Like magpies and their nests, investors have traditionally looked to add ‘shiny things’ to their portfolio as the threat of inflation looms.

The relationship between precious metals and inflation has been shown empirically in the past, including gold and the ‘white metals’, being silver, platinum and palladium.

These are also “real assets”, physical pieces of ‘something’ which we believe to have some form of intrinsic value.

The logic behind the procyclical relationship between these metals and inflation is that their value is measured/derived in ways differing to that of fiat currency – whilst when prices rise the purchasing power of currencies decreases (as our primary form of exchange), precious metals should hypothetically hold their value as they are seen to be tangible and of a value not associated with simply buying everyday goods and services.

This relationship is often unstable and often influenced by short-term market dynamics than longer-term structural factors.

In fact, recent market conditions have made many ask the question if precious metals do still provide an effective inflation hedge – certainly there is more sentiment and speculation focussed on this asset class than the concept of buying corn or milk to benefit from rising prices.

But let’s not affirm or deny their inflation-hedging capabilities just yet – time to jump in and talk about our precious.

Gold (Au)

We will get the controversial metal out of the way first, gold.

Gold is one of the oldest forms of currency in human history, dating back to 550BC Lydia (now Turkey) – due to its relative scarcity and historical use as a base for jewellery, it has held a place in our society as a measure of physical value.

Today, gold is far less linked to any currency or medium of exchange.

As Mike touched on back in February, gold has not underpinned the USD since 1971, so the relationship it holds to the value of the USD (which we will here consider as the primary market for inflation) is driven almost entirely by market sentiment.

Gold has limited uses in industry, being a minor component in electronics, so its primary use is as a ‘store of value’ in time of perceived financial or political instability – today it meets steep competition from Bitcoin as a market darling for maintaining value in the face of “impending hyperinflation”.

More-so than any other metal in this list, gold is worth what people think it is worth.

Outside of having to move your family in a time of war, it’s unlikely that you’ll ever need to turn all your assets into a physical commodity you can pick up and take with you.

This means the inflation-hedging capability of gold relies heavily on the market’s perception of the relationship – this becomes a self-fulfilling prophecy which only holds so long as enough buyers/sellers believe.

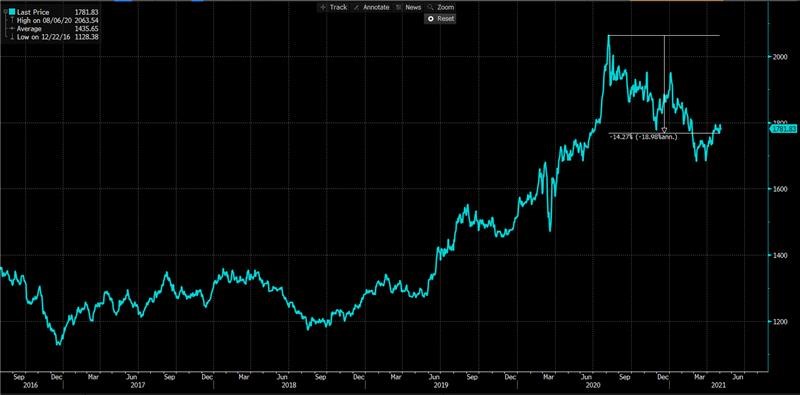

After reaching highs during the pandemic of 2020, gold is down just over 14% from its highs, with the fall cited as being a reaction to mass vaccination campaigns beginning and a lack of investor interest as traders turned to cryptocurrency as an alternative store of value.

Logically you would have assumed that as countries began printing money at record rates, this price should have rallied further – this illustrates the ability of short-term market dynamics to drive the price of gold, rather than historical relationships.

With that being said, there are ample opportunities to get exposure to gold if it fits your investment thesis and you have belief in its value – due to the size of the market and the spot nature of precious metals as commodities, ETFs are generally some of the best ways to gain pure-play exposure and liquidity:

- SPDR Gold Shares (GLD:NYSE)

- VanEck Gold Miners ETF (GDX:ASX)

- ETFS Physical Gold ETF (GOLD:ASX)

- iShares Gold Trust (IAU:NYSE)

Silver (Ag)

Silver sits in an interesting position of having a role in industrial applications, as well as being treated as a store of value as physical asset. This is common with the other “white metals” as well.

Silver is traditionally seen as a more volatile asset than gold due to it’s industrial use – as well as “what people think it’s worth”, it can also move depending on the fortunes of the various sectors in which it is used.

For instance, silver is used in batteries and semiconductors, so its price has moved with the global semiconductor shortage and rise of electric vehicles. If you believe that inflation will bring higher demand for electronics, then silver is a potential exposure for your portfolio.

There is a strong correlation in the price movements of gold and silver, as the two most popular ‘hoarding’ precious metals, but this does not always hold and there are multiple strategies exist in which traders arbitrage the price of silver to gold, expecting Ag to eventually follow Au.

In terms of investible opportunities, there are several large ETFs which seek to track the spot price of silver – perhaps barring SLV, after the WallStreetBets bull run:

- iShares Silver Trust (SLV:NYSE)

- ETFS Physical Silver ETF (ETPMAG:ASX)

- Aberdeen Standard Physical Silver Shares ETF (SIVR:NYSE)

Platinum (Pt) and Palladium (Pd)

According to the Journal of International Financial Markets, Institutions and Money, platinum and palladium are the two most reliable inflation hedges out of the precious metals asset class.

This inflation-hedging ability is expressed through short-term dynamics and is heavily linked to their rarity above the other metals, as well as their varied use in industrial products.

These products, the studies show, share linear relationships with inflation and therefore these metals should rise in value proportional to that of goods, protecting or even enhancing the real value of the asset.

Palladium is usually the most expensive precious metal per ounce (in USD).

Palladium tends to lack the speculative value of gold and silver due to its lesser known qualities and lack of involvement in everyday life – we see and feel gold and silver jewellery on a daily basis, but most people would struggle to identify what palladium actually looks like (it’s shiny).

Its primary uses are in medicine and chemical applications – its main use in the industrial space for the last few decades has been in catalytic converts to speed up chemical processes.

Platinum has been shown as a parallel to gold in the fact that it tends to rally in times of financial or political instability, however it has much higher ‘upside volatility’ due to its scarcity compared to gold.

Platinum is one of the most common materials used in reducing the toxicity of automotive emissions, as well as petroleum refining catalysts. It is tied to the auto industry and the price of underlying components of these products – as emissions standards become stricter on cars, this could become a tailwind for the price of platinum.

You do take significant geographic concentration risk in palladium since it is almost exclusively mined from regions in South Africa and Russia. This alone makes the price of Pt relatively volatile.

In terms of ETFs for these two metals:

- Aberdeen Standard Physical Platinum Shares ETF (PPLT:NYSE)

- Aberdeen Standard Physical Palladium Shares ETF (PALL:NYSE)

- ETFS Physical Platinum Securities ETF (ETPMPT:ASX)

- ETFS Physical Palladium Securities ETF (ETPMPD:ASX)

Golden Slumbers

As we touched on at the very start of this note, precious metals are not always the most direct inflation-hedge you can find, very often linked to speculation on what “people think it’s worth”.

However, they do offer an asymmetric exposure to your portfolio and look to reduce volatility from equity risk premia, particularly. Gold and silver offer a more sentiment-driven exposure, whilst palladium and platinum are more direct exposures to industry and the health of particular sectors.

Be aware of volatility and as always, all that glitters is not gold.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.