regulated networks with reasonable barriers to entry and with limited competition.

Because of this, utilities tend to behave similarly to bonds, paying regular dividends that investors can harness for income, though with less certainty of payment and yield compared to bonds.

[Flippant sidebar: I’d call them “not as fixed, income”]

There are currently 24 companies listed in the utilities sector of the ASX, with the largest (>1bln market cap) being well established names such as APA Group, Mercury NZ, Origin Energy, Ausnet, Meridian Energy, Infratil, Spark, AGL, Genesis Energy and Contact Energy.

We’ve chosen to focus on two in particular today, as our proxies, APA Group and Origin Energy.

Bond Like Returns

Focusing on this first, as it’s one of the historical prime ordinances for utility industry investment, dividend yields in Australia are far above bond yields.

As a fixed income investor, it’s something that I’m continually cognisant of as a 5-year government bond yield ~0.62%, 5-year major bank issued hybrids at ~2.8-3.2% and corporate bonds in between those two ranges.

Hence, utilities offering 5%+ is quite a step up compared to bonds, where large swathes of investors will accept the higher level of capital price volatility in return for the higher income compensation.

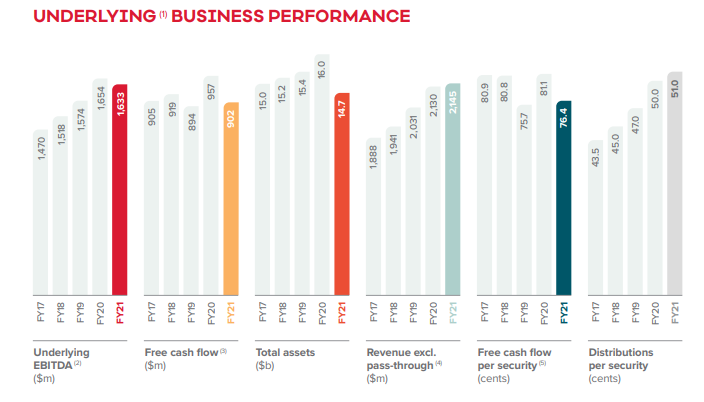

Looking at APA Group (ASX: APA), it owns and operates natural gas and electricity assets domiciled in Australia, and it’s our largest domestic natural gas business and our largest utility by market cap.

When APA reported their FY2021 results on 25 August, they reported 2.14bln AUD of revenue, up 0.7%, though EBITDA fell to 1.63bln (-1.3%), having invested in “strategic development”, and was paying higher insurance and compliance costs than the previous year.

APA is paying a distribution of 27c/share, bringing total FY distributions to 51c/share, up 2%, where dividends have been continually growing these past five financial years.

Using APA’s share price yesterday ($9.32/share), their current dividend yield is 5.47%.

Source: APA FY2021 Annual Report

Within the ASX, there are few other choices of similar yield, including Origin Energy (4.44%), Stockland (5.37%), GPT (5.53%), Charter Hall (5.62%) – whilst SGP, GPT and CLW are not utilities, they provide similar style income-focused returns.

