On 13-Sep when we last detailed our outlook for our Australian dollar (AUD) we re-identified the fundamentals of our domestic currency’s worth:

- (C)ommodity prices (terms of trade)

- (C)arry (interest rate differentials)

- (C)hina (their growth and how it influences our growth)

- (C)OVID-19 (which has driven so many economic relationships of the past two years)

In today’s update, we want to nuance some of these factorial views and the economic influences, as well as provide an update for our AUD trajectory given the market has moved.

Horizon Preference

If you’ve ever wondered how and why some factors affect economic outcomes and security prices at times, but not at others, you need to be aware of a concept called “horizon preference”.

The idea is that depending on your sentiment, your views of the future will shift between the short and the longer term.

When things are good, we think longer term, into the future.

When things are bad, like last year, we dwell on the present and think about our immediate safety, our supply of food and water, our ability to pay bills, etc.

As countries have emerged from the pandemic and are beginning to transition into pre-COVID levels of economic and social activity, horizon preferences have shifted once again from shorter to longer term.

This change in sentiment regarding the economic recovery is the reason why we’re starting to see a shift in investor preferences and sentiment, and renewed optimism and longer-term strategic thinking.

AUD/USD

This is important for the valuation of our AUD, as our currency is a global bellwether for economic activity and global trade.

As we’re a relatively open economy with accessible capital markets and a liquid currency, we’re amongst the few preferred proxies for global investors, looking to take advantage of economic reopening and the positive shift in sentiment.

As it stands, the AUD/USD exchange rate is sitting just above 74c (15-Oct-2021) having reached a recent low of 72c.

As we forecast in our previous currency update, we expected a near-term low of high 71c to low 72c as our key support level, which would likely align with peak negativity regarding domestic COVID infections.

Chart 1 – AUD/USD Spot Exchange Rate

Source: Bloomberg

This investment thesis was validated in September as more than half our national economy was in effective lockdown restrictions, in a period just before vaccination rates showed we were nearing towards our 70% 16+ threshold.

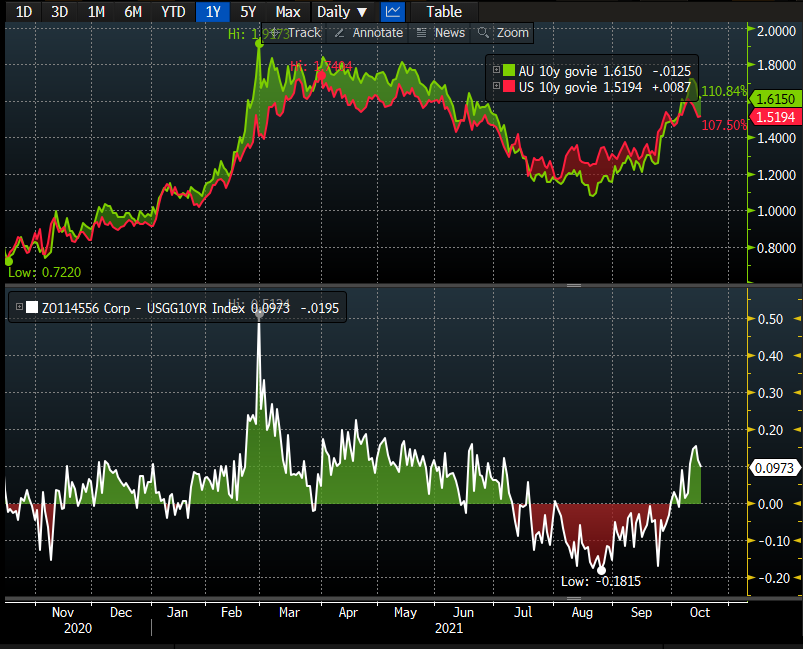

(C)arry

In the past 5-6 weeks, Australian 10y government bond yields have risen from 1.23% to 1.62% at time of writing (15-Oct), where now they are at yields above equivalent US 10y treasury bonds.

The interest rate differential is now +9bp, and whilst this isn’t much, shifts the marginal demand curve for Australian bonds as global investors will have preference for the higher-yielding bonds.

