“For a piece of information to be desirable, it has to satisfy two criteria: it has to be important, and it has to be knowable.”

Quote attributed to Warren Buffett

As investors, the preservation of capital’s purchasing power is a sacrosanct duty.

At a minimum, we would want to grow capital in line with general price levels within the economy.

The reason?

That way we can always buy a constant amount of goods and services.

It’s for this reason that inflation is the number one enemy of an investor, as prices increasing faster than an investment’s return (inflation) causes an erosion of our capital’s purchasing power and we’re losing money – in real (ex-ante) terms.

It’s the reason we’re paying so much attention to inflation this year and the debate around whether the increase in prices is “transitory” or sustained.

Transitory is Ambiguous

Transitory is defined by the Oxford Dictionary as “not permanent”, which isn’t exactly helpful as central bankers that make monetary policy decisions affecting us tell us inflation is transitory.

So what?

The inflation is not permanent, sure, but will it spike for 3 months, 6 months, 18 months, 3-5 years?

All of the above are non-permanent time periods, but they would each elicit a different investor response.

For example, I’m less concerned about a 6-month aberrative spike in prices that is once-off and associated with the economic rebound from the pandemic, after a price decrease in 2020.

However, I should be concerned about inflation (as measured by CPI) increasing 6% in 2021, then 4% in 2022, and say 2.5% in 2023….that could potentially see an erosion of capital if not invested accordingly.

Monetary Policy Efficacy

The reason why central bankers tend to gloss over short-term anomalies is because these “disequilibrium” events tend to mean-revert over the medium term.

I’ll give an economic textbook example:

- There’s a cyclone that affects Queensland that sees whole crops destroyed

- The lower supply of produce causes prices to spike upwards

- The higher prices entice more people try to plant new crop, or more foreign-market growers to export to Australia to try and take advantage of the higher prices within our market

- This increases supply over the medium term, that sees prices fall back to “natural” levels

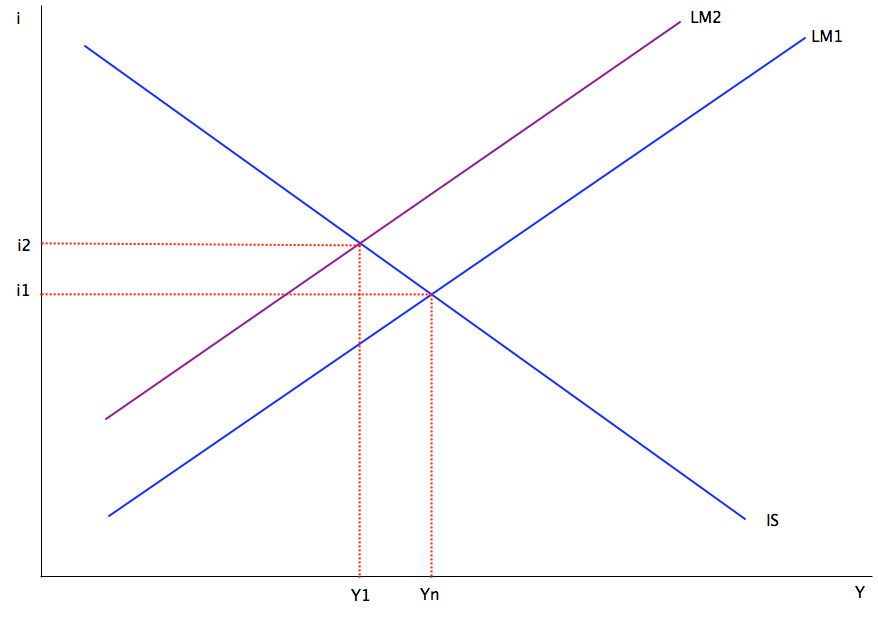

Graphically, we would see the price shift upwards and to the left, then revert back to its previous intersection. This is part of the IS-LM model that we touched on earlier this week.

Source: MNEconomics (2011). “Short and Medium Run Effects of Monetary Contraction”

This is where we’re currently at in regard to inflation, where we are discounting the possibility that this short-term spike in consumer prices will become a longer-term trend.

Inflation is Psychological

Milton Friedman famously said, “inflation is always and everywhere a monetary phenomenon”, which was a reference to the long run.

