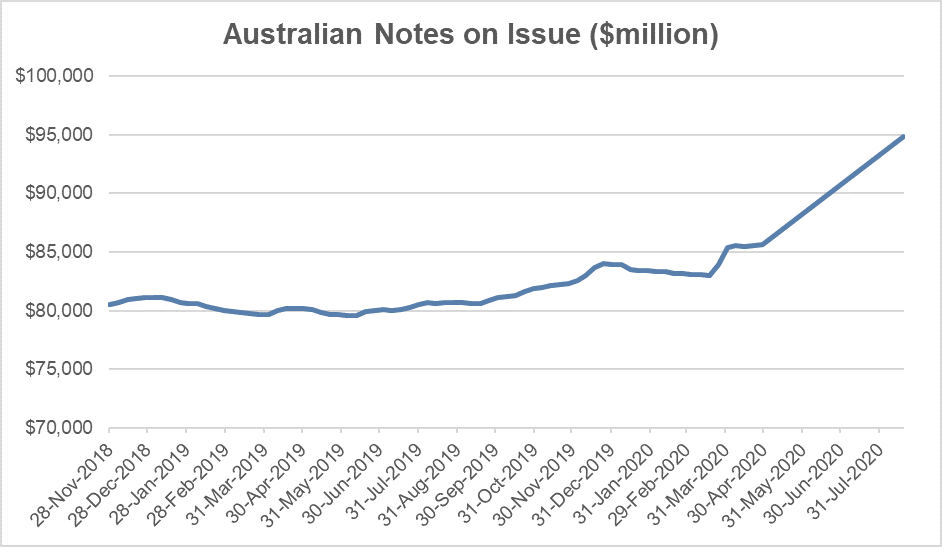

Worried Australians have stockpiled fresh Australian banknotes during the current pandemic, with Note Printing Australia issuing over $10billion worth of new notes year to date, increasing the total supply of bank notes 13% from 84 to 95bln AUD.

This is an interesting data point as this has happened during a healthcare scare where cash transactions have declined and electronic payments such as EFT or tap-and-go have surged.

While some have attributed this to people wanting to keep “some extra money at home”, I believe this isn’t so simple and may be individuals and corporations seeking to avoid any future perceived threat of negative interest rates.

Source: RBA, Mason Stevens

A little background – Note Printing Australia

Note Printing Australia (NPA) is a wholly owned subsidiary of the Reserve Bank of Australia and produces all our domestic currency and passports in a state-of-the-art facility in Craigieburn, Victoria.

NPA is known for producing the first polymer (think: plastic) banknotes back in 1988, and also prints banknotes for several other countries (New Zealand, Canada, Romania, Vietnam etc.) due to its high standards of quality and difficulty to counterfeit.

The NPA facility in Craigieburn is also comprised of a National Banknote Site that has been operational since August 2018. This site stores, processes and distributes banknotes to domestic bank branches based on demand for currency.

Logistically, NPA keeps inventory for “management purposes” so that it can accommodate growth in the number of banknotes due to seasonal fluctuations in demand, or to meet contingency needs in the event of systemic shocks.

However, they produce new banknotes (like they are currently doing) based on demand (“consignment”) where commercial banks are requesting new cash to be printed.

Source: RBA Annual Report 2019

Cash stockpiling and recessions

We first started describing economic downturns as “recession” or “depression” from the Great Depression.

Prior to this, these drop-offs in economic activity were described as a “panic”

An economic panic – such as the downturn resulted from earthquakes, wars, pandemics and business cycles sees a rise in “precautionary savings”, relative to individuals’ incomes.

This is due to increased uncertainty of future events, and people save more money because of the unknown future.

This has been very common in previous pandemics of the last eight centuries.

So why the cash hoarding now?

This pandemic is no different to others in that the increased uncertainty has led individuals and companies to stockpile cash assets.

This refers to not just physical cash, but cash in a bank.

Cash is:

- a store of value and

- exhibits “optionality” as it allows investors and speculators to take advantage of perceived lower prices that may be available in the future.

Large cash positions are being accumulated because of both these reasons.

But what about negative interest rates?

The merit of holding increased amounts of cash is less when cash assets are not a store of value, because of negative interest rates.

i.e. Negative interest rates cause cash in bank to no longer be a store of value. This means that if you hold $100k in a bank account and the interest rate on the account is -0.5% p.a. – something experienced in Europe right now – then your $100k will be worth $99,500 in a year.

But if you hold PHYSICAL cash, a bank can’t charge you a negative interest rate and it can be avoided.

Also, if you are a banking institution, physical cash or bank account cash makes no difference, they’re both considered High Quality Liquid Assets (HQLA) for your liquidity purposes and all reporting as a cash asset on your accounting statements.

Meaning, if you are a banking institution then there’s no penalty in your regulatory metrics for holding physical cash or electronic cash.

Reading the tea leaves

As mentioned, NPA issues new bank notes subject to (new) demand.

Banking institutions request physical cash from the RBA/NPA that is delivered to branches around the country or kept in the NPAs storage facility for safe keeping.

