The earnings season is nearing completion, and there has been a clear outperformance of growth over value.

Some of the greatest upside surprises have come from the Information Technology industry, which should come at no shock given the impact of COVID-19 on the increasing digitisation of the global economy.

The focus of today’s note will be on two of the most prominent ASX shares within this industry – Afterpay (ASX: APT) and WiseTech (ASX: WTC).

Both companies delivered earnings results with strong growth forecasts – which go along with the significant customer acquisition they have been able to develop since the onset of the COVID-19 pandemic which accelerated the technology adoption curve.

This story of COVID-19 accelerating adoption rates is emblematic of the industry as a whole – which has been able to enjoy a strong period since the pandemic forced businesses and consumers online.

Whilst certain consumer habits will remain post-COVID-19, a continuation of current growth trajectories may not.

The lofty multiples at which they trade have priced in these ambitious growth outlooks to an extent, however, it is likely that we see some retracement in technology adoption rates as the economy reopens.

Moreover, for those companies within more nascent sub-sectors of the industry, competition is only set to increase and may eat into forecasted growth figures.

This is the 4th instalment of our reporting season series, which has to date covered:

Afterpay – Declining EBITDA but New Revenue Streams

After a busy few months, capped off with Square’s (NYSE: SQ) acquisition, Afterpay released mixed results in their FY21 earnings.

Whilst the story of Afterpay is difficult to summarise in a few paragraphs, it’s a company we have written about extensively in the past:

Afterpay reported an EBITDA (excluding share-based payments) of $39m, down 13% YoY and 55% below market estimates. This miss was driven by lower than expected net transaction margins, and higher operational expenditures – including an increased marketing spend.

Source: Bloomberg

However, one of the brighter spots of their performance was the expansion of revenue streams, with Afterpay planning to begin offering in-app advertising, which should increase net transaction margins.

This expansion of revenue streams is critical to Afterpay, given merchant revenue should continue to come under pressure over time as more competitors move into the market.

Moreover, marketing spend increased in 2H21, growing as a proportion of Gross Merchandise Value (GMV) from 0.7% in 1H21 to 0.9%, which can be attributed to the new brand campaign, where Afterpay have attempted to drive more direct app/website usage.

Whilst this negatively impacts the bottom line in the near term, this could be positive for future customer monetisation should it increase the customer base, through enabling greater revenue from the aforementioned introduction of in-app advertising.

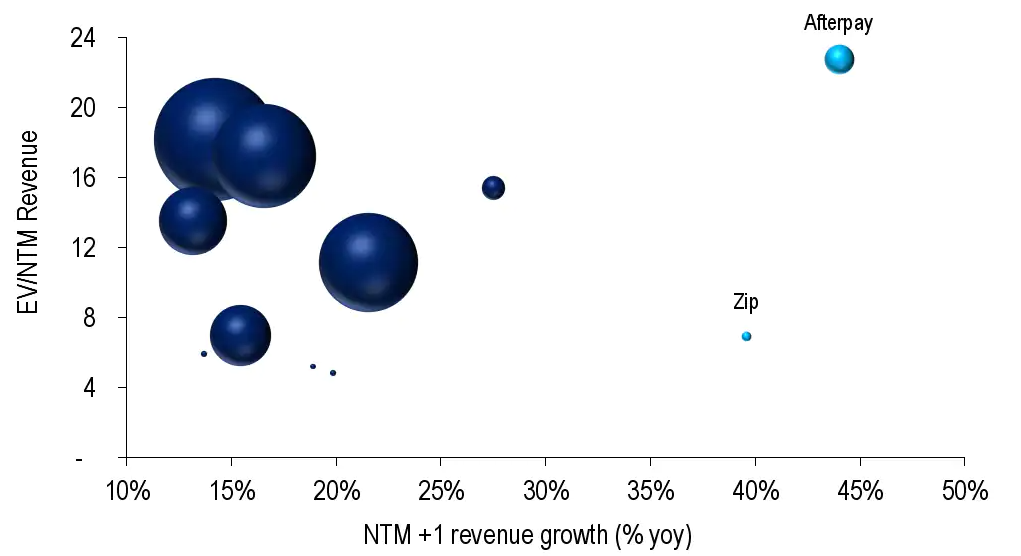

In terms of valuations, Afterpay is still valued at a premium to its payments/fintech peers on multiple metrics, however this is in line with its elevated growth prospects, driven by its brand strength and the opportunities presented by Square’s acquisition.

EV/NTM Revenue Margins

Source: Citi

Going forward, valuations will be driven primarily by that of Square, with upside potential from a greater than expected shift towards e-commerce and an acceleration in merchant acquisition.

