If there is anything that the central banks have learned – especially our RBA – since the 2007/2008 Global Financial Crisis (GFC), it is that monetary policy is more effective when it is transparent and understood by financial markets.

Gone are the days where a central bank may regularly hold a surprise “inter-month” meeting, where a cash rate might be hiked or cut in response to a specific variable they were monitoring closely – this did happen in March 2020 as a response to COVID-19’s increasing infection rates, though the trend of less of these inter-month meetings remains intact.

Now is the age of central bank transparency, where central bankers engage in regular speeches and publications with consistent, uniform messages, seeking to reassure financial markets that they’re still credible institutions worthy of determining the most important price in the entire world – the price of money.

Recent RBA publication

On 23 March 2021, the RBA published a discussion paper that details their Financial Conditions Index (FCI) and Growth-at-Risk (GaR) modelling.

You can find both the academic version in full and non-academic summary here.

This was one of the RBA’s first steps to producing a comprehensive narrative that financial conditions are currently “restrictive”, rather than “expansionary”, where they can quantify economic costs associated with instability.

This is another example why central banks are providing more and more forward guidance to monetary policy.

Spoiler alert: they’re paving the way for extended and further stimulus in the months and years to come.

Don’t agree? Hear me out...

The RBA has a wealth of researchers at its disposal to model risks to economic activity from changing financial conditions.

In this case, they have been utilised to produce a new model to assess these risks and the underlying sensitivity to financial (think: monetary) conditions.

This involves modelling the distribution of economic activity across different industry sectors, computing the probability density functions (PDFs), evaluating tail risks to economic activity, then weighing the upside and downside scenarios.

This sounds intense, but it’s basically a risk/reward analysis, where they’re attributing the different growth sequences due to certain levels of financial conditions, assigning probabilities to these outcomes.

Broad Summary

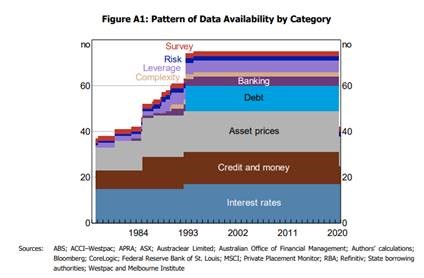

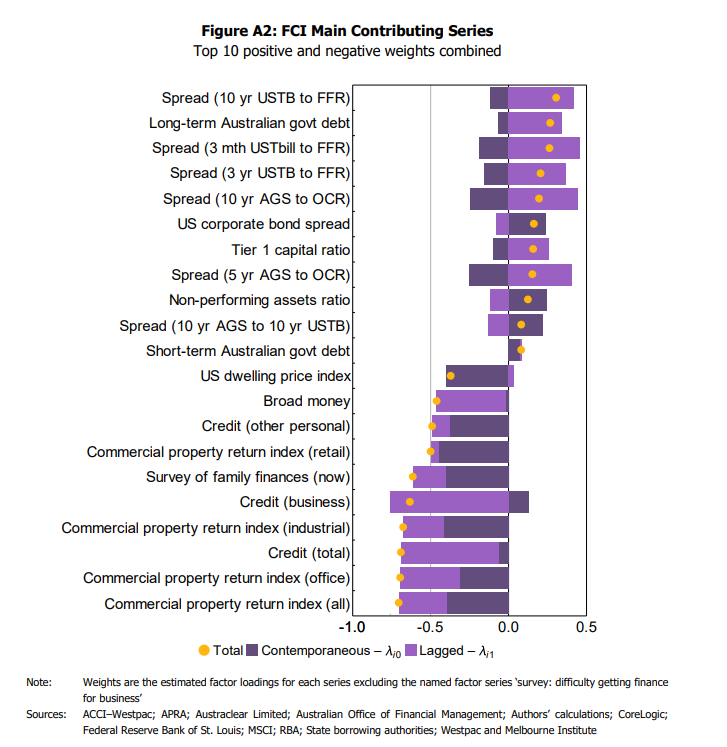

The Financial Conditions Index uses a dynamic (think: changes in real-time) factor-based model which incorporates 75 different data points at various weightings, to measure financial conditions.

Data points include those such as asset prices, interest rates, spreads, credit growth, money supply, debt issuance, leverage, business confidence, consumer sentiment, etc.

