The RBA met for their 10th and 2nd last Monetary Policy Decision meeting this year, and decided to play things safe by following the recent actions and commentary of the Bank of England, Reserve Bank of New Zealand, Bank of Canada and the US Federal Reserve.

Their media release can be viewed here.

What I mean by stating the RBA is “changing tune” is that they’re following in the footsteps of other central banks to distance themselves from previous and even recently stated economic forward guidance.

Instead, they bowed to market forces and admitted their forecasts were a shade too far from reality (aka. wrong) and those economic conditions have improved ahead of original projections.

As I wrote in September, the RBA does this time to time again (my previous reference to wage price forecasts) and even changes their chart’s axis or look-back history to hide some of their worse forecasts (i.e. made a 20y chart a 15y chart).

Prior to yesterday’s meeting, the policy blueprint stood as follows:

- Maintain the cash rate target at 0.10%

- Purchase $4 billion AUD of government issued securities a week until February 2022 and then review if still required

- Maintain a Yield Curve Control (YCC) policy pegging all government issued bonds maturing before and including April 2024 at 0.10% (in line with the cash rate).

The latter two statements were oft cited as the most important two as the 4 billion/month of QE was providing more and more liquidity to the market, and providing forward guidance that the cash rate would not be increased until after April 2024 (likely in H2 2024).

In yesterday’s meeting, the RBA Board decided to:

- Continue to maintain the cash rate at 0.10%

- Continue to purchase $4bln AUD/month of govies

- Discontinue the YCC of the April 2024 Australian government bond

That implies that they’ll still maintain the 0.10% yield of the Dec 2021, July 2022, Nov 2022, Apr 2023 govies it was already targeting and buying in the secondary market, just not the April 2024.

We would interpret this as a nuanced change in forward guidance, where the likelihood is now on mid 2023 as the period where conditions may be correct for a rate hike, as opposed to H2 2024.

Moreover, this has set precedent that if economic conditions continue to improve ahead of RBA forecasts, they may discontinue the YCC of the April 2023 govie, bringing forward guidance to November 2022.

Likewise, if better yet again, from November 2022 to July 2022, working their way back to the Overnight Cash Rate.

RBA Outlook

The RBA forecast is for GDP to grow 3% over 2021, 5.25% in 2022 and 2.5% in 2023, where they’re concerned about future setbacks “on the health front”.

As several Australian states and territories rebound from the latest delta outbreak and lockdowns, firms are re-hiring, and the unemployment rate (UR) is expected to improve over the medium term.

The Bank’s forecast is for an UR at 4.25% in Q4 2022 and 4% at the end of 2023.

While the RBA is keenly aware that trimmed mean inflation has reached 2.1%, something I wrote about on Monday in the context of the recent bond market sell-off, their central forecast is for sustainable inflation to only pick up and stay in their target 2-3% p.a. band in 2023.

Surprise surprise, that aligns with the new April 2023 YCC and forward guidance for conditions to be right for possible rate hikes.

The RBA media release ended by saying the Board is committed to maintain “highly supportive monetary conditions” in order to facilitate full employment and inflation consistent with their target, where underlying inflation is forecast to be no higher than 2.5% at the end of 2023 and wages increasing gradually.

Market Reaction

In terms of market reaction, there was a patch of volatility yesterday afternoon given there was a broad amount of uncertainty regarding what the RBA make look to do and/or say.

With any form of uncertainty, markets tend to hedge their bets about the expected outcomes and quickly re-price the eventual outcome after the announcement or event.

Yesterday was no exception.

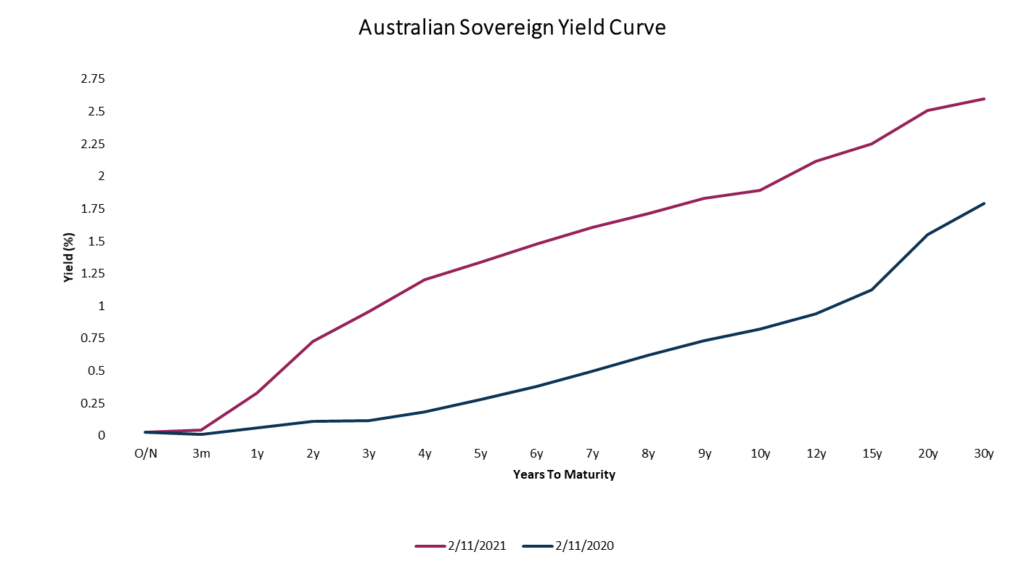

In terms of government bonds, our yield curve (magenta line) has steepened remarkably since one year ago (blue line), where we can see that 1 and 2y government bonds are now trading above the RBA’s YCC target of 0.10%.

This is something we could expect the RBA to do something about in the near-term, but also likely not to fight against in the medium term as they’re now less likely to impose their will on the market, especially if it’s an opposite view.

Source: Mason Stevens, Bloomberg

The AUD/USD exchange rate wasn’t as volatile as I expected, though to be fair, had already been rallying off the 72c mark at the start of October, already factoring in the likelihood of higher bond yields and a less dovish RBA.

Source: Bloomberg, as at 2-Nov-2021

The ASX 200 was barely moved on the result either, rallying ~20-30 points from 7320 to 7350(ish).

This would be viewed similarly to the AUD/USD, where the ASX has already come off from 7443, where it was trading last week before the Q3 CPI print that saw bond markets become more lively.

Source: Bloomberg, as at 2-Nov-2021

Closing Remarks

I can’t help but realise that while some things have changed, the monetary policy setting in Australia is very much the same.

Our cash rate is unchanged, our central bank is buying more and more government bonds and will be doing so for at least another 3 months, and that financial conditions are still relatively easy in Australia, with emergency levels of stimulus still being provided.

For me, I’m fond of using a car analogy where this all comes across as less accelerator, but not yet an outright brake, which would imply a withdrawal of stimulus.

Quite the opposite, by continuing to provide increasing amounts of liquidity to the market through their QE program, conditions are continuing to be eased “quantitatively”.

In terms of timing, in a statement read by RBA Philip Lowe at 4pm AEDST, he states that “the latest data and forecasts do not warrant an increase in the cash rate in 2022. I recognise that some other central banks are raising rates, but out situation is different. The Board will not increase the cash rate until inflation is sustainably in the target range.”

“This is likely to take time. The Board is prepared to be patient.”

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.