Historically, our Australian dollar (AUD) currency’s worth has largely been defined by three criteria:

- Commodity prices (terms of trade)

- Carry (interest rate differentials)

- China’s economic impulse

And lately we should also add to the list:

- COVID-19, which has driven China’s economic trajectory and their purchasing of key Australian export commodities, as well as our own domestic growth potential

We can call this the four C’s framework – Commodities, China, COVID, Carry.

As we haven’t provided an update on the AUD trajectory since 21-July, we thought that today would be an excellent time to take stock of the headwinds our AUD faces, despite potentially being fundamentally undervalued.

Commodity Prices

Australian currency is one of the world’s most cyclically sensitive currencies, alongside the Mexican peso (MXN), Norwegian krona (NOK), South African rand (ZAR) and Russian ruble (RUB).

And amongst these other cyclically sensitive currencies, Australia has the largest economy and a more liquid currency market where AUD has become the global go-to proxy for “risk-on” and global growth, making it an incredibly good bellwether for assessing global sentiment, as well as our domestic outlook.

In terms of commodities, our AUD (green line) has tracked commodity prices (red line) reasonably faithfully over the past decade, although with a slightly lower correlation since 2020 where the other C’s have played varying importance, as COVID asserted its factoral dominance.

Source: Bloomberg, green = AUD/USD, red = Bloomberg Commodity Index

Carry

The other factor in the breakdown of commodity vs AUD correlation has been the RBA’s Yield Curve Control (YCC) policy, pegging our 3-year government bond yield to the Overnight Cash Rate (OCR).

This effectively capped the yield of bonds maturing within this range and gave the forward guidance that the RBA would be extremely unlikely to raise the OCR within this period.

As Australian interest rates were not allowed to float due to market forces, whilst other government bonds were and are, this created a negative interest rate differential, where a number of other sovereign bond yields moved higher than Australian equivalent yields.

Because of this, there was reduced “carry” for income-seeking investors such as sovereign wealth funds, central banks, global pension funds, life insurance companies etc, who would invest elsewhere at those higher yields, to varying degrees.

However, this was not limited just to the shorter end of our yield curve, as Australia underperformed in our vaccination rollout where we were the slowest OECD nation until recently (we’re now 35/38), this also limited the upside to our government bond yields, where our Australian 10y government bond yield (green line) has traded under US 10y govies (red line), represented by the lower panel which tracks the yield differential.

Please note, investors usually require a yield premium to purchase AU bonds relative to US, so even if AU 10s were ever so slightly higher yielding than US 10s, the premium wouldn’t be large enough to become a “carry trade”, like we saw in the 2001-2007 period where the premium was >1%.

Source: Bloomberg

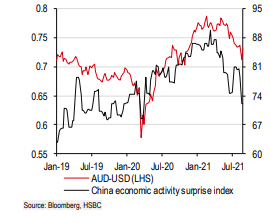

China

The China factor is heavily intertwined with the commodity factor, as China is Australia’s number one export destination.

The current deceleration in mainland China’s economy adds a headwind to the AUD from a commodity price perspective, and also elicits negative sentiment from peaking projections of the global growth rebound.

Whilst China is slowing, it’s also slowing faster than market expectations, where HSBC’s economic surprise index for China has dropped quickly.

Hence, we can see a reasonable relationship between AUD/USD and the Chinese CSI 300 equity index.

Source: HSBC, Bloomberg

It’s also worth remembering that the linkage between the AUD and China go beyond just cyclicality of commodity prices, the risk-sensitive nature of the AUD also plays a part where AUD faces occasional pressure when trade tensions rise between the two nations, and the projected slowdown in Australian national exports.

COVID-19

Some of the recent weakness in China reflects the impact of COVID, where they aren’t alone, that’s also affecting our domestic economy to a larger degree as well, as Australian COVID infections have risen to a record high, and resultant lockdowns have impaired economic activity and both consumer and business confidence.

The AUD has obviously suffered alongside these developments, where it’s important to assess whether these are transitory or longer lasting impacts.

On the transitory side of things, some states and territories may reach their 70% double-dose vaccination targets before year end, where economic growth may rebound in what’s being now dubbed “revenge shopping”.

This sounded hilarious the first time I heard the term but begins to make sense as we see the large volume of people already organising parties, birthdays, weddings etc as soon as they’re available to do so, where we can imagine a fair amount of alcohol may be involved in many of these occasions.

On the slower side of things, some parts of Australia may only begin to reopen in Q1 2022 or may attempt to maintain “zero-COVID” models, whilst international travel may also come back more slowly than many would like.

Likewise, large crowds may not be allowed for a period of time, as a safeguard for the public as a politically viable solution to limit a potential 3rd wave domestic spike in cases, likely around the time most of us require our booster vaccinations mid next year.

Near-term Pain for Longer-term Gain

Using the above four factor approach as well as short-term positive view of the USD, it’s hard to be positive about the AUD for the coming 3 months until year end, where we could foresee an AUD/USD exchange rate at year end of 72-73 cents, a 10% depreciation peak-to-trough since January 2020 where we briefly touched 80c during peak “reflation” and optimism.

Hence, we’d expect some short-term pain for the AUD, and some form of bounce-back in 2022 as we experience some form of V-shaped recovery, though to a lower extent than in 2020 and 2021.

In fact, we could argue that AUD/USD (green line) looks cheap relative to its terms of trade (net exports, red line), where this historical alignment has been muted by the RBA’s YCC as well as bearish risk sentiment in regard to China and global growth.

Source: Bloomberg

However, we wouldn’t go so far as to assert that AUD/USD will completely align with the terms of trade and commodity factor too soon, as that would imply an AUD/USD of ~85c or higher, but instead, we’ll remain at the behest of the four C’s, requiring an improvement from China, the domestic impact of COVID, confidence improvement and commodity exports remaining strong.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.