What is QT?

Most investors have an adequate grasp of monetary policy and the implications for their portfolio, where monetary policy that is expansionary or contractionary will likely have a resulting influence on the price of money.

Not just the present value of money but also the future value of money (the yield curve).

Most of this understanding is around the movement of the Overnight Cash Rate (OCR) or the manipulation of the size of the money supply, where the key focus for most of our lives has been the absolute level of the cash rate, which currently stands at 0.10%.

Central bank asset purchases have been a policy mechanism for a long time as well, multiple decades in fact, but usually short term in nature.

In Australia, we call them Open Market Operations (OMO) where the RBA would buy/sell government bonds to expand/contract the amount of bank reserves on issue, which in turn would see a change in the money supply.

This was primarily a short-term policy tool, which is why quantitative easing (QE) as it’s now known today was initially called Large-Scale Asset Purchases (LSAP), to make it obvious this was a longer-term and larger value policy tool and different from shorter term OMOs of generally smaller amounts of money.

QE has also been around for >20 years, where the Bank of Japan has been using it since the turn of the new millennium.

The Fed started QE in 2008 as a response to the GFC and again with gusto in March 2020 in response to the pandemic, as did the RBA for the first time, their first iteration of LSAP which has seen their balance sheet balloon.

Primarily, QE is a form of expansionary monetary policy that doesn’t move the cash rate, rather, it targets longer-term bonds by buying them, pushing down bond yields and providing liquidity to financial markets which allows them to settle during times of unrest – i.e. market participants can use the cash they receive from selling bonds to the RBA to facilitate fund redemptions or maintain corporate or household spending, rather than selling financial assets such as equities or property.

For example, the Fed’s QE renewal in March 2020 had an obvious effect on equity markets directly and indirectly, where the rate of expansion of their reserve base (the “impulse”) tightly aligned with the rise of the S&P 500.

Chart 1: Fed Balance Sheet (green) vs S&P 500 Index (red)

Source: Bloomberg, as at 7/Feb/2022

QE performed this function well, but now that financial markets no longer require such emergency policy levels, QE can look to be reversed.

Quantitative Tightening

At last week’s RBA policy meeting, the first of the calendar year, the Bank stated that their quantitative easing (QE) program would end this week, and in their May policy meeting they would consider whether they would reinvest the proceeds of future bond maturities, the opposite of QE and called quantitative tightening (QT).

Quantitative tightening has two main aspects worth considering:

1/ Allow the balance sheet to slowly contract in size when holdings (mostly bonds) mature over time and the proceeds are not reinvested. This is in contrast to reinvesting the proceeds which would maintain the same size of the balance sheet.

2/ Actively sell assets on the balance sheet into the secondary market.

Noting that the RBA is by no means suggesting the second option, which would cause a much faster reduction in market liquidity and likely more market volatility and tighter monetary conditions.

Either way, the implications of QT should mean something to all of us, as it’s a contemporary form of monetary policy that affects the price of money.

Background on the RBA’s Balance Sheet

In the years prior to the start of the RBA’s QE program in March 2020, non-government bank deposits held at the RBA was circa 28.4bln AUD, fairly constant over a number of years, though ever so slightly increasing to account for a growing Australian population and system money supply needs.

Since March 2020, those deposits have expanded from 28.4bln to ~445bln AUD for two reasons:

- The RBA’s QE program

- Increased cash levels from households, corporates and fund managers

Chart 2: The Size of the RBA’s Balance Sheet

Source: Bloomberg, as at 7/Feb/2022

To attribute the change in deposit balance size, the RBA has transacted ~350bln AUD of bond purchases, where some of those original securities purchased have matured, they already reinvested the proceeds.

The other ~67bln AUD is the savings from these households/corps/fundies etc.

While obviously there’s significant “surplus” cash available from numerous walks of life to consume, invest or continue to be held as a store of financial wealth, the size of the balance sheet has grown to a material size relative to our economy, or >15% of our total annual economic output.

The Speed of QT

What will likely be a matter of focus for the RBA and for investors in Australia this year will be the rate of attrition of the RBA balance sheet, lest the withdrawal of bank reserves and resulting lower levels of liquidity upset financial markets.

