However, other commodities stand to benefit from humanities fourth, and arguably most important energy revolution.

These beneficiaries include copper and nickel, who will play vital roles within the development of electric vehicles (EV’s) and the construction of renewable energy networks.

Chart 1: 2019 vs 2030 Demand Growth for EV Battery Materials

Much like lithium, these commodities play an important role in enabling the use of renewable energy sources within our daily lives.

From an investment perspective, success will obviously be determined by levels of consumer demand, but also by the elasticity of their respective supply chains and the ability for companies to maintain operating margins.

Government support, like that of Prime Minister Morrison’s recent conceit to supporting the Australian EV industry will play a key role in determining the pace and scale of our energy transition, where considerable co-operation of governments; both within their nations, and between other nations, will be required to reach our net zero emission targets.

The main beneficiaries of our move towards more renewable energy sources are of course not limited to these two commodities, where nuclear could play an equally important role (should societies gain a greater understanding of their relatively low levels of risk), and hydrogen, if technology were to develop to a point where it is able to become a scalable and efficient energy source.

Honourable mentions also go to cobalt, aluminium and various rare earths, which we won’t explore in this note for the sake of brevity.

Copper – The Key to a Greener Future

Copper is arguably one of the most important metals in the world due to its high conductivity, making it a preferred material for electricity generation and distribution.

For generations we have used it in construction and industrial machinery, however these use cases have now expanded to EV’s and electricity grid infrastructure – particularly within solar and wind energy generation.

When we look at alternative materials, there is nothing which can compete with the electrical conductivity of copper, where aluminium, the next best alternative, requires two times more material to conduct the same amount of electricity (Wood Mackenzie 2021).

Therefore, the case can be made that copper is almost as valuable as the renewable energy technology itself – as there is no other material which can transfer energy from renewable sources, to consumer applications as cost-efficiently as copper.

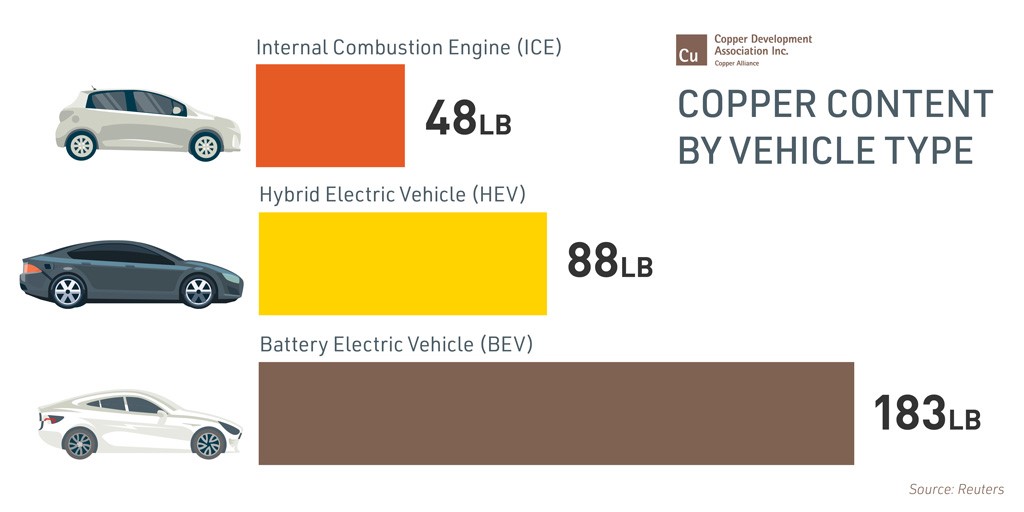

While they are already used within Internal Combustion Engines (ICE), EV’s use up to 4 times more copper given the greater amount of electrical conductivity required, being used throughout the motor, inverter and electrical wiring.

As the size of the vehicle grows (into buses and trucks), so does the proportional increase in copper usage, where electric buses can use up to 16 times more copper than their ICE counterparts (Wood Mackenzie 2019).

Chart 2: Copper Content by Vehicle Type

Source: Copper Development Association, Reuters

Moreover, copper is a vital component within EV charging stations, which will have to be built around the world to accommodate the greater amount of EV’s. Wood Mackenzie estimates that by 2030, there will have to be over 20 million EV charging points around the world, which will consume 250% more copper than 2019 levels.

When it comes to renewable energy grid networks, copper also plays a vital role in solar and wind energy, where their conductivity enables us to efficiently transfer energy from the environment, into batteries.

In order to scale up production to meet these rising sources of demand, miners will have to invest over USD$100 billion over the next 10 years, where we will have to create 8 mines the size of the world’s largest copper mine (BHP’s Escondida mine in Chile) by 2030 just to meet increased levels of demand.

