Energy markets are back.

This week WTI Crude hit 7-year highs, Newcastle coal hit all-time highs, and last week, US natural gas hit 7-year highs.

Price moves like this might make you think we’ve pivoted to a “recarbonisation” of the world – a fossil-fuelled utopia which reoccurs within Scott Morrison’s dreams on a semi-regular basis (a refresher for if anyone forgot when he brought coal to question time).

Chart 1: Newcastle coal (red line), WTI Crude (blue line), and Natural gas (green line) futures as at 19/10/2021

Source: Bloomberg

Instead, what has transpired is an imbalance between supply and demand – where energy networks have been unable to increase supply to keep up with economic re-opening activities.

These supply bottlenecks have largely been the result of reduced production capacity since the onset of COVID-19, as well as years of underinvestment in non-renewable energy infrastructure.

Similar episodes of supply and demand imbalances should continue to occur in the coming years, albeit at a much lower level, given the time it will take to build out reliable, renewable baseload energy sources, and the lack of financing and support available for non-renewable energy sources to build out supplementary capacity where required.

This will contribute, in part, to the 1-3% inflation p.a. which Bank of America forecasts will occur as a result of our move towards net-zero emissions.

However, these developments should not come as a surprise to our readers, given our prediction that investors had undervalued the monumental task of transitioning our energy mix from fossil fuels to renewables, which has subsequently set up an oil and gas bull market.

In today’s note, we will cover the coal market – its role in the overall global energy mix, and its prospects over the short and long term.

The Coal in Our Engines

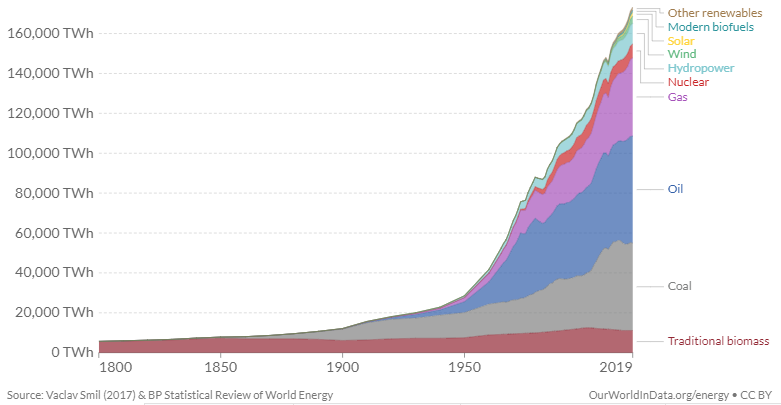

Coal has played an important role in our global energy mix since the Industrial Revolution and is currently the second-largest energy source in the world, though its weight in the overall energy matrix has declined over the past few decades.

What we have historically seen during the development of nations is the transition from older and less efficient energy sources, to newer and more efficient sources.

This transition takes time and requires nations to reach certain levels of economic prosperity, where they can justify making the substantial capital investments into more energy-efficient sources.

