The last two to three weeks have been overshadowed by geopolitical uncertainty within the Russia-Ukraine unrest, the spectre of higher bond yields (borrowing costs) and reduced financial market liquidity.

Most of the hiking cycle appears already priced in, where flattening of global sovereign bond yield curves suggests that the current central bank hiking cycle will not be particularly long or deep.

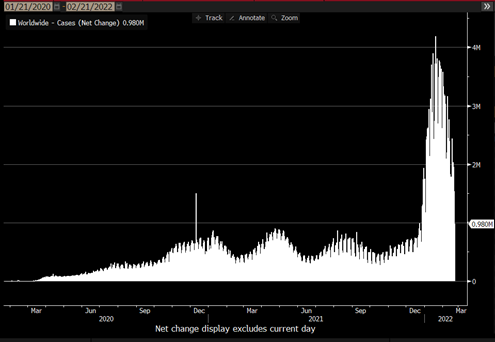

The nuance to this is that central banks remain cautious in their outlooks despite stronger and more sustained inflationary pressure, given the geopolitical backdrop but also given the lingering effects of the pandemic and the likelihood of a new COVID variant emerging with an unknown impact on health, mobility, economies, and commerce.

Chart 1: Daily COVID-19 Case Numbers

Source: Bloomberg, as at 21/Feb/2022

This has put central banks in precarious positions, where they’re trying to balance their mandated tasks of maximising employment (and the possible unknown impact of a new COVID variant) along with price stability (inflation).

In this regard the RBA has a slightly different agenda as the RBA Act (1959) does not include price stability as a goal, rather, states to target currency stability – the value of our AUD’s purchasing power.

Either way, we remain objectively positive in our outlook for CY2022, where so far economic growth prospects remain positive as are corporate earnings, though less so than last year.

In terms of equity markets, earnings remain quite strong, margins well defended, corporate balance sheets cashed up, where we can see a re-emergence of fundamentals playing a larger role in macro-decision making, as opposed to the POLICY meme of the past two years that trumped all other factors.

POLICY!

Central banks across the world have turned more hawkish, either forecasting interest rate hikes or enacting them, and also looking to unwind (to varying degrees) the substantial balance sheet accretion of 2020-2021 that provided abundant liquidity to financial markets through open market operations.

The encouraging news is that short-term interest rate (STIR) markets have already discounted substantial tightening in the coming 12 to 18 months, without materially damaging risk asset prices.

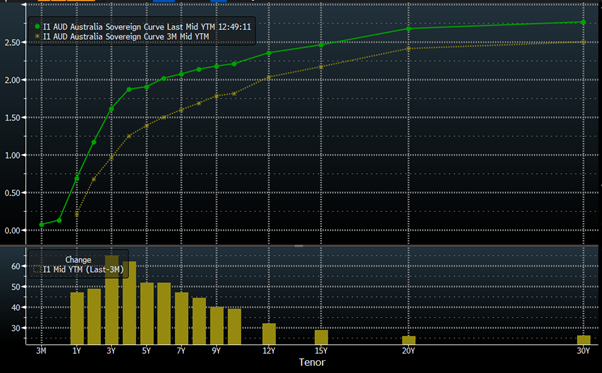

Chart 2: Australian Sovereign Yield Curve, current (green) versus 90 days ago (yellow)

Source: Bloomberg, as at 21/Feb/2022

Moreover, the tightening forecast into STIR prices shows a short and sharp series of rate hikes, followed by very flat yield curves of little hikes thereafter.

It comes across that markets are not yet ready to price any or many interest rate hikes beyond CY2024 and suggests that the accommodative backdrop will remain in place for some time.

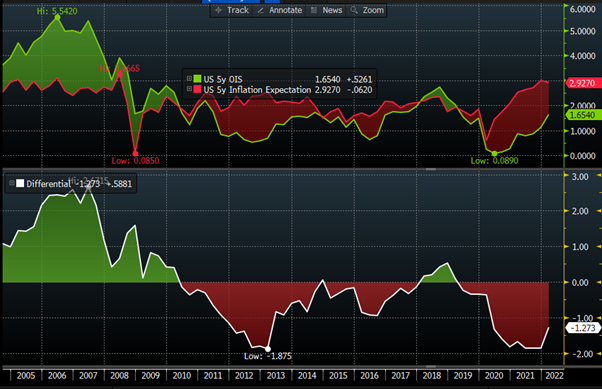

Chart 3: US 5y Cash Rate Expectations vs 5y Inflation Expectations, real interest rates priced at -1.2% p.a.

