As the COVID-19 pandemic took hold of markets in March of last year, investors began positioning themselves in those stocks deemed to be “COVID Beneficiaries”, like Amazon (NASDAQ: AMZN) and Zoom (NASDAQ: ZM).

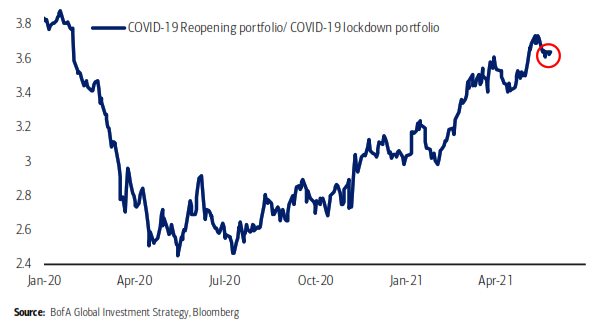

With COVID-19 vaccine developments came prospects of a global economic recovery, where increased production and consumption would see cyclical industries outperform – deemed the “re-opening” or “reflation” trade.

More broadly speaking, there has been a transition from growth stocks – focused on future cash flows -towards value stocks, which are focused on near-term earnings (which we have discussed in length in our recent factor series here and here)

However, as stock markets return to pre-pandemic levels, and much of the economic re-opening already priced into valuations, it leaves us with the question – are markets finished with the re-opening trade or is there still more to come?

In today’s note, we will go over the progress of the re-opening trade to date, its likely trajectory, and the stocks which allow you to gain exposure.

Re-Opening Doors for Investors

After years in the doldrums of investors’ portfolios, value orientated stocks came back into the fore as the re-opening trade took hold.

With the focus placed on near term earnings, those established stocks with steady cash flows reigned supreme.

Industries previously most affected by the global slow down outperformed, with cyclical industries like consumer discretionary, energy and industrials recording strong recoveries from lows.

As interest rates began their rapid ascent at the start of 2021, the bull case for growth stocks began to weaken, with increasing inflationary expectations pushing valuations for high PE shares lower.

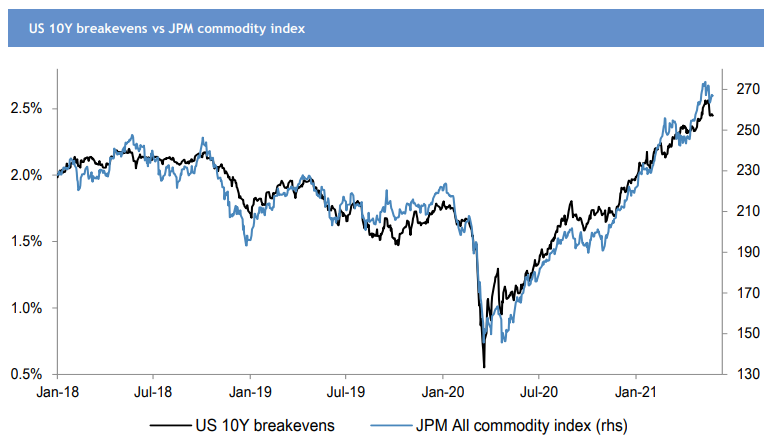

Record high fiscal deficits saw commodity prices soar, with copper, iron ore and lumber all making considerable gains.

Steepening government bond yield curves also saw the return of financials into investor portfolios, with accommodative monetary policy creating favourable funding environments.

Is the Re-Opening Closed?

As many stocks return to pre COVID levels and beyond, the question lingers – is this the end of the re-opening trade?

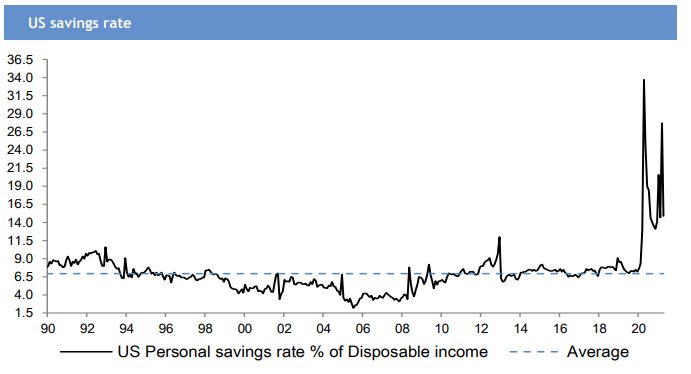

Whilst some may predict that consumer spending is unlikely to increase beyond forecasts, relatively high levels of household savings worldwide has the potential to act as ‘dry powder’ for the economy.

