At its meeting on Tuesday 6 December, the RBA Board decided to increase the cash rate target by 25 basis points to 3.10 per cent. The continued mantra is that inflation in Australia is too high (6.9 per cent over the year to October.) Global factors explain much of this high inflation, but central banks cannot address the cause, only the symptom. Monetary policy cannot ease supply chain pressure nor can it make grain grow more abundantly. The current hiking policy only has the aim of reducing the ability of individuals and businesses to pay the higher prices being charged by reducing their free cash flow.

The RBA and almost every other Bank’s central forecast is for CPI inflation to decline over the next couple of years. The dual message of rate increases and lower price pressure ahead is conveying the message that workers need not make excessive wage claims now (despite the tightness of the labour market). US officials are also very optimistic about the prospects of the economy having a soft-landing meaning there will not be a devastating pullback and workers will be able to catch up on their wage claims due to better times ahead.

Bond markets do not seem to believe much of this rhetoric. Yield curve shapes around the world are not showing a consistent pattern and although some of this is due to the unprecedented circumstances markets are dealing with, much of it also appears to be traditional and textbook pricing of what is essentially an unprecedented series of events.

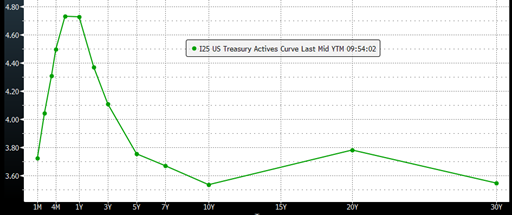

Figure 1:US Yield Curve

Source: Bloomberg

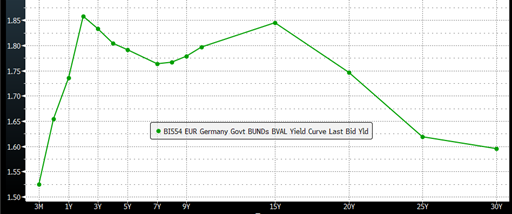

Figure 2: German Bund Yield Curve

Source: Bloomberg

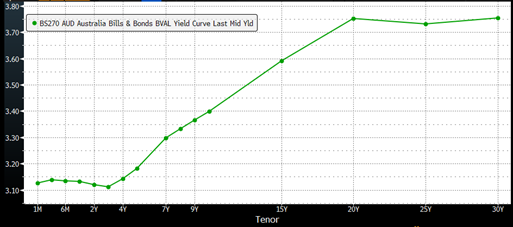

Figure 3: Australia Yield Curve

Source: Bloomberg

The RBA contends not only that the Australian economy is continuing to grow solidly, but the market has taken the view their strategy will be much more effective than that in either the US or Europe. For those economies the slower transmission mechanism of rate hikes (because Australian borrowers are largely paying floating rates) leads to higher peak rates and a need to quickly unwind them as the economy is pushed into contraction. The 20 year rates in both Australia and the US are around 3.8%, but the path to get there varies massively.

Economic growth globally is expected to moderate over the year ahead as economies slow, but the supply side issues in energy and the hope of a bounce-back in real wage growth means monetary policy has to remain “restrictive”. This blunt instrument is actually exacerbating the cost pressures on corporates who are always borrowers which is why the primary outcome of the policy is for companies to be forced to reduce their workforce and the “hope” from the fed is a rise of about 1% in the unemployment rate.

Bond markets domestically believe that growth will continue, and rates will remain above 3% for the foreseeable future. They believe that the RBA is appropriately juggling its dual mandate of inflation in 2-3% band and as close to full employment as possible. In Europe the President of the ECB Christine Lagarde has made it clear that a recession is the price to pay for inflation getting back under control. The bond markets reflect that view and the starting point is that the EU was already very fragile (starting this cycle from negative rates).

US bond markets on the other hand are not at all convinced that the Fed will be able to micromanage the economy into a soft landing. The central bank has emphasised they see a likely high point of Fed Funds at over 5% and a soft landing but markets expect the cash rate to move back towards 3% quite rapidly from this time next year as the economy withers.

What is clear is that the response from these three central banks has been very similar but the end point of this cycle and the impact on growth is seen to be very different. Australia remains the outlier, the market priced for lower yield peaks than the US or our close neighbour New Zealand and higher growth from 2024 than the market is expecting in either Europe or the US.

Not quite an economic nirvana, but the market is expressing a massive turnaround in trust in the RBA. Apologising for suggestions from the Governor that rates were unlikely to rise until 2024 has coincided with a robust endorsement of their most recent forward looking views.