“Whether ‘tis nobler in mind to suffer

The slings and arrows of higher mortgage rates,

Or to take steps against a sea of troubles,

And by opposing, switching banks to receive lower mortgage rates.”

– William Shakespeare’s Hamlet (between 1599-1601), adapted by Jesse Imer (April 2021)

In April this year we managed to make a fairly astute call that mortgage rates were going to rise due to evolving economic circumstances, as interest rates had based and were putting margin pressure on banking institutions offering home loan mortgage products.

At the time, the view was not common opinion but seemed obvious to us, as 1 to 3-year fixed rate mortgages were on offer below 2%, at a time when funding costs of banking institutions had shifted higher.

Hence, faced with lower profitability and lower net interest margins (NIM), banks were likely to shift mortgage rates higher to maintain their NIMs.

Table 1: RateCity Cheapest Mortgage Rates, as at 12-April-2021

| Term | Rate % |

| 1-year | 1.69 |

| 2-year | 1.74 |

| 3-year | 1.75 |

| 4-year | 1.89 |

| 5-year | 2.14 |

| Variable | 1.77 |

Source: RateCity; Monday April 12, 2021.

This ended up eventuating in May and June 2021, where mortgage rates rose but then remained stable thereafter.

Fast forward six months and borrowers have yet another chance – if they haven’t already – to get ahead of the rising borrowing costs ahead.

Another Chance to Fix

The biggest question variable mortgage rate paying homeowners face is whether to fix now or wait to see if interest rates fall further.

This is mostly a thing of the past and served Australian borrowers well over the past twenty years as on average, borrowing costs fell.

Hence, about 85% of Australian residential borrowers pay floating rates of interest (Source: APRA), rather than fixed rates.

The other factor borrowers need to be aware of is also the optionality of fixed versus floating rate repayments.

Variable (floating) loan types tend to be more flexible and without lock-up periods and can be re-financed more readily without (or less) cost.

There is inherent optionality imbedded into the structure, where if floating and fixed borrowing costs are the same, and interest rates were expected to remain the same, the floating rate loan would be the preferred structure due to the lower cost.

However, at present, there’s now an opportunity cost to not fix a mortgage rate, for all or a portion of one’s mortgage.

[Noting, this is quite a personal choice and should be made in consultation with your banker, financial planner, accountant, spouse etc.]

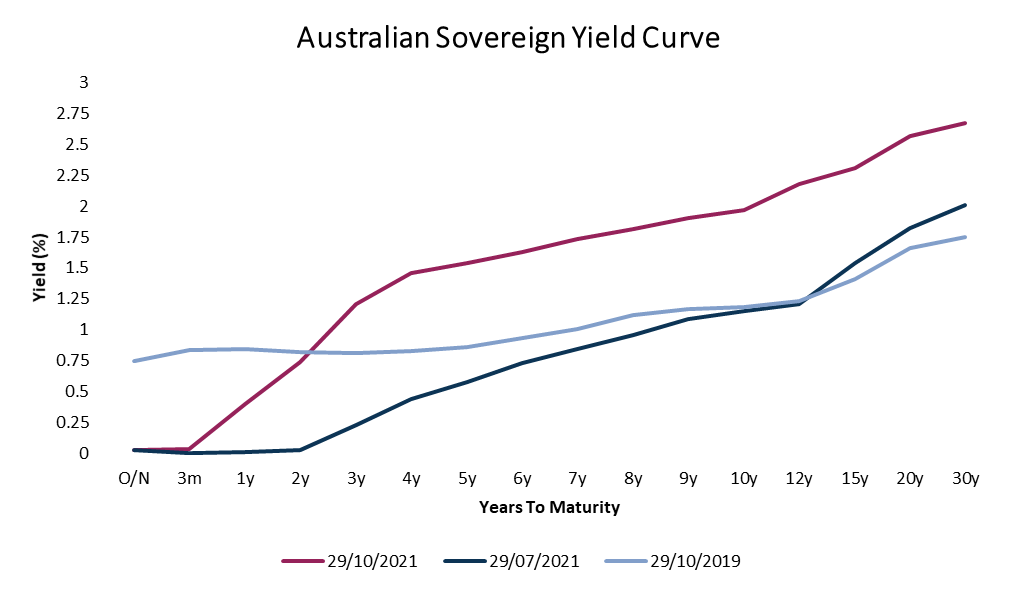

The Yield Curve

The Australian yield curve has shifted in the past few months and specifically in the past four weeks as global bond yields rose as a reaction to perceived central bank hawkishness in respect to the “persistently transitory” inflation, and shifting psychological associated.

Further volatility was experienced last week as the RBA presented less hawkish (more dovish) than the market expected, bringing yields back down slightly, though allowing 1-3year government bond yields to rise above the previous Yield Curve Control target of 0.10%.

Looking at our yield curve now (magenta line), it’s far steeper now than in 2019 (light blue), and with yields 0.5-1.0% higher than in July (dark blue line).