In all due respect to Mr Friedman, the quote hasn’t aged well because the macroeconomic assumptions regarding money supply = money demand don’t hold true in a world where massive money supply expansion (quantitative easing) doesn’t result in a flow of money from the banking system to the general economy.

Mathematically: Money supply > Money demand

The old Wall Street being out of touch with Main Street dilemma.

No, the main reason we’re not extrapolating current inflation to become future inflation is that inflation is always a psychological phenomenon where people believe prices are going higher, and they act in a way that prices move higher.

This will seem obvious to many of you, where if you perceive prices are moving higher, you’ll buy now at the lower price than the expected (higher) price.

We’ve seen this consistently in the Australian residential property market for the last decade, where the expectation of higher prices ensures we see higher prices.

This concept can be expressed in the following way, in what’s known as the Phillips Equation:

π = πe + (m + z) – αµ

Where:

π = current price

πe = expected (future) price

m = corporate profit

z = wages

µ = unemployment

From the equation, we can see the current prices are a function of expected (future) price levels + income, employment, and profit margins (“markup”).

Inflation in 2021

Here we are in Q3 2021, where global CPI has spiked higher and global wage growth remains low , and we aren’t seeing the wide-spread cries of anguish yet.

This is indicative of low-price expectations, where if prices were perceived and projected to continue at rates 3-5% p.a., there would be loud and vocal demand for higher wages and possibly price controls.

In fact, this is what happened in the 1960s and 70s when higher prices saw price controls put in place to little avail, before the Federal Reserve (under Volcker) aggressively hiked interest rates to squash inflation expectations.

PriceStats Inflation

I’m a fan of PriceStats inflation data, where the methodology of scraping millions of prices daily to measure prices is a robust measure of daily price movements, compounded over time.

This is in comparison to how most government statistics bureau’s measure inflation, through surveying retailers, supermarkets, department stores, and websites each quarter.

Using the government’s own explanation, “in total, the ABS collects around 100,000 prices each quarter”.

In comparison, PriceStats does 10x that EVERY SINGLE DAY, and updates their gauge with a three-day lag, as opposed to ABS CPI produced ~4 weeks after the end of the quarter.

For example, Q2 2021 CPI was released on 28-July 2021.

Whereas PriceStats Q2 inflation data was updated continuously during Q2, where 30-June data was accessible on 5-July.

For investors, that’s incredibly powerful as we can make real-time decisions.

Inflation Across the Globe

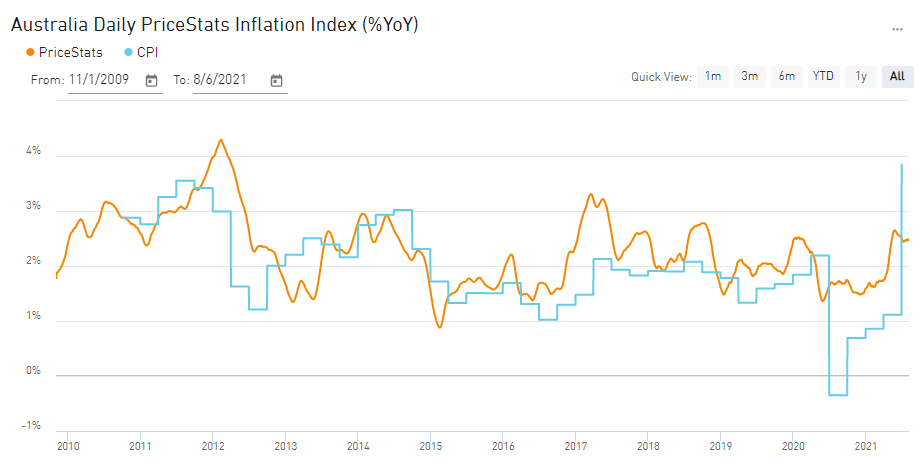

Looking at Australia, our ABS’ measure of CPI (blue line) dropped far too far in 2020, which has created a corresponding bounce far too large in 2021, bouncing off the low levels.

PriceStats on the other hand measures it current at ~2.5%, where it’s started to trend down slightly.

