One of the most important news stories over the past few months has been the escalating Ukraine-Russia tension, where the threat of invasion has continued to linger over the world as negotiations continue to fall afoot of Russian demands.

Uncertainty regarding the possibility of conflict is rife, as juxtaposing messages have emerged from each side, where Moscow has maintained that it has no intention of invading Ukraine, whilst President Biden has warned that the threat of invasion is imminent.

With a dearth of understanding on where this conflict might head, we must consider the worst possible outcome (Russian invasion) to understand the potential impact it may have on various geographic regions, asset classes and industries.

As the topic of today’s note, we will go over a brief summary of the conflict, the sectors which may be positively or negatively affected by conflict, and the ways in which investors can incorporate this crisis into their risk management frameworks.

Before we start, I’d just like to flag that I am by no means an expert on Russian/Ukrainian geopolitics, and that some of the concepts explained may simplify issues into a format which is digestible and below 1,300 words.

Whilst the topic of this note will be market centric, we must also acknowledge the unfortunate social impacts of an invasion, where the safety and wellbeing of Ukrainians would be put at significant risk, both from armed conflict in the short-medium term, and also in the medium-long term should Ukraine lose its sovereignty.

Where Are We Now?

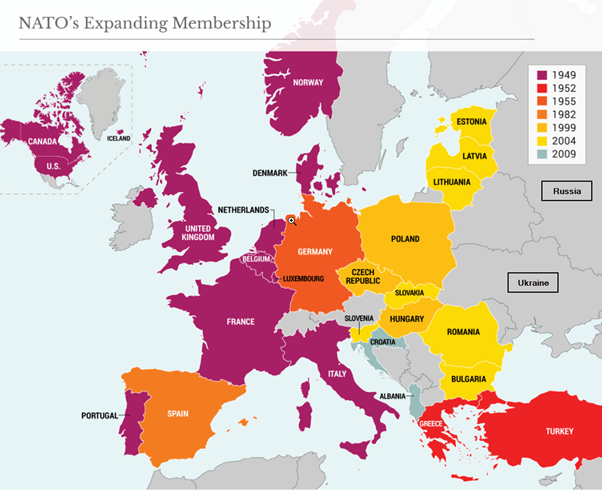

In order to understand the motivating factors behind this invasion, it is important to take a look at the geopolitical history of the region – primarily in the form of the expansion of NATO member nations.

In the past, Russia (and formerly the Soviet Union) has always aimed to maintain a buffer between itself, and Western Europe to protect against potential conflict (previously referred to as the Intermarium/Iron Curtain).

Over the past decades, this buffer zone has continued to erode as NATO’s reach expanded eastward.

Source: Geopolitical Futures, Mason Stevens

In 2008 at the Bucharest Summit, NATO even took the step of promising future membership to both Georgia and Ukraine – on the basis that they meet eligibility requirements.

This never eventuated given admission into NATO requires unanimous acceptance from all 30 member nations, as well as the accomplishment of 3 key criteria, being:

- Functioning democracy based on a market economy

- Fair treatment of minority populations

- Commitment to resolve conflicts peacefully

Whilst Ukraine’s accomplishment of the 3 criteria can be brought into question (given their lack of democratic stability and issues with corruption), the main reason why they have yet to be admitted as a NATO member nation is due to the conflict it would likely cause for other member nations.

Admission as a NATO member nation implies that NATO member nations would be required to assist in the event of any armed conflict – with these nations currently unwilling to add Ukraine given the instability in the region (Russo-Georgian War, Crimea Annexation etc).

Whilst they likely won’t be admitted in the near term, Ukraine’s desire to eventually join NATO is one of the key motivating factors behind Russia’s aggression, whose demands in negotiations include:

- For Ukraine and other former Soviet nations to never be granted admission into NATO

- NATO to limit its deployment of weapons and military presence in Eastern Europe

In order to communicate their demands, Russia has gathered an estimated 175,000 troops along its border with Ukraine, along with tanks, self-propelled artillery and short range ballistic missiles.