However, given copper mines have already been established and producing for many decades, the supply and demand story is not as attractive as lithium.

Moreover, the ability to recycle copper will see a reduction in new demand as time goes on.

Nonetheless, copper can still make up a valuable portion of one’s decarbonisation portfolio, where it offers a point of diversification away from more volatile lithium markets.

Available exposures include US based Freeport-McMoRan (NYSE: FCX), Canada based Lundin Mining (TSE: LUN) and Australia’s Oz Minerals (ASX: OZL).

Chart 3: 1 Year Performance of FCX (brown), LUN (red) and OZL (blue), indexed to 100.00

Source: Bloomberg

Other large players like BHP (ASX: BHP) and Rio Tinto (ASX: RIO) make up large portions of the market but are too diversified to be viewed as a copper play.

Nickel – A Vital Component in EV Batteries

The nickel story is one which is largely confined to EV batteries.

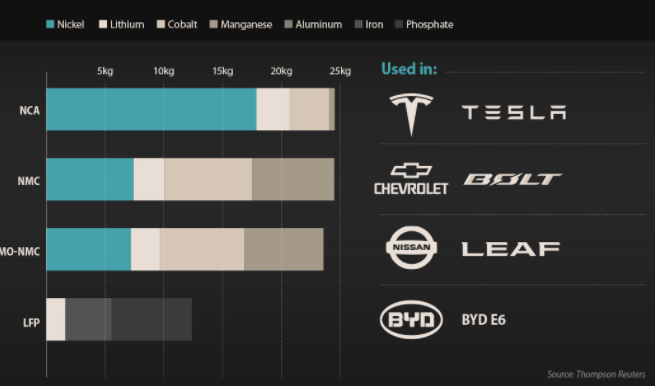

Before we look at the role of nickel within EV batteries, we need to zoom out and take a look at the different types of EV batteries, which are:

- NCA (Lithium Nickel-Cobalt-Aluminium-Oxide)

- NMC (Lithium Nickel Manganese Cobalt Oxide)

- LMO (Lithium Manganese Oxide)

- LFP (Lithium Iron Phosphate)

Each of these types of batteries carries different characteristics, where they differ in terms of cost (due to underlying materials required), life span, performance, energy capacity and safety.

The highest performing EV batteries all contain nickel, which is due to its high energy density, where it makes up approximately 80% of NCA batteries and 33% of NMC batteries.

This greater energy density enhances the distance which EV’s can travel – something which is a constant issue raised by prospective buyers.

Chart 4: Metal Content in EV Batteries

It can also act as a substitute to cobalt, which is one of the most expensive components within an EV battery.

The battery itself often makes up around 25% of the total cost of the car, so a reduction in battery costs can have a material impact on the overall profitability of EV manufacturers.

Such is the importance of nickel, that Elon Musk promised a “giant contract for a long period of time” to any company able to extract nickel in an efficient and environmentally sustainable manner.

However, since that promise, Musk and Tesla have moved away from their initial NCA battery model and shifted towards an LFP battery for their standard range cars, given the lack of nickel supply available in the market.

Importantly, their mid to long range vehicles will continue to use NCA batteries given the greater performance, where Tesla will likely return to NCA batteries if nickel supply improves.

Should other carmakers follow Tesla and move away from NCA and NMC batteries, and towards LFP models, forecasted nickel demand will drop significantly.

When it comes to nickel exposures, there are no major companies which offer a “pure play” exposure.

Australia’s IGO Limited (ASX: IGO) offers exposure through a range of EV related materials, where they mine nickel, copper, cobalt and lithium.

Importantly, they are the only company globally who is producing these four key EV battery metals.

Chart 5: 1 Year Share Price of IGO

Source: Bloomberg

Companies like Nickel Mines (ASX: NIC) do offer more pure play exposures, however, a large portion of their production is in nickel pig iron, which is unsuitable for use within lithium-ion batteries.

Other major miners are relatively diversified like BHP (ASX: BHP), Anglo American (LSE: AAL) and South32 (ASX: S32).

A Future Defined by a Handful of Commodities

The picture is pretty clear – in order for us to decarbonise our economy, we need to be able to transition from fossil fuels to renewable energy sources over a short period of time.

In order to make this transition, we need to take energy from our environment, and transmit this into our consumer products in a manner which is convenient and efficient.

The transmission of this energy is something which only a select number of commodities are able to accomplish, who will all stand to benefit from significant increases in demand over the coming decades.

Given the severity of our climate crisis, and the scale of change required to meet our net zero goals, this increase in demand must be rapid and unyielding.

Whilst the prices of these commodities have all risen over the past year, we are only in the first innings of our renewable energy transition, with a long road ahead of us before we reach net zero.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.