Reporting season is a period of a few weeks when many of Australia’s publicly listed companies disclose the details of their finances, and it happens twice a year.

Typically, reporting seasons happen in February – following the end of Q4 – and August – following the end of Q2.

While these two periods don’t capture all publicly traded firms as some follow different end dates, the period does capture most listed stocks, all within a few weeks of each other.

Hence, “reporting season”.

As Darren outlined on 26-July, we’ve expected strong results from our banks, having outperformed the market these last 12 months.

Also, we expected materials, stay-at-home technology and select consumer discretionary to have done well as well, with utilities, energy, tourism, travel and some REITS to have underwhelmed because of varying lockdowns and subdued consumer spending.

Furthermore, we expected to see corporate M&A activity increase, due to companies running decade-low leverage ratios, giving them ample capacity for takeovers, mergers, purchases etc, to try and put their best foot forward and grow out of this recession.

In terms of the banks, their impressive results were a foregone conclusion, which we publicised in my morning note on 28-July.

In their nature, banks are nearly always pro-cyclical investments, where the bulk of their earnings momentum is derived from:

- New loan origination

- The net interest margins (NIM) on existing and new loans

- Transaction fees from products as well as capital markets activities

While new loan origination has been rather subdued for obvious reasons (think lockdowns and uncertainty), NIM has grown because of steeper yield curves and transaction activities have increased due to financial market volatility and higher M&A activity from corporates.

Source: Mason Stevens, Bloomberg

As mentioned in my previous note, the lower loan loss provisions likely to be announced were going to pave the way for share buybacks, which were going to be short to medium term positive for bank share prices, with our banks holding surplus capital on their balance sheets well above regulatory requirements.

For the purpose of this note, we’ll focus on both CBA and NAB’s results, with our apologies to both Suncorp and AMP that are less widely held across our platform clients (and across Australia in general).

Commonwealth Bank of Australia

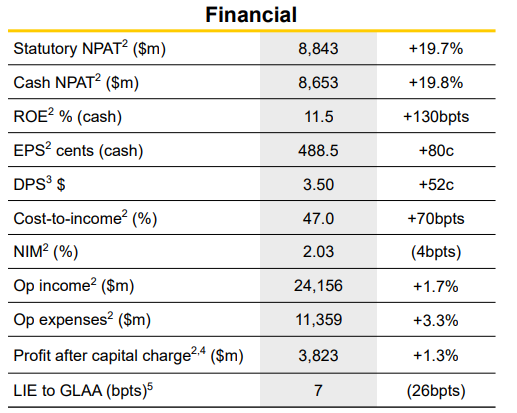

CBA (ASX: CBA) reported FY2021 earning on 11-August, and announced cash earnings of 8.6 billion AUD, which was a few percent above consensus analyst expectations.

For those interested in their results presentation and the litany of charts they provide, the presentation is available here.

The main contributing factor to the earnings beat was that loan impairment expenses was only 554m AUD, which is a reduction of 80% y/y due to an unwind in loan loss provisions across all business lines, while their revenue figures (top line) were in line with consensus estimates.

NPAT was up 19.8%, and they announced a final dividend of $2/share, or a full-year dividend of $3.5/share.

Source: CBA Results Presentation

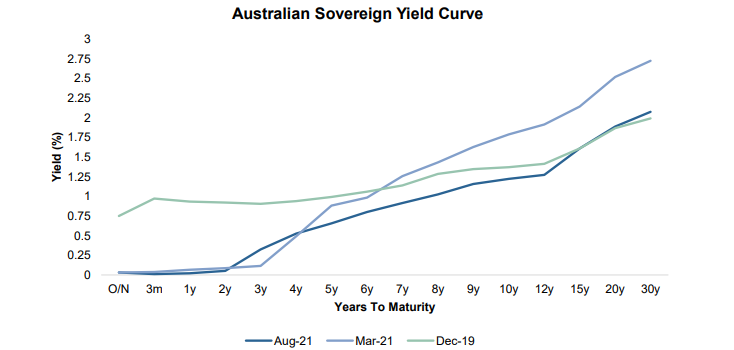

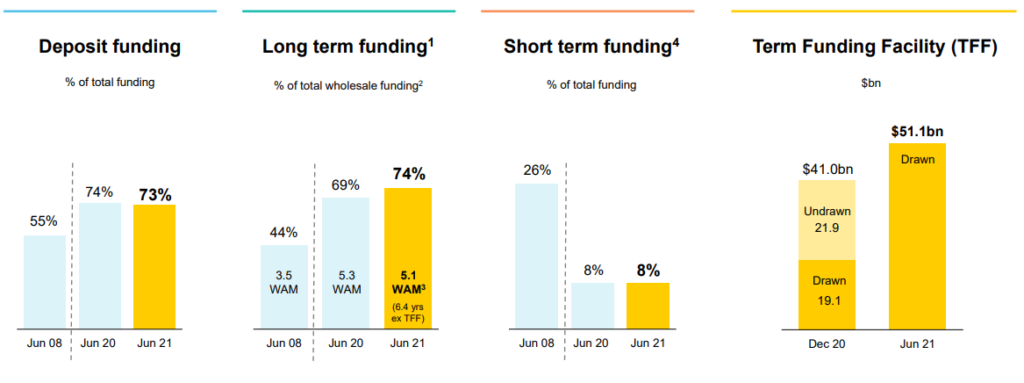

As we forecast, NIM was strong due to the steeper yield curve and low-cost funding available through the RBA’s Term Funding Facility (TFF), where CBA’s NIM only decreased to 2.03% from 2.07% at this time last year.