It’s also worth noting the Australian government bond are rated AAA, and our 10y govies are amongst the highest yielding in the world.

This factor starts to re-establish the carry trade, where foreigners will buy AUD in order to buy Australian bonds.

Chart 2: – Australian 10y Government Bond versus USA 10y Treasury Bond

Source: Bloomberg, as at 15-October-2021

(C)ommodities

Part of the catalyst for writing this note has been the sudden surge in industrial commodities, another sign of economic activity.

In the trading period Mon-Thu last week, the London Metals Exchange (LMEX) gained 5.9%, which was deemed to be a sudden strength in demand for commodities, in contrast to the supply side issues that have plagued natural gas, coal, and oil markets, as of late.

This was also reflected in the S&P500 index on Thursday, where the biggest equity market movers were the materials industry, up 2.5% on the day, after a 3.5% jump in copper spot prices, and +3.7% for zinc as well.

All-in-all, the Bloomberg Commodities Index continues to move from strength to strength this year as many nations have pledged large infrastructure spending packages as stimulus to create jobs and future productivity enhancements.

Chart 3 – Bloomberg Commodities Index

Source: Bloomberg, as at 15-Oct-2021

(C)OVID and Central Banks

One of the strongest long-term, real-time indicators for AUD gains has been our terms of trade, referring to the net change of exports relative to imports.

Economically, as we export more relative to imports, our net exports increase, and our terms of trade is higher.

As we export more and more commodities, miners tend to repatriate some to all of their USD receipts back into AUD, which can see the AUD rise.

Thus, a rising terms of trade has historically been associated with a rising AUD/USD exchange rate, where the USD side of the equation is far less volatile than the AUD side.

The cycle would usually happen in this way:

#1 Foreign countries purchase more of Australian exports

#2 Exporters repatriate their foreign currency (usually USD) trade proceeds back to AUD

#3 Financial markets would also be predictive of this relationship and purchase AUD on the expectation of a higher AUD

#4 The increase purchase of Australian exports would see prices shift higher, which would be inflationary, as would the increased monetary velocity

#5 Inflation expectations would rise, and bond yields would trend higher as additional compensation required for investments as mitigant against inflationary risks

However, due to COVID’s impact on our economy, the increasing terms of trade was not met with higher bond yields and inflationary pressure as

- corporate earnings tended to be saved rather than spent or reinvested; and

- the RBA maintained their Yield Curve Control policy, pegging our 3y government bond yield at 0.10%, equal to the Overnight Cash Rate.

Thus, the terms of trade effect was muted and our AUD/USD exchange rate (green line) decoupled from commodity prices (orange line).

Chart 4 – AUD/USD (green) Compared to Bloomberg Commodities Index (orange)

Source: Bloomberg, as at 15-Oct-2021

Looking Forward

As we know, the RBA has begun to taper their bond-buying program and will review in February 2022 whether they can taper it again.

Moreover, they also have opted not to extend their 3y interest rate peg beyond the April 2024 govie, implying they consider the conditions may be appropriate for them to begin hiking interest rates in and around H2 2024.

As this interest rate peg rolls off and as the QE program is curtailed, more and more of our bond supply will be able to free float and likely we see Australian bonds yields above other comparable global bonds again – i.e., above US or UK government bonds.

This will allow increased capital flows as more investors seek carry trades within government bond markets – certainly a market where investors are starved for yield.

This will also happen in the coming months, at a time when China also starts to spend money building facilities for the 2022 Winter Olympics, where they’ve also experienced provincial lockdowns due to a new wave of COVID infections.

In recent weeks there has been increased Chinese economic activity, using iron ore, steel, copper, and bitumen to name but a few key commodities, which should also benefit Australian exporters of natural resources.

Thus, we can consider the AUD/USD has begun its ascendency, likely moving higher, towards “fair value” of 75-78c.

(C)arry has turned positive, (C)ommodities has become more positive, (C)hina is less negative and more neutral, and (C)OVID influences are less negative; all-in-all creating a positive backdrop for our AUD.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.