Markets have faced a troublesome few months, with uncertainty rising higher than it was earlier in the year. Central banks are now truly realising the magnitude of inflation that they are faced with, and with that we are almost seeing a race to the top for cash rates between central banks.

Whilst inflation is still dominating the headlines on the news, financial markets have begun to shift their focus towards the prospect of recession as rates rise quickly as central banks try to combat high inflation.

Back in April Matt wrote a note discussing where gold was priced and how it can also be used as an indicator.

With these concerns growing around a looming recession and the recent pull back in gold prices we feel it’s worth taking another look at everyone’s favourite shiny yellow metal, gold.

Recession looming?

Earlier in the year the risk of recession was a fairly muted discussion with many investment banks holding views that suggested there was a very low change of recession for this year with the chance still small but growing next year. These views have now changed with banks now increasing the risk, Morgan Stanley updated their forecasts for recession this year from 20% to 35%, Citi has also updated their forecasts with an aggregate probability of recession now at 50%.

As we can see, there are varying schools of thoughts currently circulating around markets & the risk of recession, with bulls, bears and even some more solitary views coming through investor discussions.

Recently BAML outlined what they had been seeing in these three schools.

They noted that the bulls are piecing together a variety of pieces of information to argue that inflation is near its zenith, and that the market has bottomed as a result.

They’re adamant that the fed finally “gets it” and will raise cash rates, bringing Mortgage rates above 6% resulting in a likely cooling in the housing market. They also claim that goods spending is starting to fall as consumer sentiment dwindles, material prices are starting to fall, along with jobs. The bulls feel that with all of this and EPS cuts on the horizon, a new base to equity markets is forming that can offer attractive investment opportunities.

The bears are still roaring, and perhaps even louder than before. They feel the fed doesn’t get it, and that they aren’t even trying to ‘thread the needle’ anymore… they’re simply “smashing it” as a last resort to combat inflation, removing any chance of a soft landing the equity market so dearly craves.

They believe that with cost-of-living pressures continuing to rise, food and fuel will continue to strangle the consumer, and that the switch from goods into services spend will not be sufficient to cool inflation. If they’re right, we could see even bigger EPS cuts putting an even lower floor from here for markets.

Now, the lone soldiers, they’re certainly acting as contrarians – at least to what the media is telling us. They feel the consumer is still very healthy, which is possibly true thanks to large savings accumulated over covid, meaning they can withstand inflation for longer. If that’s the case though, does that mean rates have to go even higher to tame inflation as inflation can continue to rise with strong consumer savings? And if it does, does that just mean we’re at an even great risk of a hard landing and recession?

Gold’s performance in recession

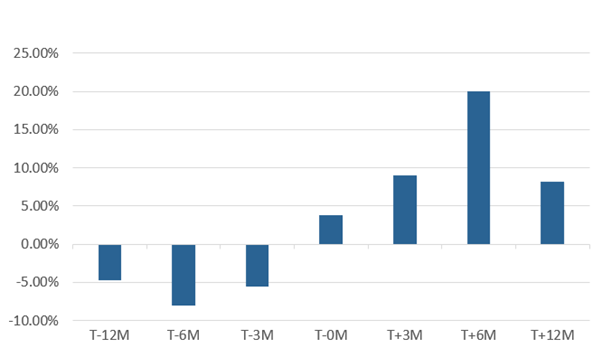

So, what do we know about how gold acts around recession? Historically, gold markets sell of leading into a recession, then find solid levels of support in the midst of recession and finally rally as economies come out of recession.

The chart below shows the median annualised lognormal gold price returns leading into the past 5 US recessions.

1981-82; 1990-91; 2001; 2007-09 (GFC); 2020 (Covid-19)

Source: Mason Stevens

While gold markets typically sell of leading into a recession, that doesn’t make them an informant to financial markets that recession is imminent. In fact, 2 of the past recessions saw rallies into them, however this was due to external factors not consistent with more ‘normal’ recession scenarios.

