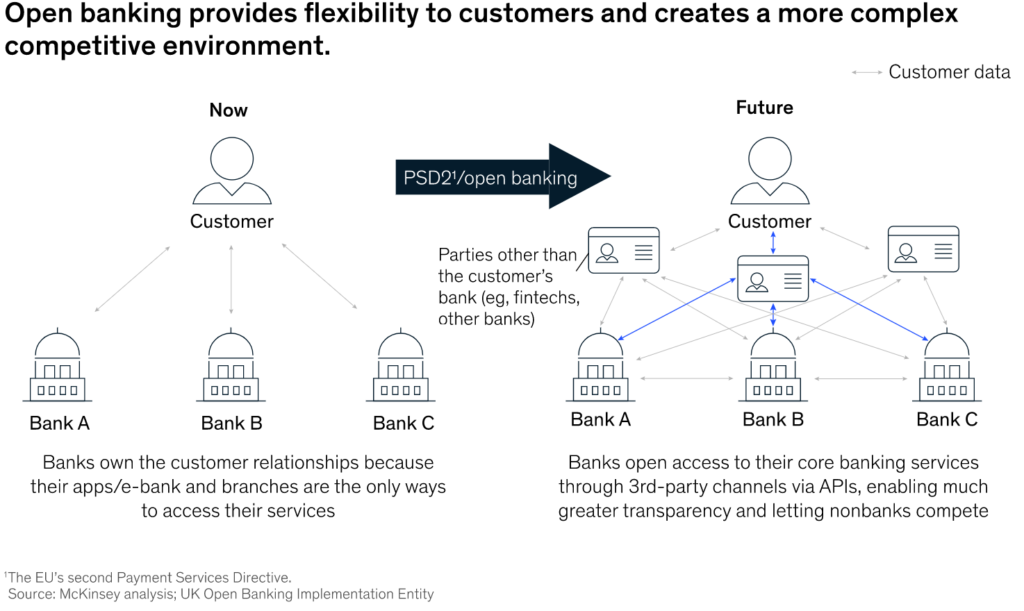

Fintech seeks to disrupt traditional financial systems through the creation and implementation of innovative technology solutions, intended to increase efficiency, generate synergies, and improve the customer experience.

Now that I’ve got most of the buzzwords out of the way – lets progress with the note.

Traditional financial systems are old, cumbersome, and outdated; however, we can’t simply rip existing infrastructure out and start anew with innovative technology.

The trust we place in banks to custody our savings -and the associated regulatory frameworks which keep them in check – takes decades to build, and whilst blockchain technology does offer greater levels of security and efficiency, its relative infancy means we will continue to operate on top of the existing core financial infrastructure for the foreseeable future.

What Fintech offers is the provision of financial services made mostly in conjunction with industry incumbents, offering solutions for payments, lending, insurance, banking, and wealth management which integrate with (rather than wholly replace) existing processes.

These services make up a large proportion of the financial services industry, and as such, there is still significant room for Fintech to grow.

In today’s note, we will cover Fintech – what it can become, regulatory risks, and Square’s recent acquisition of Afterpay.

What Can Fintech Become?

Fintech has the potential to entirely change the way we borrow, lend and spend money.

In fact, it already has to a large extent – digital wallets are quickly increasing their share of the global payments market (as we touched on last week in our piece on Apple Pay). The payments space is one of the largest subsets of Fintech – covering companies such as PayPal (NASDAQ: PYPL), Square (NYSE: SQ), and Visa (NYSE: V).

Popular payment services like Venmo (PayPal), and domestically, Beem (Westpac) will only continue to grow, given their unparalleled convenience in being able to transfer funds instantly between users. They highlight the layered financial system on which Fintech is currently built on, where funds originate from your bank account, and are transferred instantly between users within the payment applications.

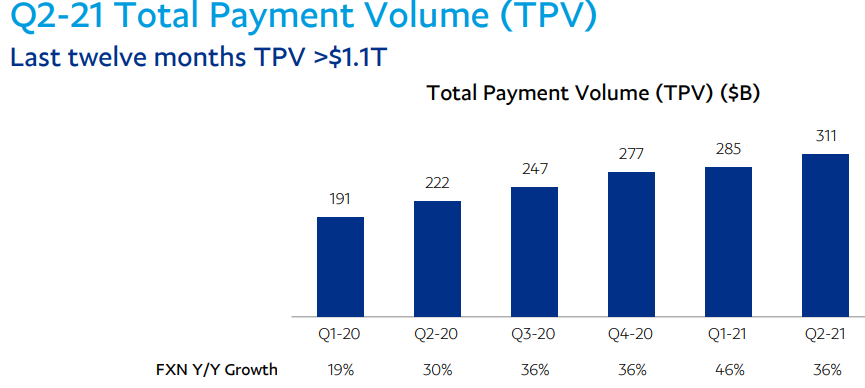

In PayPal’s most recent earnings release, Venmo volume increased 58% to USD$58bn, making up 18.6% of their Total Payment Volume (TPV). They don’t earn anything from each transaction, but instead take a 3% fee for credit card transactions, and a 1% withdrawal fee for funds held within Venmo wallets.