This strong NIM result is unlikely to last, given the recent flattening of the yield curve – compare March 2021 to August 2021 in our above chart – and also as we see CBA customers start to migrate their deposits held in low yielding accounts (at of near 0% interest rate) to higher yielding alternatives.

Anecdotally, we’re seeing this ourselves as Mason Stevens where there’s been a recent deluge of interest in fixed income solutions, seeking the higher yields available in credit bonds.

Source: CBA Results Presentation

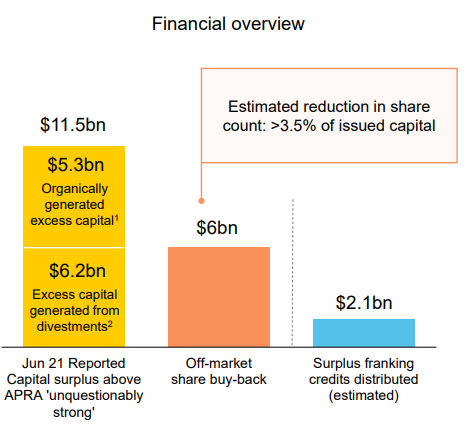

On the back of the strong earnings with lower provisions, CBA announced a 6bln AUD of stock buyback, given their CET1 ratio was at 13.1% and they aren’t forecasting any serious deterioration of their asset quality.

Post buy-back, their pro-forma CET1 will be at 12.1%, where we can pencil in future share buybacks and dividends for the coming 6-12 months.

Moreover, the large buyback is important as it signals that CBA management and APRA remain comfortable with overall credit quality and capital buffers, despite the renewed lockdowns and uncertainty across capital and regional cities.

This also means that the bank will likely be in no hurry to issue new hybrids, and likely be content to rollover their existing hybrid (Additional Tier 1 Capital) book, favouring more subordinated (Tier 2 Capital) bond issuance, as a cheaper option compared to more costly hybrids.

Immediately after the earnings announcement, CBA launched an AUD subordinated bond at 3m BBSW +1.4% p.a., where if they had issued a hybrid, they’d likely pay 3m BBSW + ~2.8%.

In terms of the short-term impulse for CBA’s stock, the large buyback was demonstrably positive for the stock price, where the buyback will be conducted off-market over the coming weeks and finalised in early October.

Source: CBA Results Presentation

National Australia Bank

NAB (ASX: NAB) wasn’t reporting their full year results like CBA was, as NAB – like ANZ and WBC too – uses a 30-September EOFY.

As such, we received a Q3 trading update from the bank, where the report can be accessed here, and we anticipate their FY 2021 results on 9 November 2021.

NAB reported Q3 cash earnings of 1.7bln AUD which is 10.3% higher than their H1 2021 update.

Source: NAB’s Q3 Trading Update ASX Announcement

Like CBA’s earnings performance, NAB’s result was driven by a $112m writeback of provisions, reflecting higher asset quality.

Differentiating themselves from CBA, NAB also recorded a fall in costs during Q3 and guided to a relatively flat cost growth for FY 2021 of 0 to 2%.

Their differed loan stock was less than 1 billion AUD – also similar to CBA – which is a manageable amount and unlikely to detract too much from next quarter’s earnings.

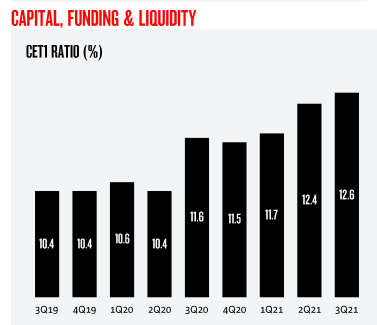

On capital, their CET1 was reported at 12.6%, a solid result, where their overall book continues to be less risk intensive as uncertainty improves, which is driving their capital ratios higher relatively.

NAB also announced they’ve acquired Citibank Australia’s consumer business, which reduced their CET1 by ~0.85%.

Source: NAB’s Q3 Trading Update ASX Announcement

On top of the acquisition news, NAB announced a 2.5bln AUD off market share buyback which will be conducted over a longer period than CBA, where the commencement date is 13-August, and the end date is 29-July 2022.

This is less positive in the short-term compared to the CBA announcement, though does establish a slow but sure perma-bid for the stock throughout the next year.

Funding wise, the update we received showed that NAB fully drew down upon their RBA TFF allowance of 31.9 bln AUD, which would likely have been a healthy boost to their NIM.

Closing Remarks

It was strongly suggested within both bank’s updates that their NIM will likely come under pressure over the coming months/quarter, as the yield curve has flattened and rolling lockdowns across states subdue confidence which leads to less new loan origination.

As such, we’d expected the banks to all have a worse trading period during 1-July to 30-Sep, unless M&A materially increases to offset the falling residential mortgage revenue (which is unlikely).

However, the stock buybacks will remain structurally positive over the short term, to support prices while the NSW lockdown continues.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.