Whilst Afterpay is more immune to any retracements in the technology adoption curve given strong market growth pre-pandemic, it is facing increased competition both domestically and internationally, and thus building a strong and recognisable brand will be key to ensure it maintains it current growth trajectory as more well-known multinationals like PayPal and Apple enter the market.

WiseTech – Strong Revenue Beat and Solid Tailwinds

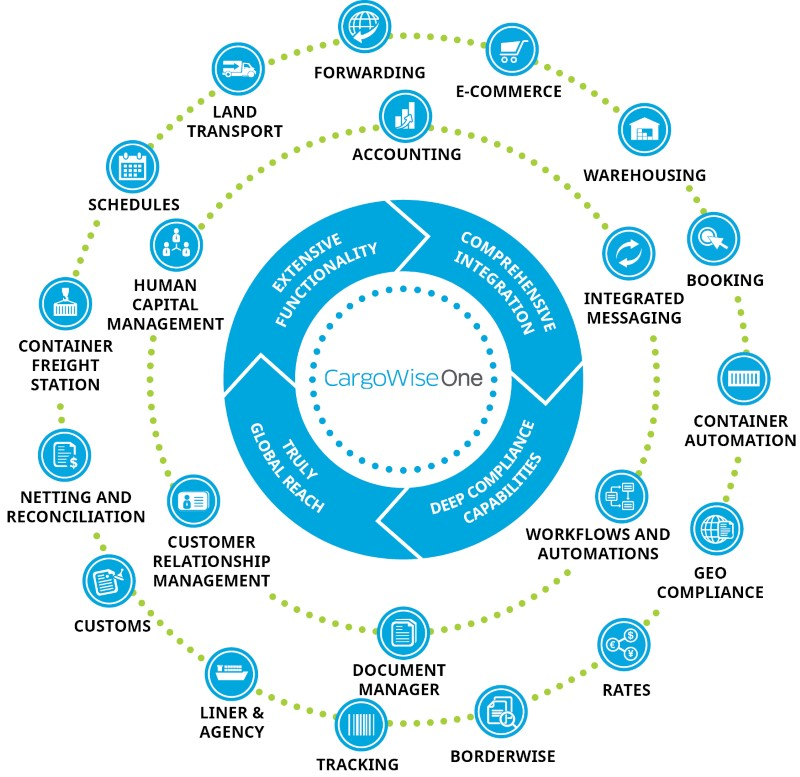

WiseTech is a leading software provider for the logistics execution industry, with its core product, CargoWise, being a market-leading Software as a Service (SaaS) solution which supports and simplifies the complexities of international freight.

It acts as a all in one solution, integrating various operational management processes into one global database, providing more transparency worldwide, reducing costs, minimising risks and increasing productivity.

The centralisation of operational processes has gained value over the past year, as employees have been forced to work remotely, and unable to travel internationally.

Source: CargoWise

Source: Bloomberg

WiseTech recorded a FY21 EBITDA of $207m, up 63% YoY, driven by strong revenue growth and margin expansion. This strong performance was reflected in the share price, which rose 28.5% on the day, even reaching 58% at one point.

The majority of this revenue growth came from CargoWise, whose revenues increased 33% YoY in 2H21.

This increase was driven by 6 new global customer acquisitions over the FY and increasing revenue from existing clients through both new and existing product lines.

Share prices were also bolstered by the acquisition of FedEx as a new client since FY end, with the majority of growth for the firm to continue to come from the CargoWise product.

Going forward, WiseTech should continue to benefit from digitisation and automation in the logistics industry, and from the planned expansion of its product lines.

However, downside risks for the stock could come from slower than expected new customer acquisition, which may not continue to occur at current rates as economies re-open and employees are able to work physically, and travel internationally.

Out of Steam, Or More to Come?

Whilst positive news has come out of the Info Tech industry during this earnings season, much of the valuations of those companies with loftier multiples are predicated on strong expected growth.

Whilst Info Tech companies have been able to enjoy a strong period since the onset of COVID-19, it is improbable that the rate of technology adoption will continue at current rates. Therefore, looking at previous rates of adoption and customer acquisition has the potential to mislead investors, who must look at 2022 growth trajectories with a blank slate, and with economic re-opening in mind.

Growth prospects will also be subject to a multitude of external influences, including increased competition, slower than expected economic growth, and regulatory risk.

For many of these companies, success will be largely determined by the competitive landscape, with those companies with more defensible business models, and stronger brand equity being more immune to increased competition.

Low interest rates will continue to support those companies which are more business facing, given the considerable Opex usually required to facilitate onboarding of new software and payments infrastructure.

Economic recovery timelines will have enhanced influence on Info Tech companies, with the re-introduction or continuation of restrictions likely to hamper medium term growth prospects.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.