Source: PriceStats, State Street Global Markets Research

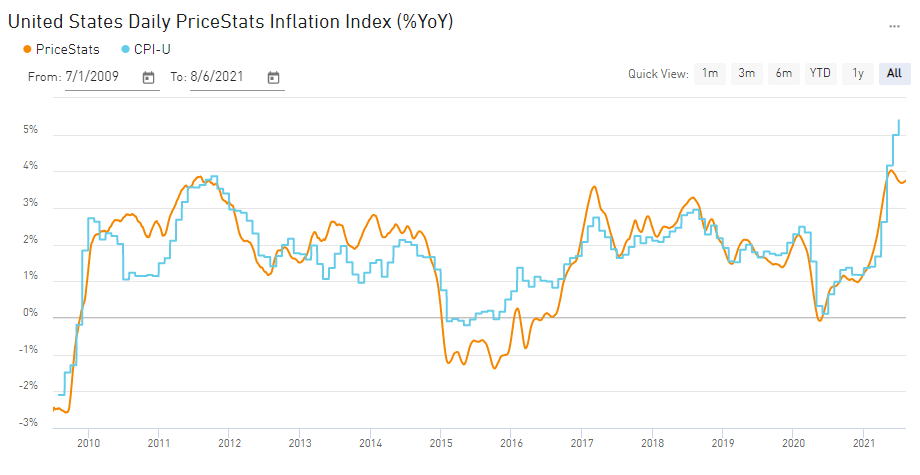

As for the USA, PriceStats is at ~3.7% versus their official at 4.99%, another large divergence.

Using the more up-to-date data from PriceStats, we can also see that prices have started to decline in the US over recent weeks. This aligns with the recent Non-farm Payrolls data, that showed over 1.2 million full time jobs were re-added to their economy, mostly across service sector workers, which should help ameliorate the supply-shortages causing the price increases.

Source: PriceStats, State Street Global Markets Research

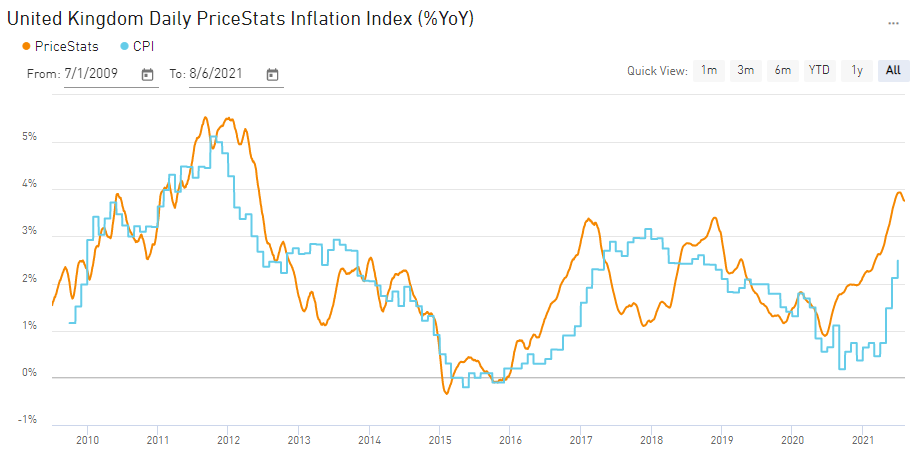

In the UK, in contrast, we see the rare global occurrence where PriceStats is highlighting much higher inflation than the UK official estimate measures, though is starting to catch-up.

This would likely be because the UK has quickly re-opened borders and their domestic economy, because supply-chains have had ability to re-establish themselves and re-stock inventory.

This has caused a spike in prices associated with economy reopening and “reflation”, that is yet to be seen in official data, due to its lagged nature.

Source: PriceStats, State Street Global Markets Research

Closing Remarks

Using countries and blocs such as the USA and UK as our proxies, we could surmise that inflation will move higher in Australia, as we eventually vaccinate a large portion of our population and lockdowns become less regular.

This would be likely a transitory spike – less than 18 months in duration – followed by a benign period of restocking and reinvestment as cash hoardings are slowly spent or invested.

As for the possibility of higher for longer inflation, it’s still too early to determine if the collective psyche (“animal spirits”) have decided; whether prices will remain “sticky” or be projected to keep increasing.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.