Chart 1: Australian Sovereign Bond Yield Curve

Source: Mason Stevens, Bloomberg

This presents the obvious opportunity that a borrower may be able to fix their mortgage repayment rate at current levels, before the banking institutions seek to raise their rates again in the near future, as they factor in these higher costs.

As they stand, rates have risen across the board since April (our last note on the subject), but all-in-all, haven’t risen nearly as much as the borrowing costs implicit in the bond market movements.

For example, RateCity had advertised a 3-year fixed rate mortgage at 1.75% in April, now at 2.19% in November, a rise of 0.44%.

This is a smaller rise than our 3-year Commonwealth government bond, which has risen 0.57% in the same period of time.

Table 2: RateCity Cheapest Mortgage Rates, as at 3-November-2021

| Term | Rate % |

| 1-year | 2.06 |

| 3-year | 2.19 |

| 5-year | 2.40 |

| Variable | 1.89 |

Source: RateCity; Tuesday November 3, 2021.

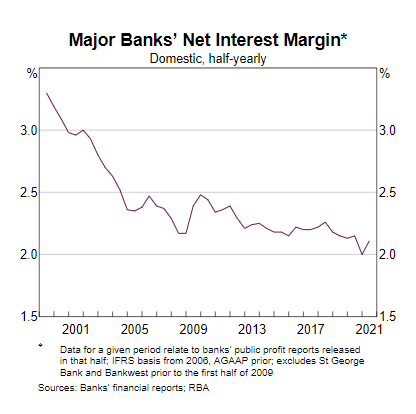

Bank Margins

Looking at the situation from another point of view, banks tend to maintain NIM of ~2-2.25%, as the RBA highlights below.

Chart 2: Major Bank NIM, 1999-2021

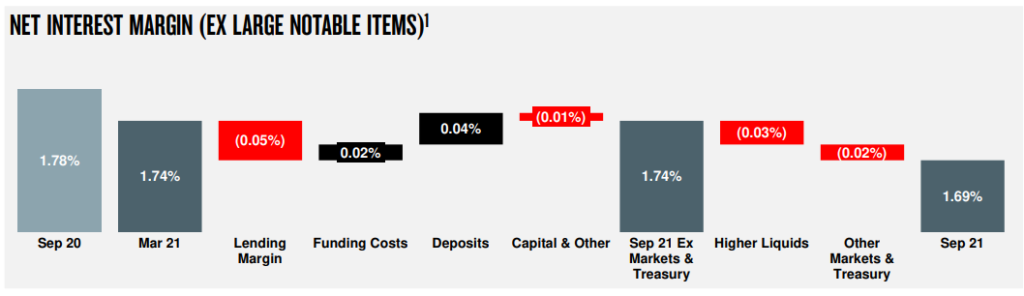

Looking at NAB’s FY 2020/2021 results released earlier in the week, their NIM was 1.69%, historically low, similarly to ANZ, Westpac and CBA’s result 3 months ago.

Chart 3: NAB’’s EOFY Result – Net Interest Margin

Source: NAB 2021 Investor Presentation

Across all the major banking houses, a lot of this was due to a lack of loan (credit) growth, juxtaposed against higher deposit growth seeing lower NIMs.

In future months, NIMs will likely take a further hit as funding costs rise, with no more of the RBA’s Term Funding Facility (TFF) available for drawdown.

This will see increased bond market issuance by banking institutions in both domestic and international markets, as they see deposit growth slow and even contract as we emerge from the pandemic, and as TFF proceeds are repaid over time.

For example, Westpac tapped the USD bond market on Tuesday issuing both senior unsecured and subordinated bonds, raising 5.5 billion USD (approx. 7.4bln AUD).

This was likely a smart decision by Westpac treasury who can see the higher funding costs in their future and the likely need to re-finance the TFF proceeds at higher rates, and hence locked in 10-20-year funding at near historically low levels.

Taking this example one step further, one of the Westpac bond tranches was a three-year fixed-rate senior unsecured bond.

This bond was issued with a fixed-rate coupon of 1.02%, that Westpac will pay semi-annually.

In a simplistic representation of what a bank’s funding cost looks like, if we add Westpac’s current NIM (~1.7%) to their 3y funding cost (1.02%) we would expect a 3y home loan to have a cost of at least ~2.75%.

But no, we can see from RateCity’s rate card that there’s 3y fixed-rate home loans available in the market at 2.2%.

Not to mention that Westpac has an AA- (S&P) credit rating and has one of the lowest cost of borrowing amongst any mortgage issuer in Australia!

Closing Remarks

All-in-all, we would expect for banks to maintain their current NIM and not let them sink even lower, and that they would likely re-price their variable and fixed-rate home loans to higher rates, in the near future.

Therein lies the opportunity for borrowers to potentially re-finance and get ahead of the curve, locking in the low rates, while they last.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.