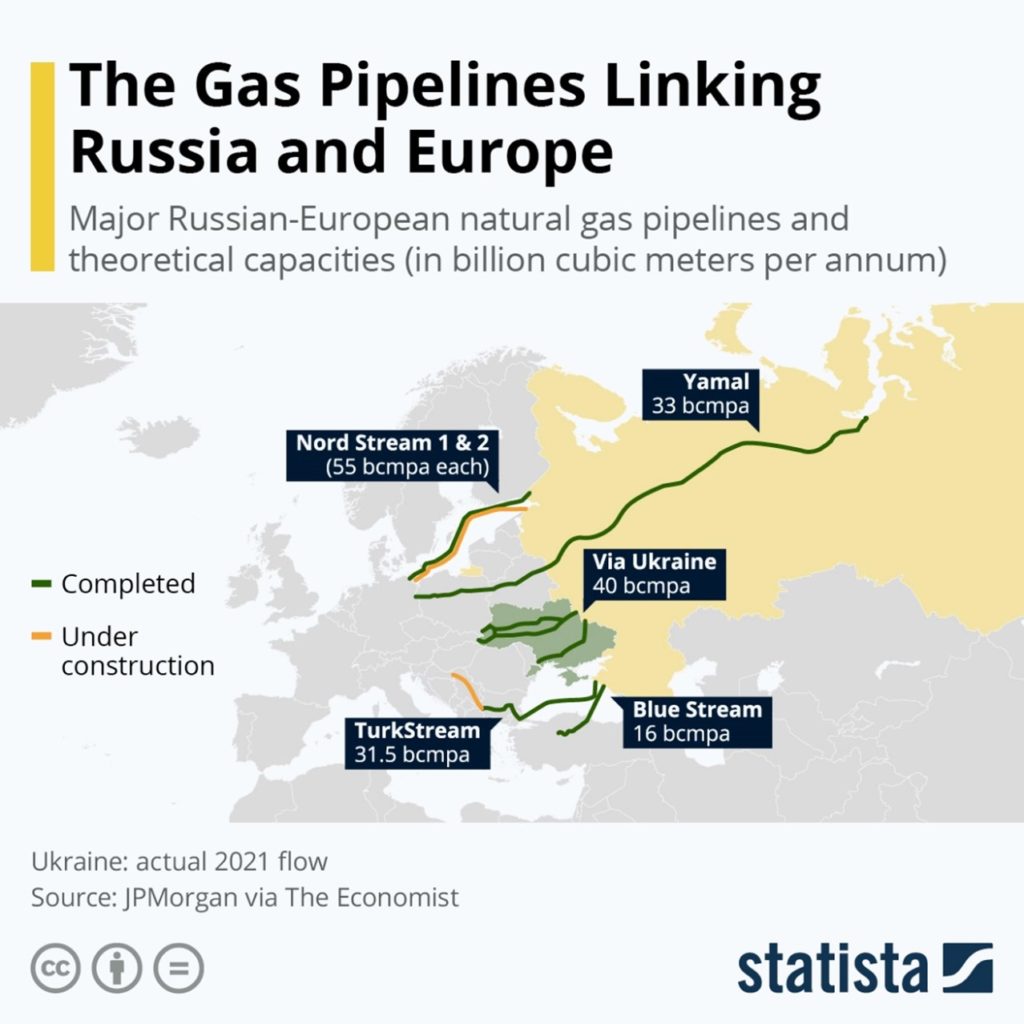

In response, the US has threatened significant economic sanctions with the removal of the Nord Stream 2 pipeline from future natural gas pipeline networks should Russia invade, although talks between both parties have been fruitless to date.

Implications for Energy Markets

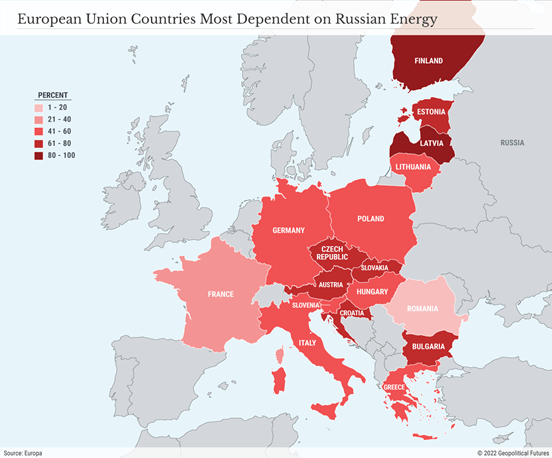

From a markets perspective, the largest concern from the potential conflict is the disruption to energy supply chains.

Source: Geopolitical Futures

As a result, Russia holds a position of power over many of these nations who have little alternative to satisfy their energy requirements, limiting the ability of these countries to implement economic sanctions and contribute to armed conflict.

On top of this dependence formed by many European nations, Ukraine is the proprietor of several pipelines which connect Russia to Europe, which if damaged during conflict, would have significant implications throughout several European countries in the short-medium term.

