As most of us have grappled with lockdown, one thing has become readily apparent.

Our lives are becoming increasingly digitised, defining the ways we work, entertain ourselves, and most importantly – the way we shop.

Even for the most digitally inept of us, the amount of time we have spent online has gone up.

This has enforced lifestyle changes which will likely be irreversible, where in the past, onboarding into the more efficient digital world was hamstrung only by societal norms.

This is a trend we’ve seen most prevalently within the work-from-home (WFH) space, where many employees and employers have been forcedly exposed to the efficiencies and increased employee satisfaction gained from working from home – a topic which we have covered recently.

However, there is one lesser mentioned beneficiary of COVID-19 which has capitalised upon the increased digitisation of our lives – online advertising.

Long gone are the days where companies are forced to pay a premium primarily advertising to consumers unsuited to their product, through mass means such as billboards or newspapers.

With online advertising, the value proposition is simple – create more targeted advertising content, which reaches more of your target market, for a fraction of the cost.

In today’s note, we will go through online advertising – why it’s effective, who are the big players, and why it’s set to stay post COVID-19.

The Value Proposition is Clear

The value proposition for online advertising is simple.

Deploy campaigns targeted at specific demographics/groups, with greater flexibility and a data driven approach.

Given the extensive levels of data collected on consumers and their individual characteristics, companies have been able to cut costs through advertising only to those parties within the target market.

For example, if a company were to attempt to market their product to males interested in outdoor recreation between the ages of 30-40, you would be able to distribute content to those individuals through targeted advertising campaigns to online users whose personal data placed them in that demographic .

Previously, this level of targeting could only be achieved through advertising on a TV show/magazine/newspaper which most suits that demographic, but would also involve distribution to other groups of people within those mediums.

Moreover, with the ebb and flow of varying stages of economic reopening, the needs and wants of consumers has changed dramatically over the course of the past year and a half.

Through employing digital market campaigns, companies have been able to alter the content they distribute or change the geographic dispersion of this content with the click of a button.

With enhanced flexibility offered by digital marketing, companies have been able to reduce/increase their spend in specific regions – a useful tool given the bifurcated stages of economic recovery both within and between countries.