Chart 2: Global Primary Energy Consumption by Source

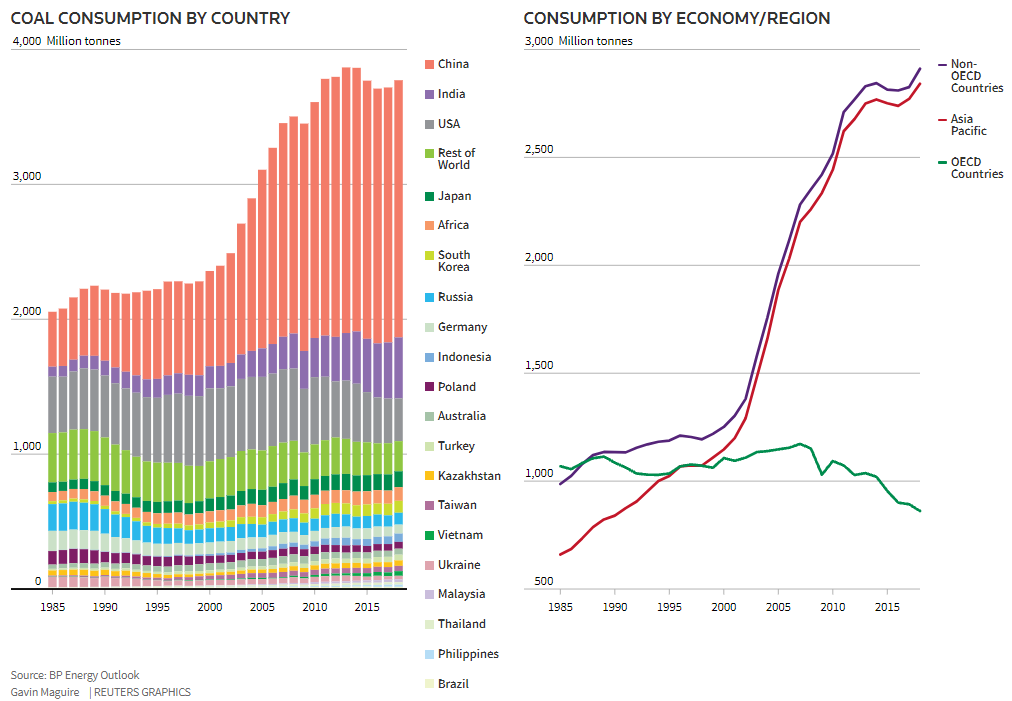

As it stands, the largest consumers of coal are India and China, but most importantly in the chart below, almost all consumption growth over the last 3 decades has come from non-OECD and Asia Pacific countries.

Chart 3: Global Coal Consumption (2018)

So, therefore, we should see global coal demand taper off as non-OECD nations slow their consumption growth and reduce overall consumption as they enhance their levels of economic prosperity, and transition towards more efficient and environmentally friendly energy sources.

The pace of this change will also likely be accelerated by global environmental pressures, with the UN’s upcoming Climate Summit likely to place further pressure on those nations reliant on coal, given it is the single largest source of global temperature increase (International Energy Agency 2019).

However, not all coal can be viewed as the same.

Coal differs through its use cases, where thermal coal is used for energy generation, and metallurgical coal is used for steelmaking.

Coal also differs in terms of its quality – where it varies by calorific value per kg, with higher quality coal providing more efficient energy.

When it comes to transitioning out of coal, ample renewable energy sources exist for energy generation, where solar, wind, hydro, nuclear and geothermal can all be adequate replacements.

Yet when it comes to the production of steel, there is currently little alternative to metallurgical coal – where hydrogen is the main alternative, but given the developing technology and current cost barriers, this method is not ready to be used at scale.

As a result, coal will likely remain in demand for the coming decades, particularly from nations undergoing significant infrastructure investment like India, who are one of the only nations growing their consumption of coal.

The Short Term: Undervalued and Underappreciated

Commodities tend to operate in boom and bust cycles.

When prices are low, investors commit less capital to the industry, and the least efficient producers are taken offline.

Supply falls, but eventually, demand outpaces supply and prices begin to increase again.

As prices increase, producers are incentivised to explore new projects, and previously unprofitable mining becomes once again, profitable. Supply increases, and eventually outpaces demand, starting the cycle anew.

For the coal sector, as well as for oil & gas, this cycle of boom and bust has held true for many years, though as investors seek to attach greater weight to ESG, producers are unable to attain the same relative levels of funding as in previous cycles.

As such, they are currently unable to expand supply to take full advantage of moves higher in spot prices.

This will continue to generate price volatility, where supply will be relatively inelastic in times of appreciating prices.

To play this unfortunate by-product of our move towards net-zero, investors could elect to invest into Whitehaven Coal (ASX: WHC), or Yancoal (ASX: YAL), who are two of Australia’s largest pure-play coal exposures.

Chart 4: ASX: WHC (red line) and ASX: YAL (blue line) performance since 20/10/2016

Source: Bloomberg

Holding such a position over a longer period of time would likely result in underperformance against the index, as well as being subject to headline-driven volatility (which was exhibited through Whitehaven’s sharp drop once the Chinese coal ban was announced), nevertheless, these securities can act as a point of alpha generation throughout short-medium term time periods.

The Long Term: Net-Zero Upside

Over the longer term it is hard to justify a position in coal, given the odds are stacked so heavily against you.

Coal stocks may seem “cheap”, but it’s not as if their valuations are guaranteed to normalise, where they will continue to be excluded through ESG screens and potentially fall even further out of favour with investors due to environmental concerns.

Moreover, it will continue to remain on the wrong side of regulation, where coal will likely become more expensive as an energy source as companies are forced to either integrate carbon capture technology or purchase carbon credits to offset their emissions.

A Burning, But Fading Fire

Coal is an industry which is under fire, where its negative environmental externalities necessitate a transition to cleaner energy sources.

However, we can’t make this transition overnight, where it will require decades to create the technology, build the infrastructure, and in the case of nuclear – alter public opinion – to phase out coal.

What we will see is a preference for higher-quality coal (given their lower relative contribution of emissions), as well as growth in technologies which reduce the emissions of coal production and consumption.

For investors, whilst short-term value may lie in coal producers, long-term value can be found in these emissions-reducing technology (like carbon capture), or in more environmentally friendly means of mining and processing fossil fuels.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.