In the multitude of notes we’ve written about equities, most will make a basic assumption that we are ‘long’, i.e. we are buying the security or fund with the view that the market is going up.

But what if we want to capture segments of the market as they go down, in a bid to reduce volatility, or maintain returns even in a risk-off environment?

How does an investor augment their portfolio’s equity exposure to espouse a particular market view, one which may diverge from simply being 100% long?

Continuing on from Jesse’s introduction to risk-off investing, today we will examine one particular investment strategy that allows a continued exposure to the equity market whilst maintaining protection against (or exposure to) a risk-off environment: long/short equity.

There are several categories which encapsulate long/short, we will cover the two primary strategies with potential managed fund exposures in this note – for purposes of this overview we won’t place particular importance on domestic versus global exposure.

An Introduction to Long/Short

The long/short strategy is not a new one to financial markets.

Hedge funds employ some variation of both long and short positions within their investment management, or many readers may be familiar with the “130/30” style of fund which has been used in institutional investing for decades.

In long/short strategies, the fund manager will generally look to employ a form of stock borrowing (using correlated long and short paired positions of the same stock), or through the use of short-selling securities to fund/leverage greater long exposure.

Amongst managers there are several means to employ long/short positioning in equities [long/short strategies can be used in fixed income as well, but we will cover this in another note], from sector-wide long/short positions, geographic long/short or market-wide.

Due to the depth and breadth of available offerings for market-wide long/short funds in Australia, we will focus on these.

Market Neutral

Market neutral strategies are implemented to capture performance from both rising and falling equity markets – generally by hedging out one particular risk, such as broad market movements (i.e. volatility).

The most common form of market neutral funds are those which hold equal long and short positions (for example, 50% long, 50% short) to net out market exposure.

The idea behind this strategy is that you’re not sure which way the market will go, but are confident in generating alpha from stock selection.

So, your performance is largely unaffected by a rising or falling market, but is almost entirely a function of your stock selection – you want the stocks that the fund manager picks to diverge away from the market to generate a return in excess of general market movement (because that market movement is hedged away).

On yesterday’s Morning Markets Call we spoke to Sean Fenton of Sage Capital, who are an example of a market neutral manager with the Absolute Return Fund, with the performance of the fund being entirely generated by the manager’s stock selection process.

You can also think of this strategy of removing beta from your return entirely, to only generate alpha. This is sometimes also known as “absolute return”, rather than relative returns to the market.

Active Extension

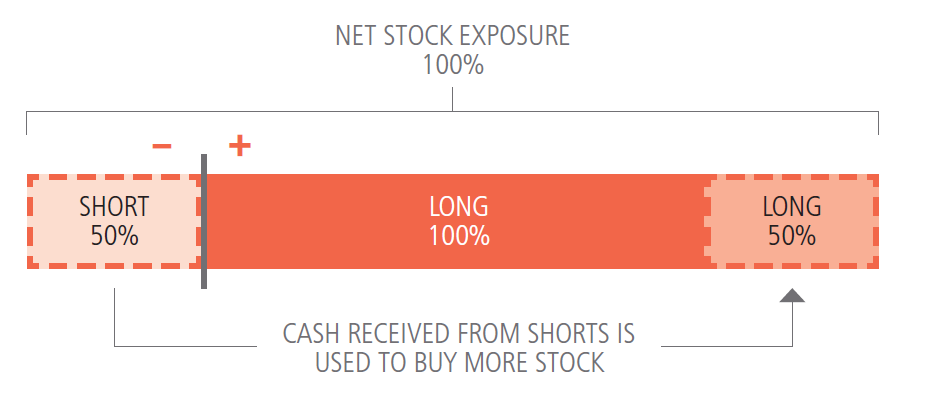

An active extension strategy is a strategy used to gain increased long exposure, by leveraging a short position allocation to free up capital in the portfolio.

For example, in the popular 130/30 style of active extension fund, the strategy can short up to 30% of the fund’s assets, which allows an additional 30% capital to be added to the long position. In effect, the fund uses 100% of its capital to go 130% long, leveraging its position into the market.

The below is a great illustration from Grant Samuels Funds Management on active extension:

Unlike market neutral, this is an inherently bullish strategy, where you are looking to maintain full equity market exposure but generate returns potentially above general market movements.

Although it is not the most direct way of going about it, active extension is a potential risk-off play if you believe that the market may increase but one particular sector will drop-off; to execute this strategy you need to be confident in the manager’s current positioning and ability to short the right areas within markets.

For active extension funds, on Friday we will be speaking to Mark Landau of L1 Capital around their Long Short Fund (LSF:ASX), which uses an active extension strategy with the aim of outperforming the broader equity index without sacrificing market exposure.

Long/Short Cheat Sheet

Let’s compress the above into a quick guide on the different utilisations an investor might see for long/short strategies – at a very general level.

| Strategy | Objective | Sentiment | Long Exposure | Short Exposure |

| Market Neutral | Preserve capital from general market movements, whilst generating returns from stock selection | Bearish/Neutral | 0 -150% | 0 – 150% |

| Active Extension | Generate returns in excess of general market movements whilst retaining full market exposure | Bullish | 50 – 150% | 0 – 50% |

To Make a Long Story Short

Long/short strategies offer a potential solution for investors who are anticipating a risk-off environment– either throughout the entire market, or just in specific sectors.

As an alternative exposure, they may complement existing core equity holdings within a portfolio, or act as a supplementary holding with diversification-based benefits.

Be it expressing a bearish, neutral or bullish point of view, long/short funds offer investment strategies unavailable to the vast majority of retail investors and can offer additional value relative to long only funds.

As long/short strategies carry greater reliance on manager skill, due diligence is key to ensuring fund selection is commensurate with risk profiles. There are a wide variety of long/short funds on the Mason Stevens platform, not limited to the two mentioned from our morning calls, and each has their own subtle approach to the overall strategy.

To make a long story short, long/short offers a way for investors to express various risk-off sentiments without needing to directly employ the use of derivatives – depending on your view on where markets are going and how you want to gain exposure to that move.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.