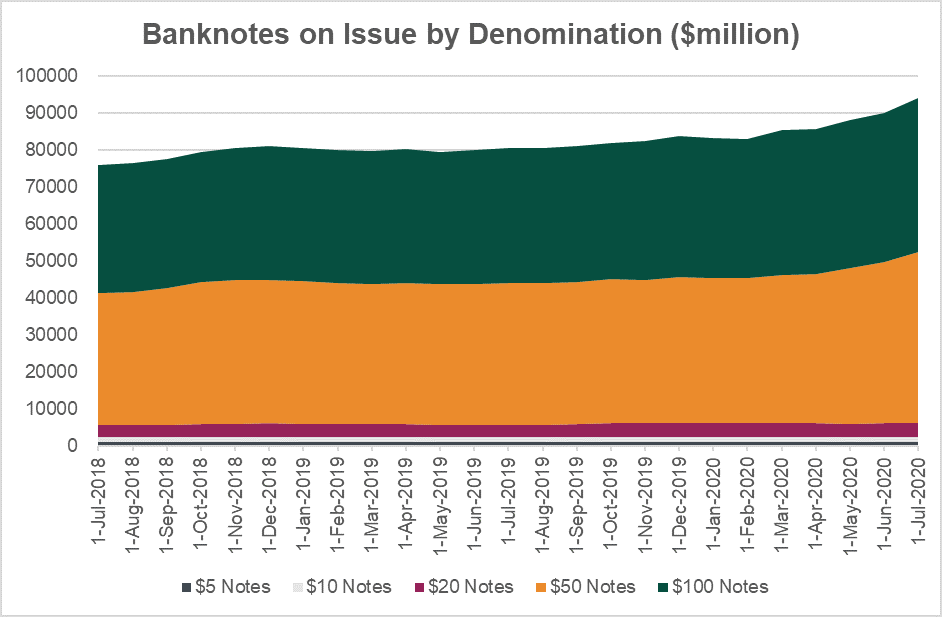

The RBA publishes a month-end summary of the current banknotes on issue, by denomination.

I find this data very telling as it shows what notes are in demand.

At present, $50 and $100 notes are those being withdrawn, while $5 and $10 note supplies have decreased this year.

The retirement of $5 and $10 notes makes intuitive sense during a pandemic as the notes more commonly used in small, physical transactions are less demanded and we see a net decrease in circulation as they’re slowly destroyed through being lost/damaged and not being replaced.

This surge in $50 and $100 notes isn’t startling, as when stockpiling cash, one would want to hold as much value as possible in the least amount of physical notes possible. Using large denomination banknotes suits this purpose.

Source: RBA, Mason Stevens

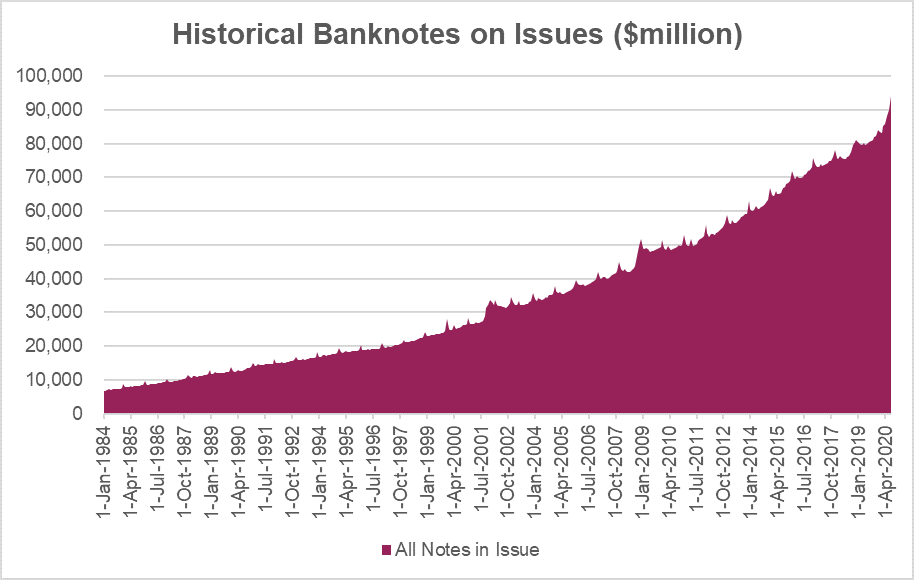

Negative interest rate hypothesis

The RBA publishes historical data from Jan 1984 to present, and never in that 36-year history have we seen a spike in bank note issuance such as this – not during the last two global recessions in 2001 and 2007/2008 GFC, or the previous Australian recession in 1991/1992.

Source: RBA, Mason Stevens

This leads me to believe that a combination of individuals, fund managers, bank treasuries and corporations are getting themselves ready for any potential negative interest rate policy.

I am hesitant to assume the large $10bln increase in note issuance is retail/individual customers because of the sheer volume of new issuance, but also that individual bank accounts are less likely to be passed negative interest rates – something evidenced in Europe where after 5 years retail customers receive 0% interest but not negative interest. However, I note that this fact will not be well known to most Australians.

Corporations, bank treasuries and fund managers, however, will be the first to receive negative interest rates as is common across Swiss (CHF), European (EUR), Japanese (JPY) and Swedish (SEK) banking systems.

Closing remarks

The RBA has been transparent regarding their view that they are unlikely to lower the Overnight Cash Rate (OCR) to a negative interest rate.

However, I am also aware that markets can force central banks’ hands by pricing in these rates, and that individuals and businesses can simply not believe the RBA at its word.

For these reasons I believe that banknotes on issue will continue to grow – and likely for similar reasons that gold as a financial asset has seen renewed interest in recent months.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.