Ranking stocks on the basis of “quality” may seem like an avant-garde technique, but it’s far from it, where the technique is well-established and has been used by fund managers for decades.

In fact, readers of “The Intelligent Investor” (1949) by Benjamin Graham would’ve been made aware of the concept (emphasis ours):

“The risk of paying too high a price for good quality stocks – while a real one – is not the chief hazard…the chief losses to investors come from the purchase of low quality stocks at times of favourable business conditions…”

This was a truly prescient statement at the time, which we should unpack.

Benjamin Graham, known as the “father of value investing” and also author of Security Analysis (1934), has quite clearly told us three relevant criteria for stock selection:

- buy securities at relatively low prices compared to their worth (valuation matters),

- main losses come from the purchase of low-quality assets (quality matters) and

- we need to be aware about our position within the economic cycle and the implications for corporate earnings and economic growth (growth matters).

As a background, we’ve also written several notes in recent weeks regarding other factors and attributes that are the main drivers of markets:

As my colleagues have done before me, I’ve written my note from the point of view that quality companies – referring to the factors that we can quantify that define quality – are going to be the key to investment performance and success going forward.

Defining Quality

Quality and value are often confused, because the filters and criteria that define them are similar in nature.

Value stocks focus on financial ratios such as price-to-book (P/B), price-to-sales (P/S), price-to-earnings (P/E) and other widely adopted measures, aiming to evaluate how cheap a given stock is with respect to its intrinsic value.

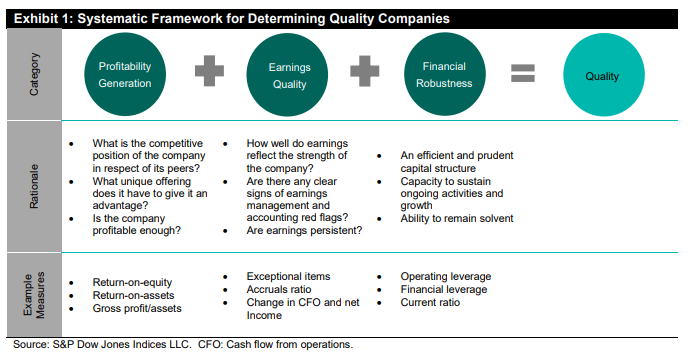

Quality, on the other hand, focuses on three main nebulous concepts – profitability generation, earnings quality and financial strength (S&P Global: Ung, Luk, Kang [2014]).

Backtest for Quality

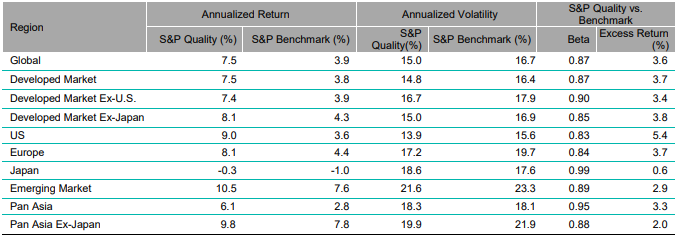

In the 15-year period between Jan 1999 and Dec 2013 that the S&P study reviewed, quality benchmarks consistently outperformed broader equity indices, across multiple geographies, with less volatility.

This means that not only did an investor receive more return for this factor allocation, they achieved this with less risk.

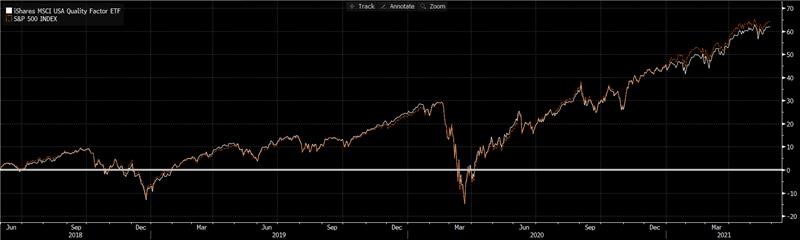

Re-running this backtest more recently over the period between 2018-present, the results are similar though less pronounced. As you can see below, the white and orange lines overlap for the majority of the three years, where US quality has returned 62.13% gross, compared to S&P 500 64.27% – but again, with less volatility.

Quality and ESG

The premise is simple in that quality companies tend to exhibit less volatility than lower quality companies, because of their better balance sheet strength, profitability and regular earnings.

As they’re higher quality, they tend to also score better in various ESG assessments too, where higher quality companies generally have better quality governance frameworks, environmental policies and social impact.

This is why quality as an investment factor should be on your radar for the coming years (decades?) because of the increasing popularity of ESG investing.

If ESG investing becomes more popular in Australia, similar to what has already happened in Europe and the USA, then more fund managers will allocate to those companies exhibiting high quality factors.

The increased number of marginal buyers of these securities will create positive momentum, where there may be more buyers than sellers.

As a subset of this idea, companies that are improving not only their quality, but also their ESG specific quality characteristics, will likely receive greater allocation due to their rise in ESG rankings and the positive impacts associated with this.

Investing in Quality

For those seeking a benchmark, the MSCI World Quality Index was incepted in 2012 and has historical performance since 1975.

This is a good place to start, though we note there are several other options available from S&P, Russell, FTSE and other index providers.

In terms of finding investment exposure, there are several options across various investment structures.

In advance, we note that when accessing quality managers and exposures, it’s worthwhile considering the portfolio’s market-cap weighting and sensitivity to changes in monetary policy, where quality names tend to be companies with larger market capitalisations, which have similar beta to equity benchmarks and perhaps to your existing equity exposure.

ETFs

Two of the most recognisable Australian ETFs representing quality are VanEck Vectors MSCI World ex-Aus Quality ETF (ASX: QUAL) and BetaShares Global Quality Leaders ETF (ASX: QLTY), where both provide liquid access to quality factors, though the underlying factors that VanEck and BetaShares use differ.

State Street Global Advisors also have a similar styled AUD ETF, the SPDR MSCI World Quality Mix (ASX: QMIX), which is slightly more multi-factor than the above two ETFs.

Internationally, one could look at JP Morgan’s US Quality Factor ETF (NYSX: JQUA), though there are many options available when looking at foreign equity markets.

Managed Funds

I’ve found it difficult to find specific quality-factor managers, as active managers have the ability to reposition their portfolios to take advantage of changing factors.

For example, Fund Manager ABC may represent quality as at 31-Dec-2020, but then have rotated into growth or value in February 2021, no longer representing the quality factor investment.

However, one fund manager I’ve found that consistently exhibits a quality framework is Aoris Investment Management and their Aoris International Fund (APIR PIM3513AU or PIM0058AU), but also can be categorised as “value” as well.

Direct Securities

For Mason Stevens platform clients inclined to direct equity investment over using externally managed products, I’d suggest reaching out to our Equity Dealing team to discuss the relevant factors, criteria and screens that can be utilised to refine the investment universe based on quality factors.

Closing Remarks

It’s hard to rebuff the original sales pitch of buying quality companies at reasonable prices, as that’s a time-tested investing strategy.

It’s also hard to argue against the notion that the sheer volume of money being allocated to ESG-stylised mandates and portfolios will not see quality perform reasonably, with more marginal buyers entering the market.

It’s also hard to contest that companies with relatively better balance sheet strength should also exhibit less earnings volatility, especially if you project central banks to increase cash rates in coming years, where companies with relatively more debt may be encumbered and see higher debt serviceability.

For these reasons we’re continuing to invest in similar styles to what Benjamin Graham proposed over 70 years ago, buying quality companies at attractive prices.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.