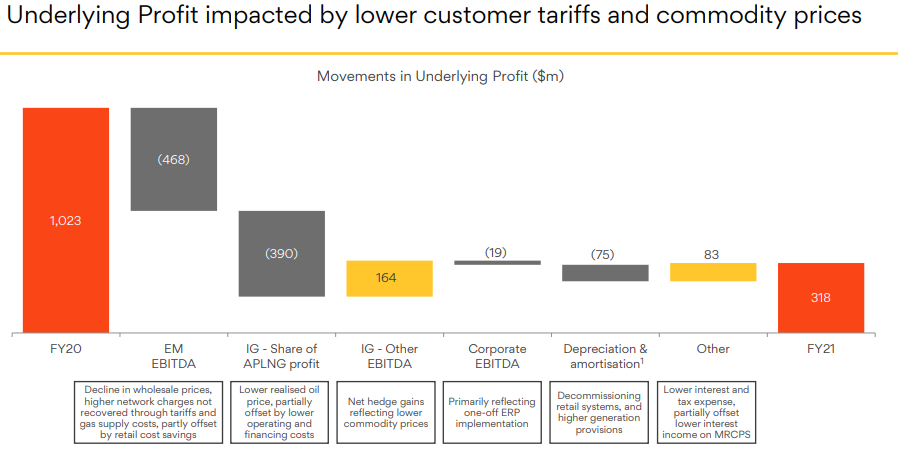

Origin Energy (ASX: ORG), in contrast to APA, had a worse year where their underlying profit was a loss of 318mio AUD, reflecting lower oil, gas and electricity prices, and their statutory profit was ~-2.29 billion, reflecting 2.2bln of impairments and deferred tax liability.

As such, investors are receiving a lower final dividend of 7.5c/share, where their FY total is 20c/share, below last year’s 25c/share.

Using yesterday’s share price ($4.50/share), ORG’s dividend yield is now 4.44%, down from ~5.1% last year.

Source: ORG FY2021 Investor Presentation

Looking forward, the outlook for ORG is negative in the year ahead, where analysts are predicting further earning downgrades due to lower energy (oil) prices forecast, with some light at the end of the tunnel in FY2023, bottoming in FY2022.

Decarbonisation and R&D

Something that Darren flagged in his pre-reporting season note was the likelihood of M&A activity, and R&D expenditure in the coming months/year ahead.

The reason for this is the lower for longer interest rate policy mentioned in my opening pre-amble, married to the growing popularity of decarbonisation, ESG and “net zero” emissions.

For these reasons, we’re seeing more and more granularity in the data expressing how corporates are going about achieving these targets.

In the case of APA, they set their target of net zero by 2050, giving them a very long horizon to achieve this.

In quite a frank admission, CEO Rob Wheals admitted “we don’t have all the answers for how we will meet this ambition today,” but that APA is working towards the target.

In February 2021, APA announced an investment to further this cause as part of their pathfinder Program, a hydrogen energy pilot project to convert 43km of the Parmelia Gas Pipeline in WA to Australia’s first 100% hydrogen ready transmission pipeline.

In regard to Origin Energy, decarbonisation is by no means a recent commitment, having signed up to the “We Mean Business” coalition in 2015, the first energy company globally to do so.

Like APA, they have pledged to be net zero by 2050, and doing so by rotating into lower carbon products, driven by their own (and customer) climate change ambitions.

At present, they’re the number one commercial installer of 10-100kW solar installations in Australia, and is number 2 in residential solar installations, now boasting >117,000 “green energy” customers.

Moreover, Origin are converting their regional operations to GreenPower, where solar has been installed at 9 of their LPG terminals with another 5 to come.

Otherwise, ORG has identified timber, paper and pulp as the commodities that pose significant deforestation risk within their supply chain and are reducing their use of paper-based products.

Closing Remarks

It’s quite an interesting job reviewing corporate earnings and trading updates, as they provide real world examples into investment trends and ways in which the world is changing.

On the surface, the market was bifurcated as the corporates with profit-links to energy prices (i.e., Origin) had worse years as commodity prices fell (as did bond yields), that made their earnings less attractive as the same time that their dividend yields (if sustained) became relatively more attractive than the lower yielding bonds available.

On the flip side, energy transmission utilities such as APA Group had a better year, due to regulated income and the optimal environment of some people being back at work with a large majority working from home.

Thinking about this one logically, a corporate office’s energy bill isn’t largely different between 10 people on the floor compared to 80 people, so the current environment of some people in offices and large numbers at home is optimal for these utility companies!

Otherwise, these utilities have also benefited from the lower bond yields and are using the pickup in earnings to transition to greener power networks, to utilise the greener energy sources being linked to our electricity grids.

This is likely to be a long trend ahead of us – indeed towards 2050 – as R&D continues to feature in this transformative process, as corporate activism continues as do the dividends.

*I would like to thank Gareth dM for this particular turn of phrase

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.