I can’t help but notice the similarities between today’s market environment and markets back in 1999.

As Mark Twain once observed:

“History does not repeat, but it rhymes.”

Back then, Value investing and Value managers were seeing outflows after having underperformed Growth managers for years.

The spread between valuations of US and Emerging Market equities were wide with the US witnessing speculative behaviour in stock markets (“dot com bubble”) from retail investors with a lot of investors waiting for mean-reversion to occur and underperforming in the meantime, as value stock’s performance was lacklustre to the phenomenal returns from growth and tech stocks.

I recently saw an entertaining snippet from a client redeeming from fund manager GMO back in 1999, who cited similar reasons for their withdrawal to what GMO is now seeing again, 21 years later.

Source: GMO Research Library

You can see the similar market situation today, and its reason enough to re-think risk management and portfolio allocation.

The 60/40 Portfolio

In 1952, the Journal of Finance published a paper written by Dr. Harry Markowitz titled “Portfolio Selection.” He wrote it while still in graduate school and introduced the concepts known today as “Modern Portfolio Theory” (MPT), for which he later received a Nobel Prize in economics for his work.

MPT addressed asset class risk by blending stocks and bonds to achieve a more-optimal portfolio with less risk than the individual components, something we now call diversification.

After some time, academic studies were published showing that a “balanced” portfolio which exhibited the correct mix of risk and return was composed of 60% stocks and 40% bonds.

This became known as a 60/40 portfolio.

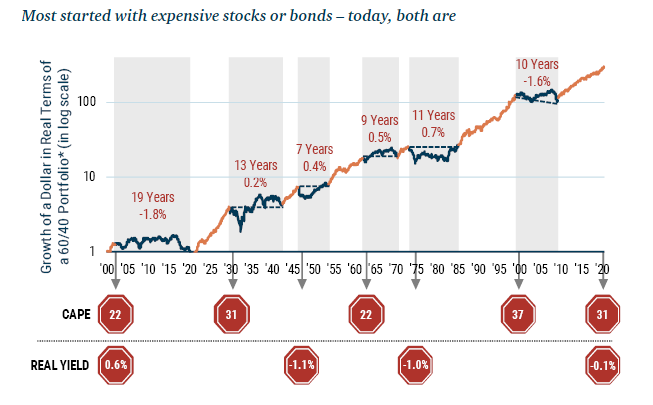

Lost Decades

As mentioned above, the realities of modern financial markets and their correlations to one another make us re-think the conventional 60/40 portfolio mix, just like investors needed to in 1975 or 1999.

In both these times, 60/40 portfolios returned 0% or less over a 10-year period.

This is worth re-stating. Investors who simply executed a buy-and-hold strategy over certain periods saw negative returns or near zero% returns for an entire decade, and we’re in a similar situation based on current bond spreads and equity valuations.

There are six different “Lost Decade” periods in the last 120 years where this occurred.

Yes, for nearly 60 of the last 120 years, balanced portfolios produced zero returns.

Source: GMO Research Library

During a lost decade, investors realise that they need to be more strategic and tactical in their asset allocation, but also that they need to be nimbler with their funds, rather than employ the long-term “set and forget,” buy-and-hold strategy.

Risk AND Return

We used to combine stocks and bonds to varying ratios to find an efficient frontier between risk and return.

What we were measuring, and building was portfolios with high Sharpe ratios; portfolios that had favourable relationships between risk and reward.

A portfolio with a higher Sharpe ratio uses risk more efficiently, as they produce returns but with less volatility than a portfolio with a lower Sharpe ratio.

More positively, this may be the ideal time to re-think current portfolio holdings and look at more unconventional approaches.

Unconventional Asset Allocation

This has led an increasing number of investors to introduce other asset classes into portfolios, rather than just stocks and bonds.

This includes domestic and international equities, domestic and international FI, precious metals, real estate and infrastructure.

However, this has also seen funds flow to “alternative” investments such as credit, hedge funds, emerging markets and private equity.

The Idea Behind Diversifying – The impact of losses

Something that is not fully understood from Markowitz’ original work on Modern Portfolio Theory was that the concepts were not meant to be confined to stock and bond portfolios only, but that Modern Portfolio Theory should be an ever-present mindset and that portfolio managers should remain vigilant to uncompensated risks from inherent correlations between similar investments.

Markowitz was prescient and wrote the following first paragraph, emphasis mine:

The process of selecting a portfolio may be divided into two stages. The first stage starts with observation and experience and ends with beliefs about the future performances of available securities. The second stage starts with the relevant beliefs about future performances and ends with the choice of portfolio. This paper is concerned with the second stage.

People read they needed to diversify stock portfolios with fixed income for the volatility smoothing affects but missed the overarching message that portfolio managers need to manage risk to achieve forecasted return.

Perhaps Markowitz’ first paragraph should’ve said “Do not use MPT without relevant beliefs of future performance.”

I’m belabouring this point because

#1 investors often don’t have expected returns front of mind for markets; and

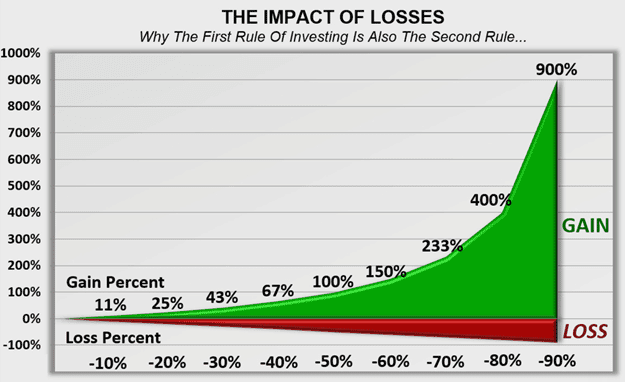

#2 each incremental loss requires a slightly larger gain to return to breakeven.

For example, a 40% loss would require a subsequent 67% rebound/gain to breakeven.

Likewise, a 50% loss a 100% rebound, or an 80% loss a 400% rebound.

Therefore, we must remember that we need to build genuinely diversified portfolios, then review them periodically as their past performance and diversification may not be suitable as financial markets evolve.

Source: Crestmont Research

How should we then invest?

Let’s sum up everything we’ve spoken about today and recently.

We’re entering a period of moderation with potentially lower returns in equities based on existing developed market valuations, but also of limited capital upside for bonds as interest rates are near the zero-lower bound (zero%).

I believe that diversifying among asset classes without proper forecast performance expectations is simply diversifying losses, rather than avoiding losses.

The answer is investors need to be truly diversified, but also need to be tactical in asset allocation.

Said otherwise, we need to invest in non-correlated assets or trading strategies with investment managers that have the mandates to achieve investors’ goals.

Next week I’ll discuss the different types of investments that may constitute a truly diversified multi-asset portfolio.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.