Pre-amble: while today’s note is on the topic of equity market exposure to the Work From Home (WFH) thematic, we start by using a new, visual way to represent trends, particularly in economic data and sentiment regarding financial markets.

There is a very cool technology out there which utilises a statistical technique for vector quantisation, a process that analyses signals to partition data into obvious clusters.

This technique is called “k-means clustering”.

While we won’t belabour the data science of this, we want to emphasise that an ability to partition data (observations) into segments (clusters) of a relative mean (average) allows us to visually depict moving trends within the world.

This could be the changing voter preferences of the USA, or the consumer preferences for cereal, or the sentiment regarding monetary policy or equity markets.

In each of these examples, k-means clustering can be utilised to visually review preferences in data.

Source: AnalyticsVidhya.com

With this in mind, hedge funds around the world, such as Renaissance, or investment bank Goldman Sachs, use these data science techniques to analyse sentiment and mood, to get ahead of trends before they are established; where these techniques are by no means a mainstream concept, yet.

I’m personally a subscriber to Epsilon Theory website, which uses a program called “Quid”, created by ex-Google developers and are a leading user of the k-means clustering techniques.

In Epsilon Theory’s instance, they use their Quid clustergrams to review market sentiment, as a source of alpha for investing.

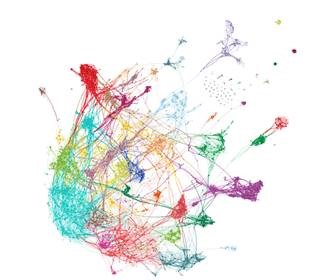

Working From Home Clustergrams

In a recent article, Epsilon Theory produced a series of clustergrams that are a collection of news articles for an entire month (May 2021).

- Each article is about the topic “remote work”,

- Each dot point is an article,

- Lines between the dots are links between stories,

- Distance shows the relative connection,

- Colour represents linguistic similarity,

- Areas of the clustergram appear bold for emphasis.

In the below chart, the dots related to the term “COVID” are bold and are spread throughout the entirety of the picture.

Hence, it is obvious that the work-from-home narrative is driven by COVID.

Duh Jesse.

Source: Epsilon Theory, Quid

Integral to this are the news articles and media reports that explore the role of work within society, corporatism and the capitalist system (bold dots) on the left/middle side of the picture.

Source: Epsilon Theory, Quid

But the BIG BIG BIG topics are all about corporate profitability, worker productivity and the clustergram has a certain gravity to it, (towards the bottom).

Source: Epsilon Theory, Quid

The Trend Towards WFH

The WFH investment thesis is not exactly new, but it has sped up considerably since February 2020.

For example, the Australian Federal government proposed the National Broadband Network (NBN) more than a decade ago with the view that Australia required a newer, better and more robust internet network, accessible at home.

While the current NBN is a pale shade of its original and potential glory, the writing was on the wall at the time of how the world was evolving.

Fast forward to 2020 when COVID interrupted the global economy, it became all the more important to have household infrastructure in place to allow workplaces to continue functioning, outside the confines of the traditional office building.

This sped up the trend of the flexible work environment that empowers individuals and families to continue to work whilst not in the immediate vicinity of a central business district, or while disabled, rearing children and other reasons – there are a myriad.

The WFH Investment Thesis

What we can learn from the clustergrams above are that the global narrative is that remote work is here to stay, and that trend is only speeding up, not slowing down.

It means that it’s becoming common knowledge that companies that restrict remote work too heavily are going to be criticised.

It means that it’s becoming common knowledge employers who roll back remote work programs too soon or altogether are likely to see higher staff turnover (if not already).

It means that workers expect to be able to work remotely, where possible, and for it to be more widespread and accepted in the future.

Which means there’s some very specific trends that are likely to stay around:

Rise of the Home Office and of Home Renovations

We’ve seen this already with the surge in demand for products from Nick Scali (ASX: NCK), Home Depot (NYSE: HD) and Bunnings (owned by Wesfarmers, ASX: WES)

Rise of the Green-change or Sea-change

In urbanised nations, workers relocating away from cities to (generally) less expensive locations or to more ideal locations – near lakes, beaches, forests etc.

This has an interesting implication as wage growth is intrinsically tied to cost of living, and if households lower their costs of living, their arguments for wage increases may wane as well.