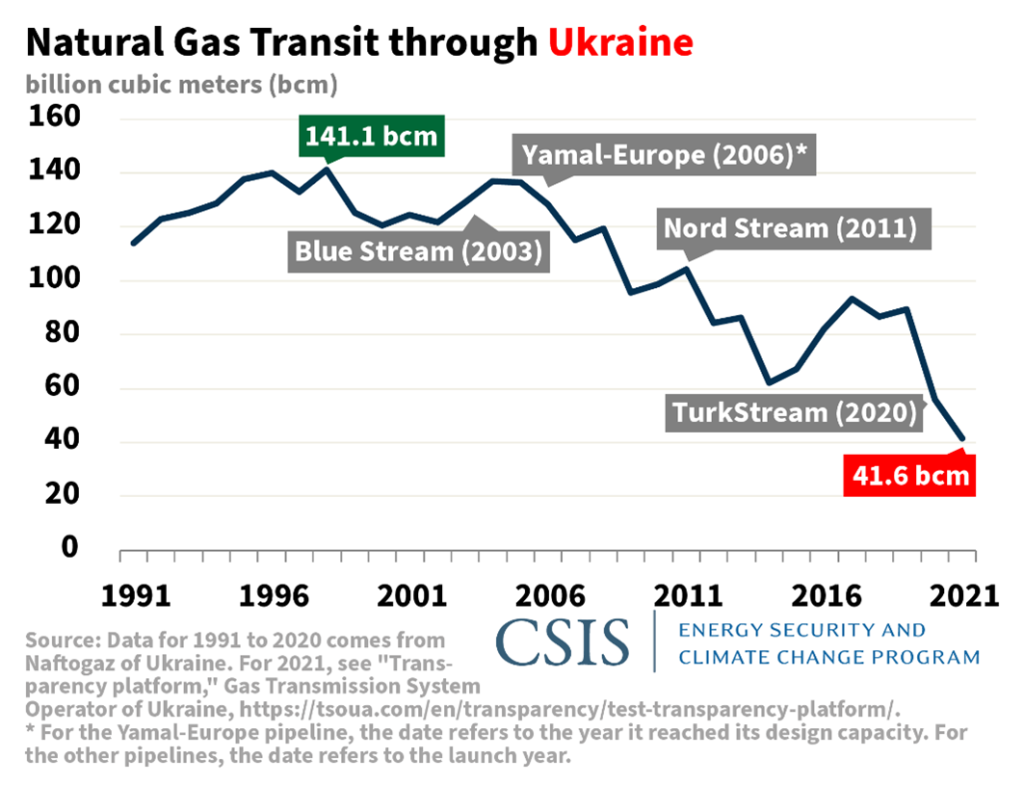

However, the amount of natural gas transported through Ukraine has fallen over the years, lessening the importance of Ukraine to Europe’s natural gas network – which is only set to be exacerbated once Nord Stream 2 comes online.

In the event that countries attempt to reduce their dependence on Russia, or in an event where supply chains are disrupted, other natural gas companies around the world will stand to benefit from the additional demand – with prices already rising on the back of these fears.

Chart 1: 1-year performance of Brent Crude and Natural Gas futures

Source: Bloomberg

Investors wishing to benefit from further disruptions in energy supply chains can gain a diversified exposure through the Energy Select Sector SPDR ETF (NYSEARCA: XLE), which aims to replicate the energy sector in the S&P 500 – with most of these companies have little to no exposure to Russia or Ukraine.

Implications for Global Markets

Whilst the Russia-Ukraine tensions have received significant attention in the news, it is unlikely to have a significant influence on the global economy.

The majority of its impact would be centralised in the surrounding countries, who would be directly affected by disruptions in supply chains and economic sanctions, and would likely see Europe underperform vs other DM economies over the period of the conflict.

However, countries like Australia and the US will likely have to deal with the prospect of higher inflation from broad based increases in energy prices, although the extent of this will be determined by the ability of other suppliers to meet demand.

In the immediate aftermath of the invasion, bond yields would likely rally as investors seek safety, although a continued period of risk-off sentiment would be unlikely to remain at a global level.

Central banks will likely disregard any tension or conflict when determining their stance on monetary policy, given the fact that movements in the cash rate would be unable to resolve supply chain issues, and would only act as a detriment to economic activity.

Another scenario which is oft mentioned is the likelihood of there being no conflict.

Should Russia and the US reach a form of agreement, and Russian forces were to be withdrawn – we would likely see falling energy prices as the market removes its “conflict premium”.

Whilst this is likely to be on the optimistic side of things, it is not inconceivable to consider that this crisis will be resolved peacefully.

Unlikely to Impact Australian Portfolios

For many Australian investors, the conflict in Ukraine is unlikely to make a mark on their portfolios.

The economic impacts of conflict will largely be confined to Europe, where most Australian and US equities will remain largely unaffected.

Energy names look set to the most affected, although investments in companies who are not exposed to the region should offer relative protection.

Appropriate risk management should only focus on these two areas – where other geographies/asset classes will remain largely unaffected by the conflict.

Despite this, it is still important to maintain a basic knowledge as the situation unfolds, given geopolitics can be one of the hardest fields to forecast and understand.

It may be that this situation evolves into something far beyond what we can currently foresee, and have a basket of implications for all investors around the world.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.