SaaS (Software as a Service) businesses are one of the fastest growing segments within the IT industry, and have been one of the largest beneficiaries from the COVID-19 pandemic given the growing importance of flexible, affordable and cloud based technological solutions.

For many organisations, the implementation of SaaS solutions has been a matter of necessity, driven by our increasingly digital existence, covering areas like;

- Data storage (Microsoft Azure, Google Cloud),

- Customer Relationship Management (Salesforce),

- Communication (Zoom, Slack),

- Document management (DocuSign) and

- Customer service management (Zendesk).

Such is their importance to businesses, that many have touted SaaS revenue streams to be more valuable than first-lien debt, where its predictable, recurring, stable revenue streams provide a payment stream similar to that of a coupon.

“Software contracts are better than first-lien debt. You realize a company will not pay the interest payment on their first lien until after they pay their software maintenance or subscription fee. We get paid our money first. Who has the better credit? He can’t run his business without our software.”

- Robert Smith, CEO and Founder of Vista Equity Partners

This hypothesis, predicated on the belief that SaaS solutions are essential to the functioning of many businesses around the world, was put to the test during the COVID-19 pandemic.

Many businesses were forced to layoff significant portions of their workforce, halt all discretionary spending and do whatever was necessary to reduce their cost bases.

However, throughout all this, SaaS revenues held up admirably, confirming that they hold priority even over first-lien debt and highlighting the integral nature of many SaaS solutions to the day-to-day operations of many businesses around the world.

It is this intrinsic strength that justifies the lofty multiples on which they trade – if a once in a generation pandemic is unable to disrupt their revenue streams, then what can?

Therefore, as the topic of today’s note, we will cover SaaS businesses – why they are set to continue growing over the coming years, and the most influential players within each corner of the industry.

Why SaaS?

SaaS business models are far superior to legacy models – where in the past, software was sold on a license basis (incurring a large upfront fee) and had to be installed physically on computers by IT teams.

This made software inefficient at large scales – and encouraged the usage of a limited number of applications, often fitting square pegs through round holes as a result of the high cost of expanding available software.

However, with SaaS and its subscription-based modelling, and its typical location in the cloud, software has become cheaper for companies to both install and use, as well as significantly enhancing efficiencies through broadening the scope of potential software applications within a company.

The enhancement of efficiencies is primarily expressed through the ability to automate work flows through a greater integration of SaaS applications – easily justifying the additional subscription fees which companies may have to pay.

Going forward, it is likely that we continue to see many companies expand the SaaS applications they utilise, and subsequently provide greater recurring revenue streams to the industry.

Large Multiples and Poor Performance

SaaS companies have endured a tough couple of months – a product of their high valuation multiples, and their subsequent exposure to the tightening of monetary policy in the US.

Chart 1: 2-year performance of various SaaS stocks (as at 8-Feb-22)

Source: Bloomberg

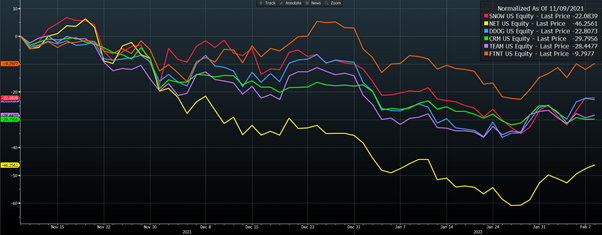

Chart 2: 3-month normalised performance of various SaaS stocks (as at 8-Feb-22)

Source: Bloomberg

As previously mentioned, their high multiples are justified by the strength of their recurring revenue streams, and the wide runway for potential growth available in the future.

Whilst they have been performing poorly, their fundamentals have remained strong.

Over the last few weeks, 3 of the largest cloud players reported impressive earnings – being AWS within Amazon, Azure within Microsoft and Google Cloud within Google.

- AWS: USD$71bn run rate, growth of 40% YoY (accelerating from 39%)

- Azure: USD$40-45bn run rate, growth of 46% YoY (decelerating from 48%)

- Google Cloud: USD$22bn run rate, growth of 44% YoY (decelerating from 45%)

All three players serve as accurate barometers for market performance and highlight how recent performance is purely a result of multiple compression.

So, if recent performance has been a result of exogenous factors (Fed tightening), and fundamentals remain strong – does this offer a unique buying opportunity for SaaS stocks in the short-medium term?

Unfortunately for SaaS investors, it is likely that returns will continue to be driven by policy, as opposed to fundamentals in the short-medium term.

This is the reality of having valuations driven by healthy multiples, and will likely see further volatility until a point where there is more certainty about rate hike and quantitative tightening timelines.

However, SaaS companies still offer attractive investment propositions over longer term investment horizons, where fundamentals will play a much larger role in determining the performance of the security.

Atlassian (NASDAQ: TEAM) – The Master of Work-From-Home (WFH)

Atlassian has served as one of the pioneers in the development of the WFH revolution – both from the perspective of software provider, and as an employer.

In August of 2020, they announced that their workforce could WFH in perpetuity, and that they were only required in the office 4 times per year – a testament to their focus on developing collaborative technological solutions which support remote working.

Within their product suite, they have Jira (issue & project tracking software), Confluence (document/data collaboration) and Trello (visual work management tool) – which are all focused on developing greater collaboration, and more effective communication amongst business units.

From its 29 October high, TEAM has fallen 34.17% (as of close on 8/2/22), primarily due to the premium applied to its multiple – trading at around 26x EV/NTM Revenue.

Chart 3: 5-yr chart of TEAM (as at 8-Feb-22)

Source: Bloomberg

This premium is well earned, being a leader within the “DevOps Cloud” software realm – and possessing one of the most attractive exposures to cloud adoption/remote work thematic within the enterprise software space.

Salesforce (NYSE: CRM) – World Leading CRM Software

Salesforce is the world’s largest customer relationship management (CRM) platform, enabling businesses around the world to automate its databases and client communications, as well as to manage customer satisfaction, and communicate internally.

Within the last few years, Salesforce has been aggressively conducting strategic acquisitions, in an effort to build out its Customer 360 tool.

These acquisitions have included;

- integration platform, Mulesoft in 2018;

- data visualisation platform, Tableau in 2019;

- and messaging platform, Slack in 2020.

The objective of Customer 360 is to better integrate sales, service, marketing and commerce channels, through combining data and creating more effective communication internally through the integration of Slack.

From its 9 November high, CRM has fallen 30.26% (as of close on 8/2/22), with worse than expected quarterly earnings in December driving valuations lower.

Chart 4: 5-yr chart of CRM (as at 8-Feb-22)

Source: Bloomberg

Going forward, its relatively low multiples reflect a more pessimistic perspective on its future growth potential, trading only at around 7x EV/NTM revenue. This is a product of Salesforce’s long history as a leader in the CRM space, and the lack of growth opportunities available relative to some other newer SaaS companies.

Down But Not Out

Whilst SaaS stocks have been on the bad end of recent market sell-offs – it hasn’t been a product of worsening fundamentals.

If anything – the picture looks more favourable, where SaaS stocks have already demonstrated that adverse economic conditions will not hamper their recurring, stable revenue streams.

It must be noted that the two stocks highlighted in this note only reflect some of the leading “pure play” investment options in this space, where Google, Microsoft and Amazon are all major players, but do not serve as appropriate pure play exposures.

In the short-medium term, central bank policy will continue to dictate their valuations, however for long term investors, opportunities may arise in accessing this innovative and fast-growing industry.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.