This could lead to a significant period of benign wage growth and low inflation if the trend is widespread enough.

While this part of the thematic is hard to profit from – other than simply buying property in the geographic locations perceived to benefit, i.e. Byron Bay in 2020 – it is great food for thought!

Increased Cyber Security Spending

This is a no-brainer topic as workplaces are less centralised and conducted on personal hardware rather than company issued equipment, there’s a need for cyber security to ensure adequate defence against infiltration and attack.

Australia does have some of our own anti-virus and cyber security companies, for example ArchTIS (ASX: AR9), Senetas (ASX: SEN) or WhiteHawk (ASX: WHK), the largest players are generally foreign.

Some of the larger names are Fortinet (NASAQ: FTNT), CrowdStrike (NASDAQ: CRWD), Proofpoint (NASDAQ: PFPT), Norton (NASDAQ: NLOK) and McAfee (NASDAQ: MCFE)

Increased Consumer Spending Through Online Portals and Websites Rather Than Physical Retailers

There are almost too many companies to name that may fit this brief, where we’re thinking about obvious examples such as JB Hi-Fi (ASX: JBH), Amazon (NASDAQ: AMZN), Walmart (NYSE: WMT), Alibaba (HKG: 9988) etc.

Increased Online Gambling

Mike wrote a great note about this in April, where we mention Flutter Entertainment (LSE: FLTR), Ladbrokes and Coral (LSE: LCL) and Tabcorp (ASX: TAH) as some of the largest players, which matters a considerable amount within online gambling as their balance sheet size allows for M&A activity and geographic dominance.

Increased Online Gaming

I wrote about this two weeks ago in my note titled “Pew Pew Pew Pew Pew”, where we cover the mega-trend that is part of the WFH mega-trend as well.

Within this note we mention the VanEck Vectors Video Gaming and eSports ETF (ASX: ESPO), as well as Nvidia (NASDAQ: NVDA), Sea Ltd (NYSE: SE) and Nintendo (Nikkei: 7974) – all varying sources of exposure to this investment opportunity.

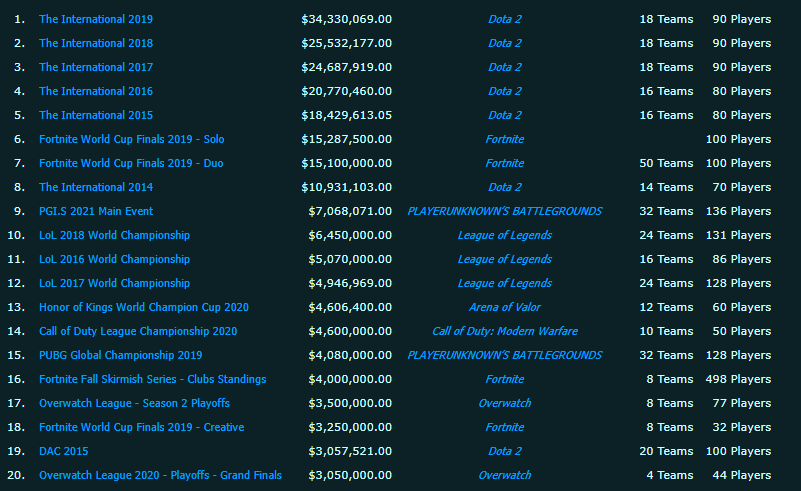

To emphasis this point just slightly more, eSports and online gaming are also going to be growing areas of EMPLOYMENT for people, where vast sums of wealth can be earned by being good at certain games.

Where games such as Dota2 boast prize pools for their version of a World Cup (called “The International”) of over $40 million USD.

Source: Esportsearnings.com, all figures USD

Interestingly enough, an Australian by the name Anatham “ana” Pham is one of the top earners, having won more than 6 million USD in prizes in recent years, before the age of 21.

Yes, he was 20 and already a multi-millionaire and there an entire generation of people that see these stories and want to be just like him, in future years/decades.

How powerful is that?

Closing Remarks

I think we’re all aware that WFH trends are established and growing, the biggest dilemma is how to profit from it within investment portfolios, where the true alpha may be within the eSports environment, in the online gambling, in the cybersecurity demand, or through an organisation that may provide the most amazing online shopping experience.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.