Source: PayPal

Moreover, BNPL solutions like Afterpay (ASX: APT), PayPal, and Z1P (ASX: Z1P) are eating into the market share of credit cards – with consumers enjoying greater convenience and reduced costs. Using artificial intelligence (AI), BNPL providers are able to approve users almost instantly, and largely without human intervention by leveraging consumer data.

This offers a more efficient and cost-effective solution to traditional credit card models – which involve a lengthy approval process. Fees are considerably lower, with no account-keeping fees charged, and the fee burden being placed on the vendor, as opposed to the customer.

However, as I will touch on later – regulation is one of the single biggest threats to this space, with existing regulatory frameworks unsuited to these new business models.

We’ve also covered the payments/BNPL space in other notes, which can be found below:

Fintech within the insurance space has seen a shift in mindset – where coverage used to be determined on the basis of what the insurance companies were able to sell, but now is more based on what the customer demands.

Through utilising AI, Fintech insurance companies are able to better understand the underlying risks attached to each individual customer, and subsequently, are able to offer more flexible, adjustable coverage.

For customers – it’s a win, win.

Premiums are able to be charged at a rate consistent with the client’s individual characteristics, where previously it was primarily a “one size fits all” approach.

Application processes can be simplified – where extensive medical and financial checks are not required to gain coverage.

Existing companies such as Trov provide usage-based insurance – where coverage can be toggled on and off at will to cover periodic situations, and Metromile, which offers pay per mile car insurance for city dwellers.

However, despite 73.7% of uninsured American adults listing affordability as a key driver to their insurance status, the Fintech arm of the industry still remains relatively nascent.

Fintech is also enhancing the user experience within the wealth management industry.

For many companies, this has taken the form of the development of mobile apps – something Mason Stevens has rolled out recently. For further details on this, please contact your Mason Stevens representative or visit our website.

Mobile apps enhance the user experience – offering analytics, trade processing, and other additional features on the go.

Other Fintech developments have taken things further – with “Roboadvisors” now offering automated asset allocation, with little to no human intervention throughout the lifetime of the account.

Whilst automated advisor services could never replace the expertise and sophistication of a financial advisor/asset allocator – Roboadvisors have the potential to offer more cost-effective solutions for those with more simplistic demands.

Square Pegs in A Round Hole

Current financial regulatory frameworks are largely unsuited for Fintech’s, and as with any new disruptive technology, regulators have had a tough time in figuring out what the best course of action is.

If regulations are too harsh, you risk stifling innovation, but if they are too lax, consumers are at greater risk being exposed to fraud or dangerous practices.

Regulation will continue to serve as one of the largest threats to most Fintech companies, and as such investors must keep abreast of any regulatory changes.

Square and Afterpay

Afterpay is a favourite within our morning note series, and for good reason – there is always something new and exciting which they bring to the table.

Max touched on Afterpay last week, but as always, they have surprised us once again with their acquisition by Square.

What the acquisition offers is the combination of two disruptive market leaders, both with a unique two-sided business model.

They have both been pioneers in their own space – Square with micro-merchant card acceptance, who previously rarely accepted card payments given the costly nature of mobile terminals, and Afterpay with the BNPL model.

Both businesses also provide pride themselves on providing value to both merchants and consumers, and with such similarity in their focus, synergies are inevitable.

Afterpay will be able fill voids within Square’s ecosystem, boosting Square’s ARPU (Average Revenue Per User) and enabling Square to move up-market on both the merchant and customer side.

Moreover, Afterpay will be able to benefit from exposure to Square’s 70m users and 3m merchants, providing a healthy advantage in the race to becoming a household name in America – much like they are in Australia.

Fin(Tech)

The matter of Fintech becoming a controlling force within the financial services industry is a matter of when, not if.

The benefits for customers and businesses are undoubted.

Whilst the current market is distributed across many different companies, what will likely transpire is the acquisition of leading Fintech companies by long-term industry incumbents, as well as the growing dominance of current market leaders such as PayPal and Square.

Over the next 5-10 years, our economy will become increasingly more digitised, and those companies which will stand to benefit will be those who provide value to both consumers and business owners.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.