There are two under-appreciated types of risks that investors continually face, and we can categorise them both as “tail risks”.

Tail risk refers to the likelihood of very large impacts to portfolios, greater than we would expect under typical statistical assumptions.

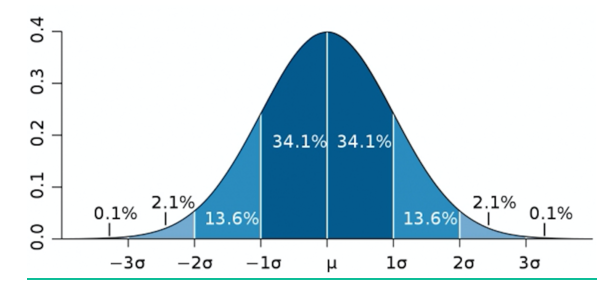

We are used to thinking about probabilities in terms of the familiar “normal” distribution, otherwise known as a bell curve, that looks like this.

The normality distribution is simple in that 68% of expected returns fall within one standard deviation (one sigma) of the average expected result, and that 96% of the expected area falls within two standard deviations from the mean (2 sigma).

The misunderstood part is what occurs outside of that 96% area, the “tails” of the bell curve, where investors can experience great upside gain or downside pain.

Both tails are a “risk”, but pardon me for not being quite as worried about an asset suddenly appreciating in value, as I am one that may crash.

Nassim Taleb wrote a book on this topic in 2007, called “The Black Swan: The Impact of the Highly Improbable”, which I would recommend as an enjoyable read, as Taleb uses philosophy as the lens to explain complex statistics and misunderstood risk exposures.

The Second Derivative

Cast your mind back to high school calculus, where to find the first derivative of a function we find the rate of change for Y with respect to X (dY/dX).

Said otherwise, we’re finding the sensitivity of Y variable to changes in X.

The second derivative is to look at the sensitivity of the first derivative to fluctuations in the rate of change, where we measure the acceleration or deceleration of an object, or the changes of curvature of a line.

We call this 2nd derivative convexity, and it is everywhere in finance.

There’s convexity in bonds, also known as “gamma” in options.

Convexity is what blows someone’s investment portfolio up, or sees them make exponential gains.

And once you know about the 2nd derivative, you can see it everywhere.

Take for example the VelocityShares Daily Inverse VIX ETN (NYSE XIV) in Q4 2017.

People were happy with the 100% returns over the 2017 calendar year to December, until they saw a 99% loss in a matter of weeks and the ETN was liquidated at $6/share after crashing from $142.

You might look at that chart and say okay, that was an ETN that had exposure to leveraged derivatives, that doesn’t happen as quickly in stocks and bonds right?

Well it can, if we remember what happened to US bank stocks in the GFC.

Let’s use Citigroup (NYSE C) for example:

Citigroup equity slowly traded from $300 USD/share in 2003 up to $550 in 2007, but then lost 88% of its value during the 2007/2008 recession.

What we can take away from this is that:

- A positively convex asset goes up faster than it comes down

- A negatively convex asset goes down faster than it goes up

Most stocks are negatively convex, as per the metaphorical adage “prices go up on an escalator and down on an elevator”.

Risk Off Investing

Which brings us to the catalytic reason for writing this note.

We’ve noticed that many investors are speaking to our asset management team recently about covering themselves for a potential risk-off event in the near future, a left tail event.

This may not be a high-conviction projection, but it does indicate that there may be an increased perceived likelihood of a 2+ standard deviation event, that may have adverse consequences for investment portfolios.

And no, these investors are not worried about a positive 2+ standard deviation event that would be categorised as a “melt up” or right tail event, where asset prices quickly rally, we’re talking about the potential for a negative equity market event and seeking to hedge this risk.

Risk Off Series

It’s always handy to be prepared for unexpected events in financial markets where we can have go-to strategies to manage risk and return if something sudden occurs.

Hence, we see it as a topic worth exploring in greater detail in the coming days and weeks.

We’re going to be following this note with more in-depth articles, covering potential go-to strategies such as:

Bonds:

- Long interest rate duration to get exposure to positive convexity and safe haven demand

- Long US Treasuries and other development market government bonds

Currency:

- Long JPY for safe haven protection

- Long USD for similar reasons

Equities:

- Selling growth and momentum stocks and rotating into value and quality

Alternatives:

- Long volatility

- Long-short fund managers, a type of “style” investment

- Long precious metals and real assets

Where we also encourage you to get in contact, should you want to talk specifics regarding your own investment portfolio’s composition.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.