If you missed last week’s missive, I’d encourage you to take a look, as today I continue from where we left off last week.

The original topic was to deconstruct modern portfolio theory, in order to build portfolios that meet requirements, with assets that are truly diversified to achieve investor or client goals.

Diversifying gains to reduce losses

We want to diversify gains to reduce the chance of losses, as no one cares about losses if they are diversified.

The whole point of diversification in Modern Portfolio Theory is to decorrelate the portfolio positions so that there’s balances between risk premia, and that it all isn’t from one similar source.

For example, a portfolio that has 50% domestic equities and then 50% domestic hybrid securities (as a proxy for fixed income) would not have been diversified this year, as the hybrids had a large correlation with equities and sold-off just as the underlying equity did.

Another example, WBC ordinary equity (red line) dropped 45.13% in Q1 2020, whereas WBCPF’s price (green line) declined 7.84%

This is an example of a correlation where both prices moved in the same direction because of the same catalytic events.

A diversified relationship would’ve seen the opposite occur.

Source: Bloomberg

To epitomise the opposite example, I compare the ASX 200 (green) versus the Bloomberg Ausbond Government bond index (yellow).

The ASX 200 dropped 35.85%, whereas the government bond index stayed steady and continued to pay income (bond coupons) throughout the year.

Source: Bloomberg

In comparison:

- A portfolio that was 50% hybrids, 50% ASX 200: -22% in H1 2020

- A portfolio that was 50% government bonds, 50% ASX 200: -14% in H1 2020

Different types of assets

As money managers, we need to be more aware of the different types of assets available for investment, so that our asset allocation universe is broad, so that it can then be defined and refined to meet investor objectives and goals.

This comes in two forms:

- Different asset classes that have different expected returns and different correlations

- Different vehicles (funds, SMAs, direct securities) that have differing styles of management

A large task.

Different asset classes

To gauge some of the different asset classes, a prime example is to look at the investment holdings of our Future Fund – the Australian sovereign wealth fund setup in 2006 by then Treasurer Peter Costello to “strengthen the Commonwealth’s long-term financial position,” which runs over 148bln AUD as at December 2019.

Future Fund provides a wealth of information for their different allocations, which you can view here.

Future Fund invests in:

Public Equities

- Australian equities

- Developed market equities

- Emerging market equities

Private Equity

- Leveraged buyouts

- Venture capital and growth

- Special opportunities

Property

- Unlisted

- Listed

Infrastructure and Timberland

- Unlisted

- Listed

Debt/Fixed Income

- High grade debt

- High yield debt (sub-investment grade debt)

- Distressed debt

- Event driven debt

Alternatives

- Multi-strategy hedge funds and relative value

- Macro-directional

- Alternative risk premia

- Global alpha

Currency

- Currency overlays to make gains/losses based on currency movements

Money Markets

- Cash and cash equivalents

This is quite the comprehensive list of asset classes and may include block-chain currency such as Bitcoin or Ethereum in the future too, which is a slowly emerging asset class.

Different investment styles

This is the most time-consuming part of an investment process, as once we determine our risk tolerance, and then what asset classes we want to combine, we must choose managers that articulate the investment thesis.

I.e. passive vs active management, large cap vs small cap equities, credit vs government bonds, value vs growth equities, momentum vs mean reversion, currency hedged versus unhedged etc.

For this, Morningstar, Mercer, Lonsec, etc. have available resources to help categorise investment managers, and we provide a full list of available fund managers active on our Mason Stevens Investment Service platform here: masonstevens.com.au/resource-hub

Capital market assumptions

At this point we know what asset classes are available and what fund managers can be utilised to espouse our investment thesis. Finally, we need to overlay our capital market (return) assumptions to pick.

Institutional fund managers typically make their capital market assumptions (CMA) available online as a free resource.

