With the post-pandemic bull market rally ending earlier this year, and as the economy moves to a tightening cycle, we are seeing a disparity between the consumer’s sentiment and their balance sheet.

Consumer sentiment is at multi-year lows, yet household wealth is at multi-year highs.

A decline in sentiment can be expected considering the rapid pace of economic change in the last few months, however high savings reserves may provide a protective buffer to transition from an environment of ultra-low rates and high asset values.

Consumer Balance sheet strength

The pandemic had adverse effects on many individuals’ incomes and businesses, however those less affected found themselves with a similar income but less to spend on, resulting in an increased savings rate.

With interest rates near zero and this increase in savings, investors looked towards investments such as equities and property for yields. This saw strong rallies in equities and house prices. The ASX200 was up 62.29% over the two-year period after the March 2020 lows.

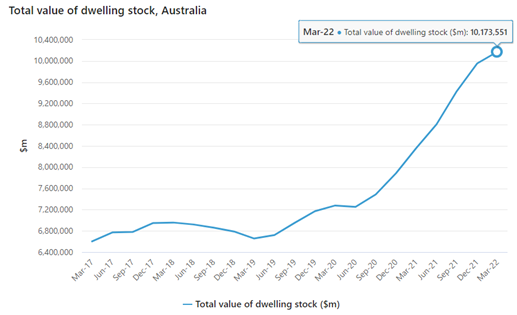

The median increase in house prices for Sydney and Melbourne respectively was 16.4% and 9.4% for the 12 months to the end of Q1 2022. More notably was the change in regional property increasing 29.1% in NSW and 17.4% in VIC over the same period.

Source: ABS Total Value of Dwellings March 2022

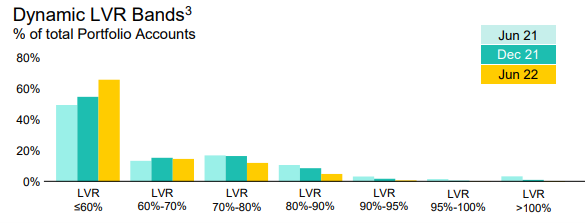

A key measure of leverage in a mortgage is the Loan to Value ratio (LVR), a measure of the value of the loan as a percentage of the property value.

The chart below shows the increase in the proportion of CBA client mortgages falling in the lower LVR bands.

Source: Commonwealth Bank Australia

This implies that investors on average may not be as highly leveraged as some fear.

Consumer sentiment

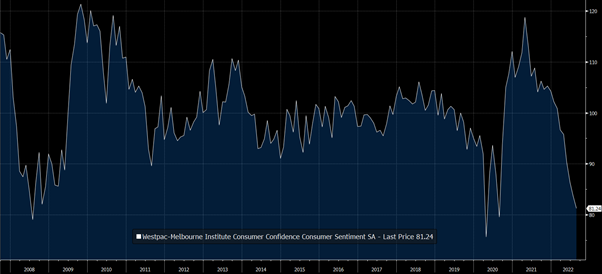

In contrast to this apparent resilience is consumer confidence, which is at the lowest levels since the COVID-19 pandemic.

The August figure for the Westpac-Melbourne Institute Consumer Confidence printed at 81.2 and marks the 9th consecutive monthly decline.

To put this number into perspective, the figure was 76 at the midst of the pandemic 79 in the GFC and is down 21% since the start of the year.

Source: Bloomberg, Mason Stevens

There has been no shortage of catalysts for a decline in sentiment this year with rising geopolitical tensions, high inflation, rapidly rising interest rates from most central banks and the unwinding of Quantitative Easing (Quantitative Tightening), a process not experienced before.

There is a fear of the unknown regarding how well central banks can navigate this tightening cycle.

In question is whether we will experience a recession and if so, what the severity of this recession will be.

One of the driving forces in the decline in consumer confidence is the rapid pace of interest rate rises and the fear of how much mortgage payments will increase.

The RBA cash rate was at 0.1% in April 2022 and is now at 2.35% with markets expecting a terminal rate of 3.775% by July 23(ASX 30 Day Interbank Cash Rate Futures Implied Yield Curve as at 6/9/22).

This is coupled with inflation at the highest level in 20 years with Australian CPI at 6.1% YOY.

The result of this is an increase in the cost of living for most Australians as the cost of essential non-discretionary goods (housing, food, energy) increase significantly.

It is clear to see from this why one may have concerns as to how they will be able to cope with these additional costs, and economists are looking into how this will affect spending on discretionary goods.

So, what does this mean?

This current period could be defined by the number of unknowns, and one of the most significant fears is the fear of the unknown.

However, as inflation shows signs that it could be peaking and the yield curve begins to settle, there are many signs that the market is increasingly digesting this new economic cycle.

It is known that individuals will come under strain and that spending will most likely decrease, but what is emerging is that the average consumer is well placed to endure this period.

The doom and gloom of house prices falling has been well reported, but stress testing done by banks displays less systematic risk.

Many consumers are ahead of their repayment schedule due to taking advantage of low interest rates for the past two years. This creates a buffer which reduces the loans in arrears when simulating the effects of continued rate rises.

These points are important when we look at the economic outlook and the probabilities of three debated outcomes: no recession, a shallow recession or a deep recession.

The chart below shows that average household net wealth is above pre-pandemic levels and above the level when the GFC hit. While a fall is expected, it is falling from a higher baseline.

Source: Goldman Sachs Global Investment Research, ABS

Real household net wealth has risen 27% over the past two years, providing more of a protective buffer than when leading into previous downturns.

Whilst a forecasted decline in asset prices and real wages, consumers are still better positioned to handle the financial strain.

This would help to limit a contagion effect of the housing defaults and stock market collapse seen during the GFC which would lead to a deep recession.

Investors may decide to sell in order to manage costs rather than being forced to sell due to not being able to make mortgage repayments.

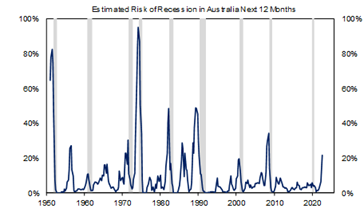

Goldman Sachs models are currently pointing to a 20-30% chance of recession over the next year and 30-35% over the next two years. These odds roughly double if the US enters a recession.

Source: Goldman Sachs Global Investment Research

Whilst market sentiment is negative, the strong balance sheet increases the probability of a mild over a deep recession if it was to occur.

How to play this

There is a rather well-known bias in stock markets where the market tends to overreact to negative news and under react to positive news.

If risk is managed adequately and thorough research is conducted, negative market sentiment can present opportunities to purchase high value stocks at discounted prices.

Investors that have taken money out of the market and want to reinvest it over the coming months may look to index ETFs as a lower volatility way to reinvest capital.

Two examples of such ETFs are A200.ASX, BetaShares Australia 200 ETF tracking the ASX 200 and IVV.NYSE iShares Core S&P 500 ETF.

Index ETFs aim to replicate the index and provide a way increase diversification without transacting in many different equities.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.