As you can see, there is an obvious high weighting to interest rates, credit supply and growth, money supply and growth, financial asset prices, debt (also similar to credit) with ~10-15 of the 75 variables measuring consumer and business sentiment, risk, leverage (also linked to credit and debt) and financial product complexity.

While we don’t know the exact weightings – they may be equally weighted or not – it’s likely these indicators are heavily influenced by bond yields (foreign and domestic), credit expansion and key financial markets.

Keep this in mind, as it’ll become more relevant when examining the RBA’s conclusions.

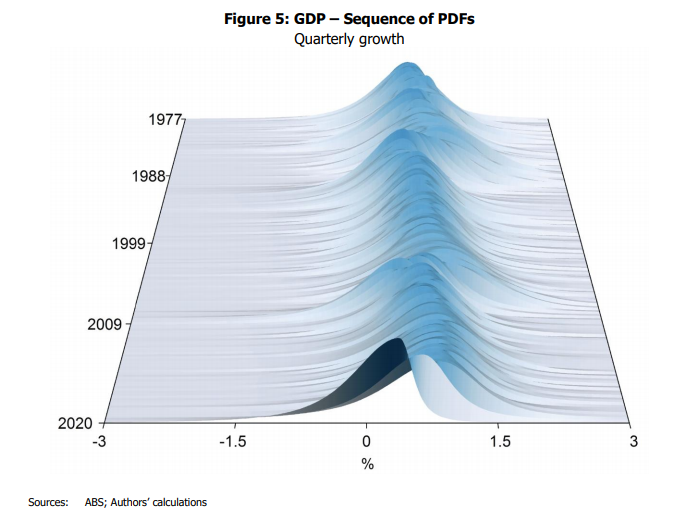

Growth-at-Risk

The growth-at-risk framework is used to assess Australia’s economic upside and downside scenarios, to provide the lens for enhanced monetary policy decisions.

It was found that there was generally more upside potential to economic growth (measured by GDP) in the 70s and 80s, with less upside in the 2010s to present day.

What the RBA found was that quite a number of these indicators were producing negative signals based on the available data; negative meaning that forward looking returns were skewed to the downside rather than the upside.

Current Financial Conditions

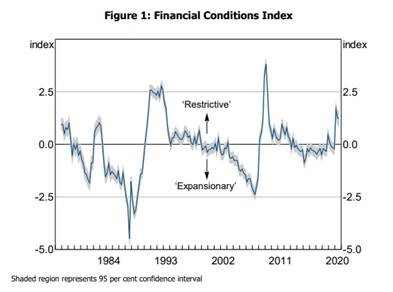

The below graph is the output as at end of Q3; we haven’t received the Q4 update yet as not all data was available as at 31-Dec-2020 when the report was written and published.

Financial conditions – based on the 75 variables – have moved above 0.0 to being “restrictive” rather than “expansionary”, which is denoted by a model value less than zero.

This may have been one of the main drivers behind the RBA’s decision in November 2020 to extend their bond purchase program (“quantitative easing”) for another 6 months, for 100 billion AUD.

This has further been extended in March 2021 for another 6 months, for another 100 billion AUD.

Likely this in aggregate is the RBA’s go-to policy response to ease financial conditions further, should their FCI model show an increase in restrictive conditions, where the RBA will respond with further policy measures such as bond purchases, or low-cost bank funding such as the Term Funding Facility (TFF), a policy initiated in March 2020 to provide support for SME lending.

Closing Remarks

There we have it: the RBA is explicitly sharing with us their methodology for assessing domestic financial conditions, showing us that they have become increasingly restrictive, which could potentially impair our economic recovery.

As we saw in their economic growth-at-risk modelling, outcomes are asymmetrically weighted towards the downside in recent years, where the RBA needs to remain proactive to ease monetary policy to achieve their mandated goals.

If I was a betting man – which I am – I would suggest that key RBA speakers such as Governor Lowe, Deputy-Governor Debelle, and Director Kent, will touch upon the key elements of this research in upcoming speeches, to reinforce the measure and cement in global financial markets’ minds that the RBA is “here to help” and are serious about providing accommodative financial conditions to achieve policy targets.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.