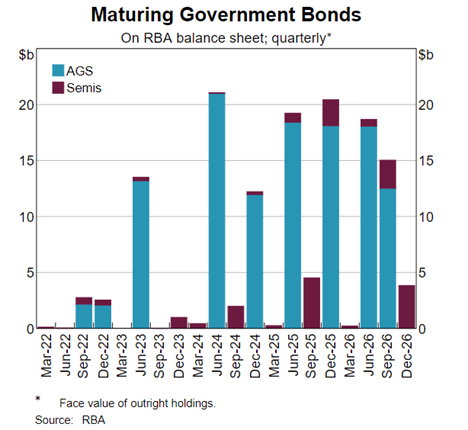

Speaking at a function last week, RBA Governor Philip Lowe provided insight that there are significant gaps in the RBA’s asset maturity profile, where “the large gaps in the maturity profile mean that we have more time to make a decision.”

Chart 3: Maturity Bond Holdings on the RBA’s Balance Sheet

This is noteworthy and distinct from other central bank balance sheets, where for example, the US Federal Reserve owns several hundred billion USD of US Treasury bills, short-term securities maturing within six months.

Otherwise, the Fed also targeted (generally) more short-term government bonds rather than longer-term bonds, making their maturity profile lumpier towards assets maturing in the next two years.

Whereas for the RBA, there are no significant maturities until September this year and the largest occurring when June 2023 and June 2024 government bonds mature.

Qualitative Easing/Tightening

While I hate to throw another jargon term at you, there is ANOTHER form of monetary policy called qualitative easing/tightening, that isn’t spoken about much.

Where quantitative easing was given its name for targeting a quantity of bank reserves to ease/contract policy, qualitative easing/tightening targets the quality of assets.

For example, a central bank buying more corporate bonds relative to government bonds would be conducting qualitative easing, as they’re targeting lower quality bonds (corporates) relative to generally less risky, higher quality bonds (government issued).

In fact, the Fed is currently enacting both qualitative and quantitative easing policy, where their 120 billion USD/month program was purchasing $90bln USD/month of government bonds and $30bln USD/month of Mortgage Backed Securities (MBS).

Bringing the theory to practice, in looking at conducting QT, the US Fed has signalled through various speeches and publications they’re happier to see their MBS holdings mature with cash proceeds not invested at a quicker rate than their government bond holdings.

Ergo, quantitative AND qualitative tightening.

More QT Likely Means Less Rate Hikes

QE became a viable policy tool because central banks had exacerbated their other tools by lowering their various cash rates near, close or even below zero%.

Hence, QE was a way of creating more expansionary policy than could be done with the cash rate alone.

Therefore, QT can also be a preferred method of withdrawing policy stimulus instead of hiking cash rates.

For example, sell side bank research has shown that every ~600billion USD of Federal Reserve balance sheet contraction could equate to a 0.25% cash rate hike.

If this is true and I imagine the Fed will do their own modelling, then this means that the Fed (and other central banks) will likely enact policy that’s a combination of both.

This will likely lead to lower cash rate forecasts combined with balance sheet attrition that in concert, provides a similar level of policy accommodation.

Why?

The global economy has far more debt today than we did pre-pandemic.

This has increased our sensitivity to changes in market interest rates (borrowing costs), where the same magnitude of a rate hike today has far more material an effect than pre-COVID.

Central banks know this and are not keen to shock financial markets by hiking too substantially when they may be able to alter financial conditions by the same degree through liquidity withdrawal, rather than rate hikes.

Forecasting the RBA

While the US Fed has already signalled they’ll look at QT as an option that will allow for a shallower rate hiking cycle, the RBA has only mentioned the prospects of QT in the past week, new news to digest for the market.

It’s our view that it’s very likely the RBA does look to pursue QT this year and in following years, especially if other central banks have already begun to do so, making the news less unsettling to AUD investors.

Given the sparsity of their maturity profile, the market won’t have too many jitters to this approach and any short-term ructions can be likely ameliorated by short-term OMOs to provide short-term liquidity.

However, the RBA will likely maintain their current modus operandi in emphasising their need to stay nimble and flexible in any policy action, where their trajectory is couched in uncertainty, dependent on economic data and thus can vary as the economic landscape evolves.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.