Source: Bloomberg, as at 21/Feb/2022

This creates an interesting situation, where at present, real interest rates are very accommodative to risk assets, but if central banks such as the US Federal Reserve are serious about returning policy to “neutral”, then we should (at some point) price in higher cash rates (more hikes) or lower inflation expectations.

In this type of environment in the short to medium term, stocks with better earnings prospects should continue to outperform, as they highlight their ability to weather bond market volatility and inflationary pressures of higher operational and funding costs.

Corporate Earnings

The current rising interest rate environment has had a large impact on equity markets in the past three months.

This was largely a sharp compression of equity multiples, where the forward P/E of MSCI World declined from 18x to 16.8x from the start of the year until now.

Chart 4: World Equity Index Performance over the past 90 days (2nd column from left), (last column is re-based in AUD)

Source: Bloomberg, as at 21/Feb/2022

On the microeconomic side, corporate fundamentals remain solid where balance sheets and forward earnings indicate companies can withstand modest increases in interest rates – such as what’s currently priced in.

Firstly, during the past two years companies slowed capex and opex and increased borrowing, building substantial cash buffers.

Secondly, companies have been able to take advantage of the abundance of liquidity in the past two years, allowing them to lengthen the duration of their borrowing profiles.

We saw this firsthand in Australia where companies that would typically issue 5-year bonds, issued 10–12-year bonds instead – such as Lendlease and Charter Hall.

And this would usually penalise corporates with higher borrowing costs locked in for longer periods, the historic low in interest rates meant that corporates saw a decrease in their borrowing cost despite the longer-term debt issuance!

Chart 5: Cost of Borrowing Has Decreased Across all Sectors

Furthermore, during this Q4 earnings season we have seen a majority of companies reporting solid earnings above analyst expectations, supported by strong top line growth and healthy margins.

While this was seen across the entire MSCI World Index, earnings upgrades were not uniform.

The majority of upgrades were concentrated in energy, IT, and consumer discretionary stocks, regionally focused on commodity-rich countries such as APAC (ex Japan) and Latin America.

Thinking about this for a minute, earnings guidance upgrades are seemingly cyclical (so far) given the commodity and energy related focus, where we wouldn’t want to misrepresent this localised rally as being a “value” rally, since most energy companies fell within the “value” factor category.

Instead, we could attribute this to a “business cycle” factor of cyclical nature, based on transitory demand for energy stocks, rather than simply a re-allocation towards lower P/E corporates.

Growth Over Value

Bringing the macro and the micro together, we remain in a world of scarce economic growth and unless the rate hike status quo changes, low interest rates, sub 4% corporate borrowing costs and negative real interest rates.

This environment tends to favour “growth” factor stocks as opposed to value, where we can foresee an extension of the “reach for yield” investment paradigm.

The market believes that an aggressive rate hiking cycle comes at the expense of future rate hikes, hence the flatter yield curve and pricing for terminal cash rates (such as the USA or Australia) in the 1.5-2.0% area.

For the yield curve to steepen, it would likely require large public or private capex to start, which is entirely possible given the strength of corporate balance sheets – though yet to be seen in corporate earnings guidance nor business activity statements.

As such, we’d suggest that “value” stocks are a tactical way to downsize risk-asset exposure in the short-term, rather than a longer-term strategic allocation.

Income Instead

Putting growth and value factors aside, we are becoming increasingly interested in dividend and income plays as a way to receive stable and reliable earning streams.

This characteristic is in vogue during such turbulent times, where the underlying fundamentals of dividend paying stocks has also improved.

Again, some Income-factor stocks also screen as value-factor stocks; and don’t want to connect the two concepts.

Chart 6: Dividend Per Share (blue) vs Free Cash Flow (orange) of MSCI World

Closing Remarks

Using current market pricing, the market has projected a short and sharp rate hiking cycle with little to follow.

This makes intuitive sense to us as even this year, our outlook is couched in uncertainty given the lingering presence of the pandemic, as the potential for geopolitical conflict to escalate into war.

This has created an environment that remains slightly pro-risk, where interest rates will likely remain near historical lows as they have since the GFC, an environment categorised by “reach for yield”.

We’ve seen the effects of the environment over the past 2-3 years within credit, public credit, growth equities, property, and private equity – even crypto.

As the amount of government and central bank policy support is withdrawn, we’re watching for a rotation from POLICY back to FUNDAMENTALS, and targeting quality of earnings, business margins, balance sheet strength & growth prospects as our ideal characteristics.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.