Evergrande has received significant attention in mainstream press over the past few weeks, as its potential default has spelt concerns of “contagion” throughout the global economy.

Being the most heavily indebted player within the Chinese property sector, it can be viewed as a “canary in the coal mine”, reflecting the health of one of the largest industries in the one of world’s largest economies.

Within our fixed income team, we have had front row seats to the whole saga as Evergrande bonds have continued to decline since June of this year, far before mainstream media headlines.

The next chapter of Evergrande’s story is yet to be determined, as the world waits to see what level of accommodation the Chinese government will provide for Evergrande and its major stakeholders, as well as the Chinese property sector more broadly.

As the world’s most indebted property developer, the worst-case scenario of default has the potential to be a major market event.

As of the writing of this note, unconfirmed reports have emerged that Hopson Development (HKG: 0754) will purchase a 51% stake in Evergrande’s property development arm for USD$5 billion – with both shares going into trading halt pending a major announcement on Monday.

In today’s note we will cover the history behind the Chinese property sector, the factors that have driven current events and the likely outcome.

A Story of Debt, Debt and More Debt

As a communist state, the Chinese government has always maintained ownership of all land since its establishment.

However, the roots of the Chinese property boom can be traced back to 1988, where the government changed the constitution to enable the use (but not ownership) of land to be bought and sold under long term leases.

This constitutional change paved the way for the development of a residential housing sector – which boomed as China urbanised, and demand for residential property soared, particularly within coastal provinces.

At the centre of it all were the property developers– who were able to purchase the rights for cheap land, and turn this into the mega cities we now know today.

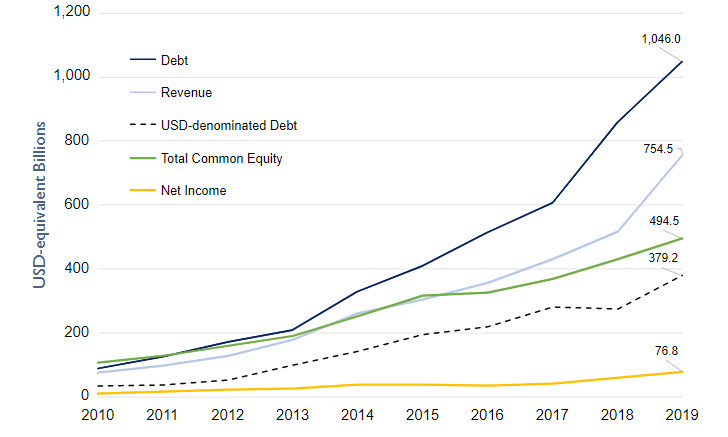

Since its listing in 2009, Evergrande has been able to grow its land bank from 55 million square metres to 231 million square metres, across 234 cities and 798 projects (Evergrande annual report 2020).

Much of this expansion has been fuelled by debt – where it had a net debt-to-equity ratio of 153% at the end of 2020 (Evergrande earnings 2020).

Similar stories have transpired through its competitors, who have all used significant amounts of debt and leverage to expand their land portfolios, where 8 of the 10 most indebted property developers are now based out of China.

Listed Chinese Property Developers and Home Builders (2019)

Source: Seafarer Funds

The Three Red Lines

In response to record levels of debt, the Peoples Bank of China and the Ministry of Housing announced the implementation of new financing rules for real estate companies, where developers wanting to refinance would be assessed against three thresholds, termed the “three red lines”:

- 70% ceiling on liabilities to assets

- 100% cap on net debt to equity

- Cash to short term borrowing ratio of at least one

If developers meet all three requirements, they can increase debt by a maximum of 15% in the following year.

These regulations were implemented to stifle the overheated housing market, and avoid the negative consequences of a debt driven housing bubble like what was seen in Japan.

In response to these regulations, property developers with weaker balance sheets sought to sell down existing exposures – with Evergrande offering discounts of up to 30% on new properties.

The picture these regulatory changes have painted is one of reduced future growth and reduced liquidity, subsequently decreasing the ability of heavily indebted developers to continue on their trajectories.