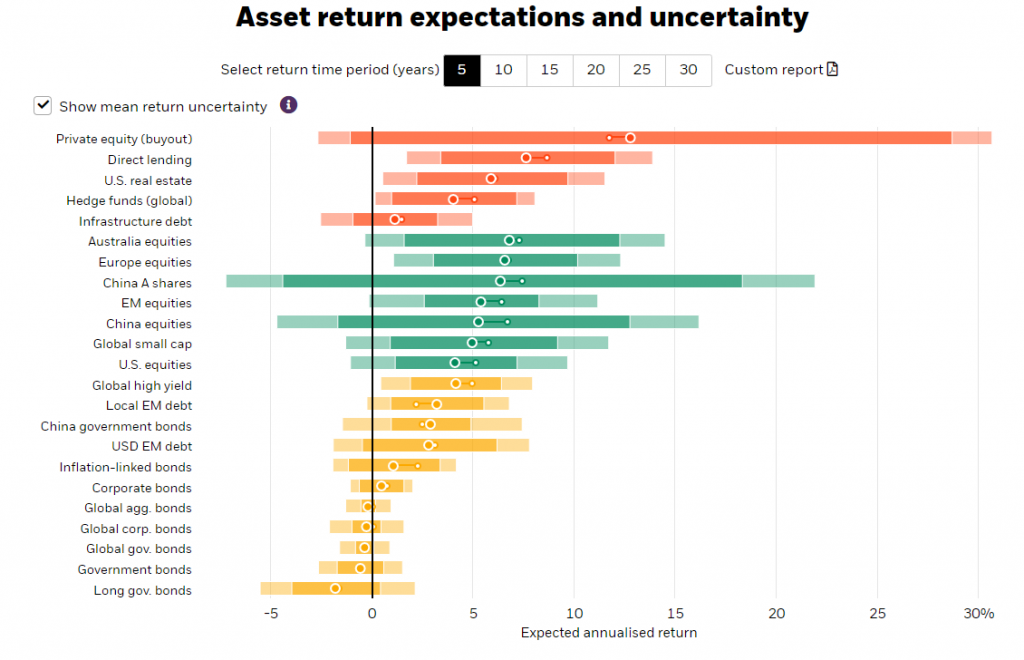

For example, Blackrock has a great visual tool for their asset class universe:

Source: Blackrock

It becomes quite obvious that private equity, private debt (direct lending), US real estate, Australian equities, Chinese equities and European equities stand out from a return perspective – but I note the width of the expected return highlights the variability in the result, with a higher expected error in forecasting.

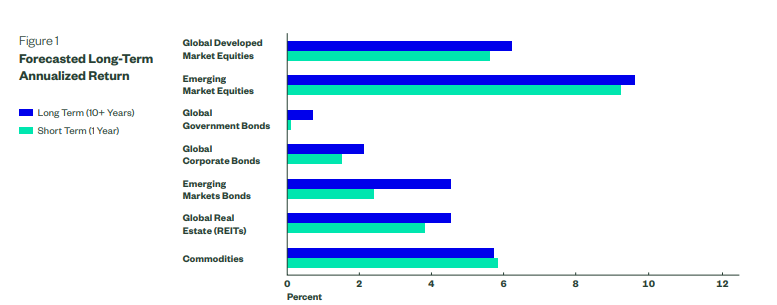

Another example, State Street Global Advisors has a less visual tool, but an equally large universe of expected returns.

Source: State Street Global Advisors (SSGA)

Looking at State Street’s CMAs, we’d be more favourable on developed market equities, emerging market equities, commodities and global real estate.

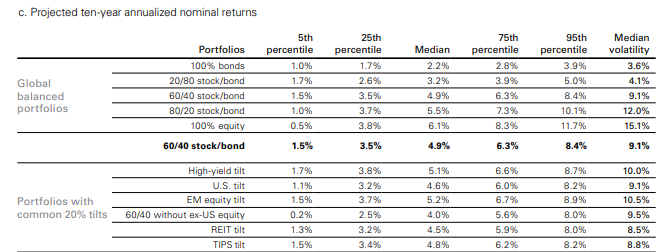

As my third and last example, Vanguard make their full-year outlook available along with CMAs for public viewing.

Their simulated returns are tabled as follows:

Source: Vanguard

Vanguard’s assumptions would indicate that balanced portfolios with a high-yield bond tilt, or emerging market equity tilt would have a better probability of higher returns than those more concentrated on inflation linked securities or REITS.

Building an awesome portfolio

When we combine our assumptions about expected returns, take steps to mitigate correlation by diversifying across a range of asset classes and investment styles, we produce what has always been the goal of Modern Portfolio Theory – portfolios that maximise risk-adjusted returns and that align to investors’ objectives.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.