As consumers continue to transition away from cash, the payments ecosystem is becoming increasingly more integral to our global economy, bringing in an estimated USD$1.9bn in revenues in 2020 (JP Morgan 2021).

The space is dominated by well-known players such as Alipay, PayPal (NASDAQ:PYPL) and Square (NYSE:SQ), who have all made their mark on the industry through their innovative product offerings.

However, Apple Pay (NASDAQ:AAPL) and Google Pay (NASDAQ:GOOGL) have continued to increase their market share through their unique contactless payment models, leveraging near field communication (NFC )technology to drive towards the obsolescence of signature and pin-based card payments.

Apple Pay in particular has shown the greatest promise to gain further market share, owing to their larger customer base, with its integration within the Apple family of products taking the majority of onboarding costs from the customer side.

For Apple, its payments business has diversified its revenue streams, coming at a time of significant importance, given the flatlining growth of its sales of iPhones and computers.

Moreover, its recent foray into the Buy Now Pay Later (BNPL) space has provided a threat to existing incumbents of Afterpay (ASX:APT), Z1P (ASX:Z1P) and PayPal.

In today’s note, we will cover Apple Pay – its current position within the market, its recent foray into BNPL and its growing importance to the Apple empire.

How Does Apple Pay Work?

Apple Pay currently accounts for 5% of global card transaction volume and is on track to account for 10% of transactions by 2025 (Bernstein, 2020).

What Apple Pay offers is contactless mobile payment, increasing convenience through leveraging NFC technology.

Instead of pulling out a card, users can instead pay by tapping their phone on card readers, or through the click of a button (instead of entering card details) in online stores.

It offers a more secure mode of payment, taking away the need for physical cards (which can be easily stolen), and replacing signature and pin-based authentication at the point of purchase, with phone-based verification.

This phone-based verification can include either face ID, touch ID, or by simply entering your pin code on your phone.

On top of more secure verification processes, your data once you have transacted is also more secure, with no card details or identities shared with merchants, with no card details stored on your device or within Apple servers.

For Apple, it’s a win-win.

They already have a large portion of the world within the Apple ecosystem and are able to pick up 0.15% on every transaction made through Apple Pay.

By 2025, it is forecasted that digital transactions will exceed USD$10 trillion, and if Apple Pay were able to account for 10% of this as forecasted, that would deliver them $1.5bn in annual revenue.

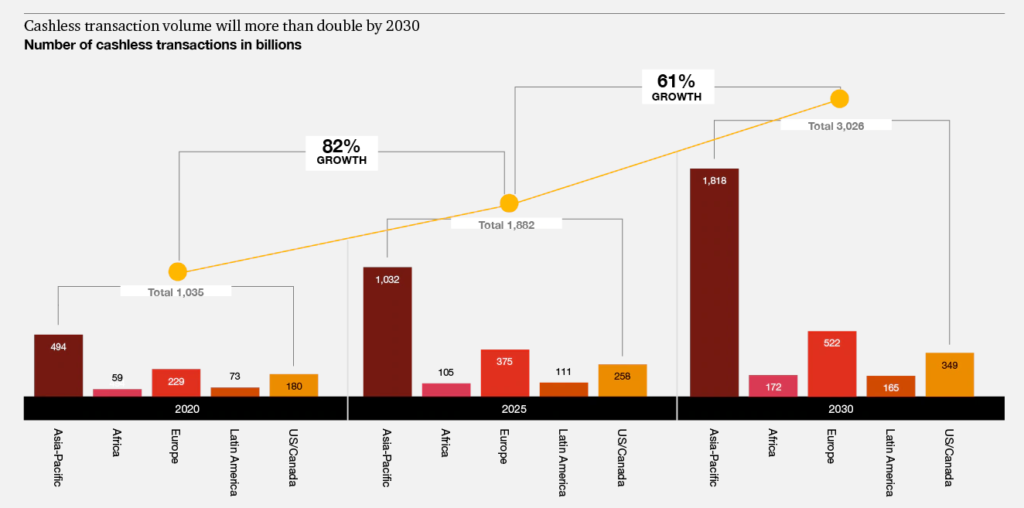

This trend is only set to continue picking up speed, with COVID-19 also increasing the movement towards contactless payment methods.

Source: PWC

However, as is commonly known, Apple has been in the crosshairs of anti-competition regulators.

The Apple Pay product is the only NFC based digital wallet enabled on iPhones, with other payment platforms like WePay and Alipay having to use QR technology, given Apple is unable to restrict its cameras from scanning QR codes.

Moreover, its legal spout with Epic Games (owner of popular game, Fortnite) could serve as a precedence for any future anti-competitive behaviour using the Apple Pay platform.

Fortnite was removed from the app store after Epic Games built in a direct payment within the game to circumvent the 30% fee charged by Apple on any purchases within the app store, citing that the fee is anti-competitive.

For many app developers, these fees are a part of life – necessary to access the swathe of customers on the app store.

Whilst anti-competition measures could hurt other aspects of Apple’s business, third-party subscriptions only make up a small portion of the 660m paid subscriptions which Apple has, and is unlikely to cause a material impact on the bottom line.

Buy Now Pay Apple Later

Apple have recently announced their planned expansion into the BNPL space through the “Apple Pay Later” solution which will be integrated within the Apple Pay product.

This expansion follows on from their 2019 creation of the Apple Credit Card, which was also integrated within the Apple Pay product.

The Apple BNPL product will follow the same arrangement as its credit card, where Goldman Sachs acts as the lender for the loans.

Along with PayPal’s expansion into the space, this serves as a significant threat to Afterpay and Z1P, particularly within the US where Apple Pay is accepted at 85% of retailers.

The implications for both Afterpay and Z1P will be followed closely by Australian investors and is worthy of a note on its own – something Max will cover later this week.

We are continuing to see a shift away from the traditional credit card model, and towards payments ecosystems which satisfy both the payment and credit needs of consumers – an area where Apple is building their expertise in.

Another Dimension to the Apple Empire

It’s no longer a secret that Apple is more than just a phone manufacturer.

Whilst payment services only make up a small portion of the tech giant’s current revenues, it will serve as an integral business unit for the company in years to come.

Given the cult-like nature of its user base and the high proportion of global consumers already within the ecosystem, the ability to further monetise its existing users will determine whether Apple transitions into a more value-orientated stock – or if it continues its trajectory as a growth stock as the business becomes more vertically and horizontally integrated.

Source: Bloomberg

Given so many consumers are already within the ecosystem, the single biggest detriment to its continued expansion in the payments space will be anti-competition regulation.

From a shareholder perspective, success would lead to even higher share prices.

However, from a humanitarian perspective, giving one company such power over so many aspects of our lives would likely lead to negative implications.

Time will tell what happens – maybe in 5 years’ time, we will be writing about Apple’s dominance in the ride-sharing industry, a real possibility given Apple’s intentions to release a self-driving car by 2024.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.