The First Domino to Fall?

The Chinese property sector accounts for 14% of GDP, and 25% of GDP if indirect contributions are included (JP Morgan 2021).

The collapse of Evergrande would see a considerable reduction in the economic growth prospects of China and would likely see the collapse of many counterparties within China’s banking, and shadow banking sector.

Moreover, even though its competitors may not be in the same situation as Evergrande, considerable mark downs have already occurred in their bonds, as investors prepare for the possibility of “contagion” through declining housing valuations and the collapse of businesses within the housing supply chain.

However, comparisons made between the collapse of Lehman Brothers and this current episode are inaccurate – where the sphere of influence of Lehman Brothers spanned the entire globe, and in a multitude of industries, where Evergrande is largely confined to China, and almost entirely within the property sector.

This limited geographical sphere of influence is reflected through Evergrande only holding USD$20 billion of USD denominated debt – a small portion when looking at its total outstanding debt of USD$310 billion.

Whilst the Chinese government will want to make an example of Evergrande, it must be noted that the property sector holds considerable importance within China, through it successfully enabling the largest urbanisation movement in recorded history, and being a key factor in much of the economic growth which China has experienced over the last 30 years.

Therefore, given its long-standing integration within the long-term Chinese government strategy, it can’t be viewed in line with technology, education and other industries which have also recently been in the press.

As a result, it’s unlikely that we will see the Chinese government merely watch on as the effects of a default ripple throughout its economy.

However, the Chinese government will face an issue where it will want to ensure that Evergrande does not default (given its reduced ability to assist once this occurs) but will likely be unable to simply bail them out given the politically unsavoury nature of such an action.

Key Events for Evergrande

As the details surrounding Evergrande’s position are relatively opaque, there are a few things which we will have to watch when monitoring this situation.

- Will Evergrande meet its interest paying obligations?

Evergrande has sought to prioritise its onshore debt over its offshore debt, and has so far missed two offshore coupon payments which were due on the 23rd and 29th of September.

However, it must be noted that Evergrande has 30 days to meet these coupon payments, until it is deemed a default event.

Therefore, the following weeks will determine whether or not these bonds will go into default – something which Evergrande has provided no colour on.

In regards to its onshore debt, coupon obligations have been met through “private negotiations”.

- What level of support will the Chinese government provide?

The question of whether or not the Chinese government will provide support is something which is yet to be answered.

The form and extent of this support will determine the trajectory of this crisis, with any developments set to shape the direction of Chinese equity and fixed income markets.

- How will its competitors and creditors perform in response?

In order to see whether there is truly a “contagion”, it will be important to monitor Evergrande’s competitors and creditors.

For its competitors, if confidence in the sector and real estate valuations continue to decline, those most indebted could end up in the same situation as Evergrande.

If this does occur, the situation could devolve into something much worse, and much more difficult to resolve through government support.

The largest property developer in China, Country Garden, is rated Baa3 by Moody’s (S&P equivalent of BBB-), and its bonds have experienced little impact from the Evergrande fallout – with the majority of its debt still trading above par.

Sunac China, on the other hand, has seen its bonds fall slightly, owing to its weaker balance sheet, only having a credit rating of Ba3 from Moody’s (S&P equivalent of BB-)

Country Gardens = COGARD, Sunac China = SUNAC

Source: Bloomberg

Evergrande’s largest creditor, Minsheng Bank, has a total of 30bn Yuan in outstanding debt with Evergrande and has seen its equity valuations slide in the past few months.

Source: Bloomberg

Contagion or Just a Cough?

It is clear that Evergrande will never be the property developer it once was, where its fate will be determined by the scope and scale of its recovery.

What will shape the trajectory of the market will be the level of government support for Evergrande, and its affected counterparties.

In a worst-case scenario, a significant portion of Evergrande’s most indebted competitors will face the same fate – which would likely lead to a situation much more severe then what we have currently seen, and with much more ramifications for the global economy.

However, if the economic consequences increase, so too will the level of accommodation from the Chinese government, especially when considering the importance of the property sector with China’s current, and future economy.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.