The GFC recession saw gold rally into it as a result of the commodity super cycle that was present at the time. The most recent recession during covid also saw a rally into it as the fed decided to embark on a mid-cycle loosening of financial conditions.

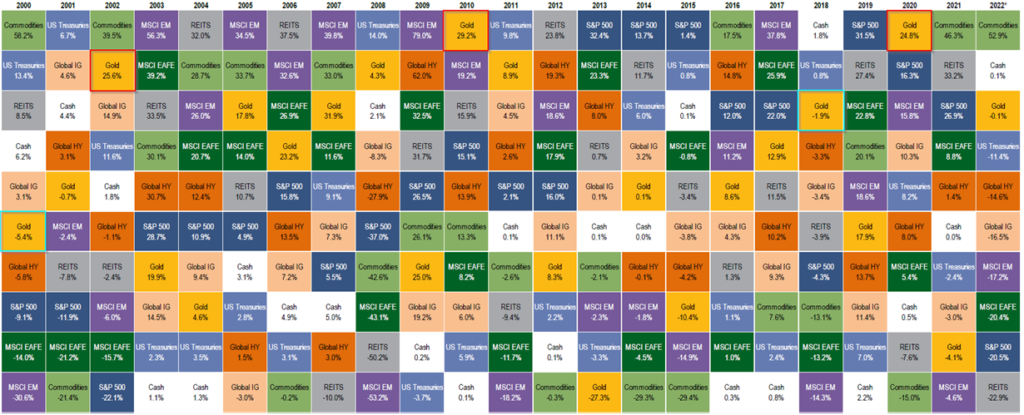

The below chart from BofA highlights the cross asset returns by year, since 2000. In the chart we can further see how the above has played out historically.

Source: BofA Global Investment Strategy, Bloomberg. *2022 YTD

Adding gold to portfolios?

Depending on where you sit with your view about recession you may want to look at adding gold back into your portfolio after the recent pull back in price.

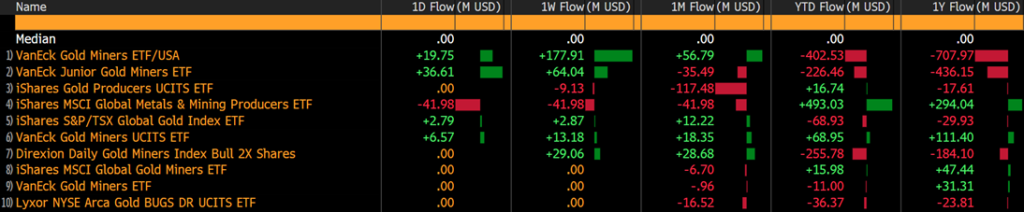

This year we’ve seen sizeable outflows across gold names. However, in the past week sentiment has certainly shifted as we’ve begun to see capital pour back into some of the gold ETFs.

The below points to that notion, where we can see positive net flows over the past week, as well as outflows over the longer term across some major gold names.

Source: Bloomberg as at 17/06/2022

If your view is that we are around the T-6M to T-3M range above then you may be wanting to look at adding in some exposure, and even more so if you’re feeling we are closer to T-0.

In our view the best ways to gain exposure are through a few names. In terms of gold miners, VanEck Gold Miners ETF (GDX:US) is one option, it looks to replicate the NYSE Arca Gold Miners Index as closely as possible. Another miner option is the BetaShares Global Gold Miners ETF (MNRS:AU) is a currency hedged ETF with the objective of tracking the performance of the Nasdaq Global exAustralia Gold Miners-Hedged AUD Index.

If you prefer to have exposure more directly through gold bullion, then perhaps the BetaShares Gold Bullion ETF – currency hedged (QAU:AU) is a way to go, another option for gold bullion is SPDR Gold Shares (GLD:US). Both of these aim to reflect the performance in the price of physical gold bullion less expenses.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.