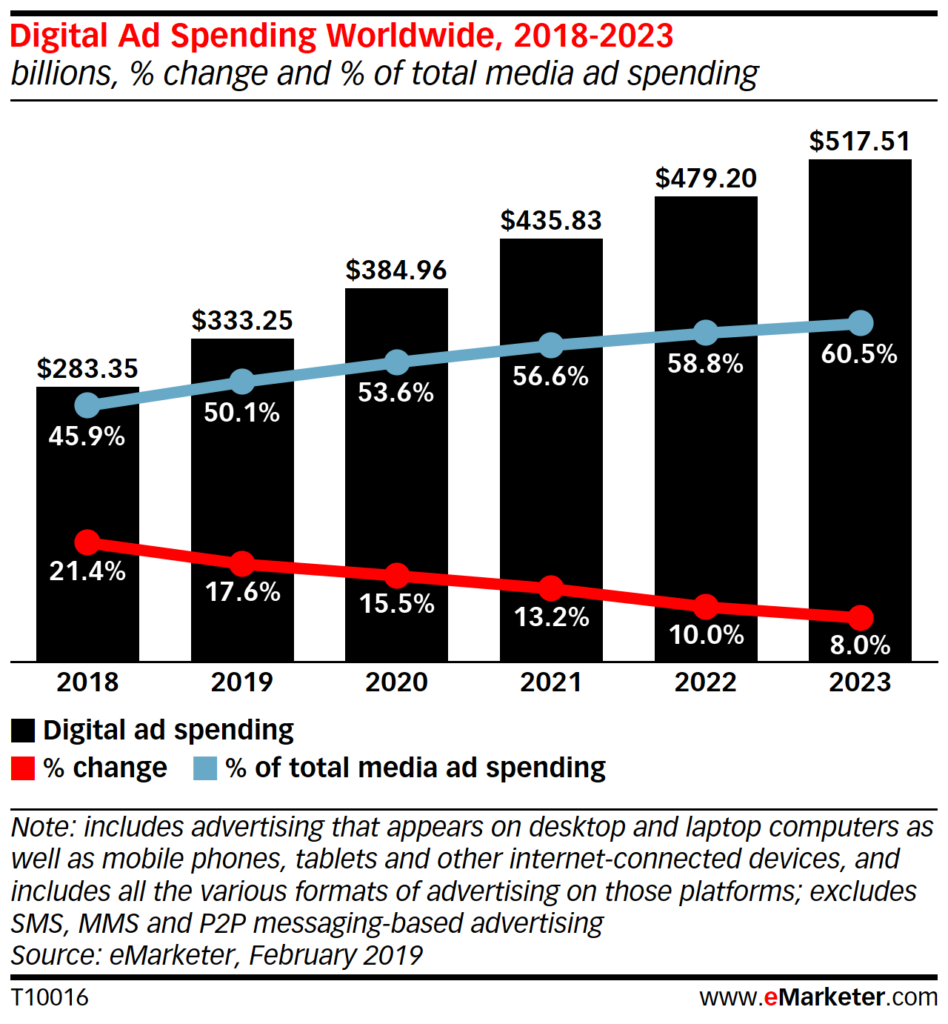

The online adveritising take up has primarily been within the US, which leads the world in ad spend and has some of the largest online adveritising companies, with an industry CAGR of 11.9% forecasted through to 2025 (Statista 2021).

Source: emarketer

Digital marketing has also become more suited to the ways in which we consume, with the U.S Census Bureau finding that Americans spent USD$791.7 billion during 2020 using e-commerce, up 32.4% in 2019.

Whilst these numbers may fall slightly in 2021 with the removal of lockdowns, it is likely that the retail industry has changed forever, and that habits have been permanently engrained into consumers.

Who Are the Big Players?

The rise of social media and internet-based entertainment has seen a dramatic shift in the way in which we consume content.

These mediums have increased our time spent online and allowed greater autonomy over what content we view.

No longer are we constrained to watching whatever is provided on TV – if you want, you can watch people eat food (yes there is a market for this), as opposed to watching Gordon Ramsay cook food.

As a result of these developments, the dissemination of digital marketing has led a transition of power from content producers (TV shows, movies and newspapers), towards content platforms (social media and YouTube).

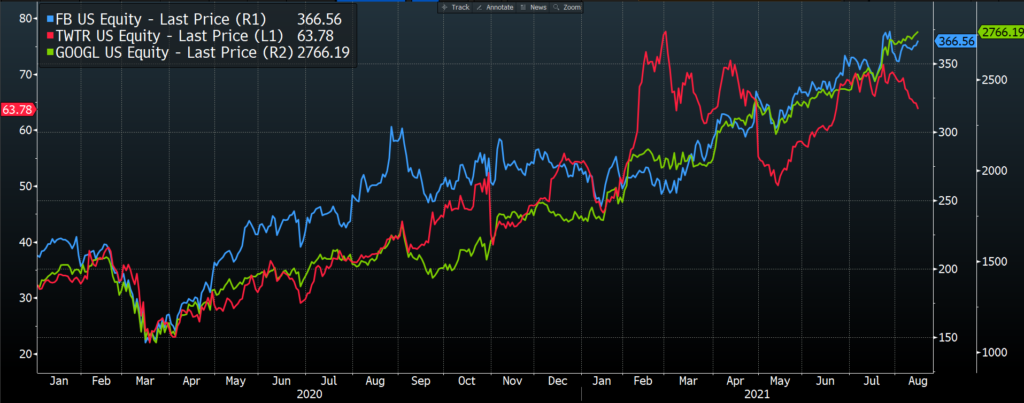

These platforms now serve as the biggest players within the place, with companies such as Alphabet (NASDAQ: GOOGL), Facebook (NASDAQ: FB) and Twitter (NYSE: TWTR) leading the pack.

Source: Bloomberg

There are multiple mediums which companies can choose to utilise across these platforms, including images, videos, augmented reality (AR), and animated stories – allowing a much more tailored solution.

Moreover, through the greater collection of user data, these platforms have been able to enable greater performance analytics, with the unique Cost Per Click (CPC) model continuing to grow in prominence.

Google stands as one of the largest players in the advertising space, deriving approximately 81% of its revenues from advertising related streams in Q1 2021 – including AdSense, YouTube and other advertisements on related websites.

Facebook and Twitter offer a more targeted medium, both being blessed with a wide variety of personal information which is made available to them through their respective social networks.

Whilst one may be able to restrict certain pieces of personal information provided to search engines like Google, a greater level of information disclosure is required to utilise social media networks to their fullest extent, enabling more accurate and effective campaigns through collection of personal information, engagement in groups and what topics you may post/comment about.

Will We Go Back in Time?

As with many of the trends which COVID-19 has accelerated, it is almost certain that we will not revert to our old ways.

Since the onset of the COVID-19 pandemic, online advertising adoption, and innovations within the space have been pushed forward by a number of years, making marketing campaigns more effective and cost efficient.

Luckily for investors, exposure to the space is relatively concentrated within mega-caps such as Google, Facebook, and to an extent Twitter.

As online advertising continues to grow its reach, the main question which will define the success of incumbents will be the ability to retain and grow user bases, and the extent to which they can be monetised.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.