A big topic of conversation in 2021 is when central banks are going to normalise policy, removing some of the “easy” money policy support that is currently in place, providing ample liquidity for financial markets.

Before normalising policy, however, the RBA has established a new paradigm, a campaign where the central bank openly discloses their policy initiatives, where possible, well before enacting them.

This is a marked shift from the days of surprise central bank announcements, or secrecy in central bank policy.

Former US Federal Reserve Governor Janet Yellen – now US Treasury Secretary – was quoted in 2012 saying:

“In 1977 when I started my first job at the Federal Reserve Board…it was an article of faith in central banking that secrecy about monetary policy decisions was the best policy”.

Nope. Not anymore.

We saw this recently in April, where the RBA publicised an academic paper discussing their own methodology to gauge how “easy” monetary policy is.

The outcome of that paper that we summarised on April 7th was that the RBA would continue with a low Overnight Cash Rate (OCR) and maintain their level of bond purchases for the foreseeable future, because in their view, monetary policy had tightened due to a steeper yield curve.

What this paper also signalled was that the RBA was becoming increasingly transparent regarding their policies and how they were rationalising their decisions.

Future Policy Path

As another insight into the RBA’s transparency campaign, they recently published an academic paper that further articulates their transparent policy framework, so that financial markets are aware of the RBA’s policy approach, limiting the likelihood of adverse financial market “tantrums” to unexpected policies.

This type of communication is known as “forward guidance”, where central banks state what future policy will look like, so that with that knowledge, households, businesses and investors are able to make decisions based upon this guidance.

In doing so, these economic actors make the forward guidance self-fulfilling by establishing a transmission of monetary policy into the broader economy.

In psychology, this is known as “dilution effect”, which refers to the concept that each incremental piece of news regarding a subject – the marginal effect – diminishes the likelihood of a reaction.

This is a well-practiced technique of governments too, whom often “leak” their budget policy ahead of annual budgets, so that the marginal reaction is reduced.

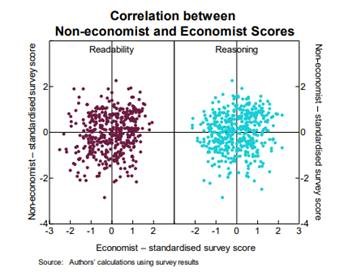

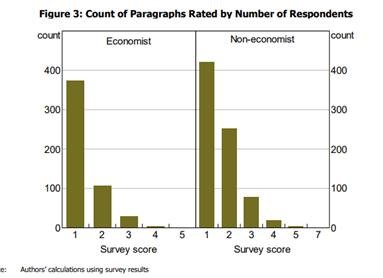

In this paper, the RBA was basically studying three things:

- Their audience,

- Readability of documents and

- Amount of reasoning within those documents.

And what the RBA found from this study was certainly not ground-breaking.

In fact, they are empirically proving what we already know.

Namely, that economists read central bank papers, Minutes and speeches differently to non-economists.

Where the RBA found there is no correlation between what economists and non-economics take away from RBA publications, based on the reasoning and readability.

The RBA also found that the more basic they made their publications (less reasoning and jargon, making them more readable), they decreased the efficacy of their communication.

Conversely, when they increase the reasoning quotient and made the publications less readable to non-economists, the communication was only accessible to a much smaller universe of people, where implications of their publication were lost due to knowledge and skill gaps.

Also, they found the more paragraphs there were to read, the less likely people were to continue reading.

As we mentioned, this readability and reasoning scoring has been well established over the last three decades through psychology studies, something we employ within our Mason Stevens morning note series, where each publication is scored based on its reading time:

The RBA’s Conclusions?

RBA communication needs to be “adapted for a different audience and no single measure can do justice to the multiplicity of objectives communication has”.

Which means more communication, and different documents for different levels of understanding, where the economist and the non-economist are satisfied and understand the RBA’s policy initiatives.

How This Affects Financial Markets

The RBA are attempting to make their policies transparent and make us all aware of the future path of monetary policy.

By enacting their yield curve control policy in March 2020, pegging our 3-year government bond at the same rate as the Overnight Cash Rate (OCR), they established a visual reminder that the OCR would remain at that level for the coming multi-year period.

Since then, they’re telegraphing every single policy initiative, where possible, ahead of time.

In fact, in previous RBA speeches, the RBA has sign-posted that their July Board meeting will address the future path of the yield curve control policy, and the likely extension of their existing quantitative easing program.

Summary Remarks

In closing, the RBA are making financial actors aware, whether these market participants are onshore or offshore, economist or non-economist, that the RBA are going to hold their ground and implement their policies in a controlled and transparent manner.

In fact, I’d go so far as to say their rubric is:

- #1 Release an academic paper discussing policy initiatives and the likely effects

- #2 Publish articles about possible RBA policy movements using friendly sources to the RBA, such as the AFR or The Australian, where non-RBA officials can begin the conversation first.

- #3 RBA insiders will speak at events and suggest what the RBA may do, if and when economic data approaches their target levels

- #4 Assess the reaction of the market based on #1-3, and if no significant tantrum, then look to move ahead on a date they propose in the future – likely a couple of months

- #5 Rinse and repeat

Which is why it’s likely the RBA does not hike for the next 2 (or more) years.

Which is why QE will likely continue, though at lesser amounts in the future as they effectively and slowly taper this policy tool.

Which is why they will wait for inflation as measured by trimmed mean CPI to average higher, before they fully exit the policy accommodation they have in place right now.

And that all-in-all, they are going to keep policy accommodation relative to other global central banks such as the US Federal Reserve, Bank of Japan, European Central Bank, Bank of England etc, lest they normalise policy too soon and see our AUD appreciate rapidly.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.