These high levels of savings will support consumption levels as governments roll back unemployment benefits and will be concentrated primarily in domestic economies as travel restrictions still remain in place.

Inflationary expectations also have scope to go higher, with bond issuance set to continue near current rates, and tapering unlikely to occur until next year as central banks seek to ensure that goals of unemployment and inflation are sustainably achieved.

If economies continue to rebound strongly, commodity prices will likely rally further, with this prospect buoyed by continuing record fiscal deficits around the world.

Of particular significance is President Biden’s recent $6 trillion budget proposal, announced in addition to existing hard and soft infrastructure plans under the Build Back Better plan.

This proposal, whilst unlikely to be passed in full, would bring America’s budget spending to post WW2 levels. Despite being funded mostly by increased tax rates, the revenues required would take decades to recoup, and as such would have to be funded in the short term by increased levels of debt issuance.

This debt issuance will continue to impart upward pressure on inflationary expectations, leaving the highly unlikely possibility of a significant retracement.

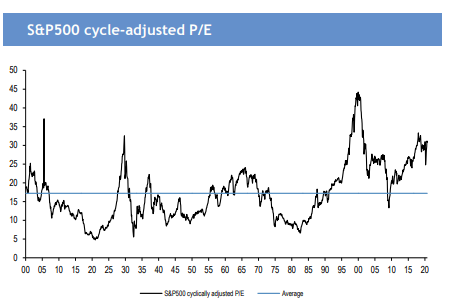

However, when it comes to valuation metrics, stocks are trading at relatively expensive valuations when looking at historical P/E ratios.

Whilst one can make the argument that accommodative monetary policy and substantial fiscal stimulus has created an environment primed for further risk taking, one can also question whether considerable movements up from current levels are possible for a sustained period.

S&P 500 cyclically adjusted P/E ratio

Where Do You Think the Market is Heading?

A range of investment exposures are available for investors according to their perspectives on the trajectories of equity markets.

The Re-Opening Trade is Over

U.S Treasury Yields have stabilised over the past 2 months, trading within a band between 1.55% and 1.75%, with some citing this as a sign of the beginning of the end for the re-opening trade.

This retracement has seen growth regain some ground against value and has rubbed some of the shine off the case for continuing outperformance of the re-opening trade.

One could argue that improved economic outlooks have already been largely priced in, with inflationary expectations and bond yields unlikely to make any meaningful moves in the short-medium term without some erroneous external impact (such a new COVID-19 shock) changing the current macroeconomic landscape.

Investors ascribing to this perspective would want to gain exposure to defensive stocks, such as Woolworths (ASX: WOW) and CSL (ASX: CSL), as well as Australian major banks who will continue to benefit from accommodative monetary policy and a steep yield curve.

The Re-Opening Trade is Well and Truly Alive

With plans for budget deficits for the rest of the decade in many developed countries and increasing inoculation rates around the world, there remains a case for the continuation of the re-opening trade.

Fiscal stimulus will continue to drive increased infrastructure spending and incentivise consumer spending, pushing forward the case for further increases in inflationary expectations.

The question of whether inflation is transitory, or a more permanent feature of our economies will remain unanswered until later this year/next year, however demand imbalances in certain commodities look likely to remain in the short-medium, albeit at potentially lower levels.

Increased inoculation rates will also unlock further consumption, assisted by high levels of household savings, particularly in the travel industry which has yet to recover fully from the pandemic.

Historically, value investing tends to outperform growth during periods of above average growth and rising inflationary expectations, with investors able to gain exposure to this trend through ETF’s such as Vanguard’s Value ETF (NYSEARCA: VTV).

More specific industries such as travel (ASX: QAN, ASX: WEB), commodities (ASX: FMG, ASX: BHP) and energy (ASX: STO) can expose investors to more specific trends within the re-opening trade.

Where to Next?

It may be the case that both of the above circumstances do not eventuate, with another scenario becoming increasingly more likely where economic growth trends will become more bifurcated.

What we do know for certain is that governments will continue to run fiscal deficits, and central banks will maintain accommodative monetary policy until unemployment and inflation targets are met – which is likely to take a number of years.

As a result, companies will continue to remain in a favourable environment – the only question is the extent to which this has been factored into valuations.

Investors wishing to hedge away risks of further movements in growth and value stocks should ensure that their portfolios are diversified, and the utilisation of other investment factors such as quality and momentum.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.