Yesterday I had the opportunity to speak at the Institute of Managed Accounts Professionals (IMAP) conference, held in Sydney.

First and foremost, I would like to thank IMAP for the opportunity to attend and speak to the large cohort of investors and financial advisors that attended, at the first in-person conference for quite some time.

For those interested, the conference was regarding “Portfolio Management in the New Normal”, focusing on asset allocation.

Specific to my own involvement, Jonathan Baird (Western Asset Management), Nigel Douglas (Douglas Funds Consulting) and I spoke regarding how central bank policy and geopolitical stresses have affected investment portfolios.

It’s All About Time Frame

The starting point for any investment thesis is to know objectives and time horizon so that portfolios can be constructed to align.

This sounds logical but you’d be surprised how different ideas, fads and speculative investments do not align with time horizons and objectives.

Because we tend to focus our attentions on short to medium term factors, we miss the forest for the trees so to speak, because this “noise” may not align with the underlying time horizon.

We’re talking about the structural factors driving portfolio returns, such as:

- Geopolitical imperatives

- Global labour supply

- Demographic trends

- Wage growth & household spending

- Inflation and borrowing costs (bond yields)

- Taxation

- Political stability

- Monetary velocity

This is not a definitive list, but through statistical back testing we can derive that these factors are the most influential over long-term asset returns [Turkington, Kritzman, Kinlaw (2017)].

Structural Factors

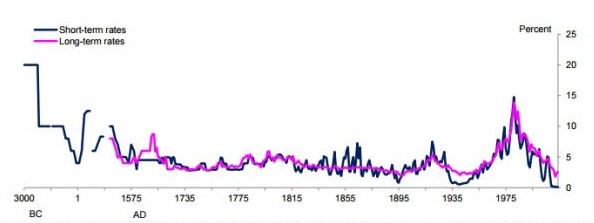

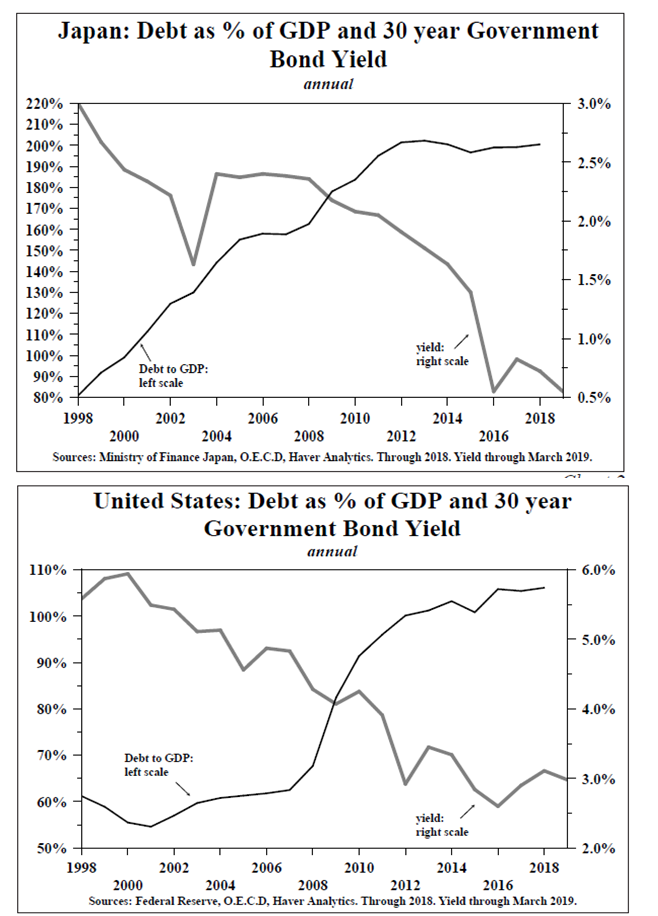

It is important to highlight that borrowing costs and inflation are at all-time lows, at levels not experienced at any prior point in history.

A History of Interest Rates by Sidney Homer provides this stunning graph of global interest rates over the last 5000 years. While this chart is now ~6 years old, bond yields are lower than back then which only highlights how different this point in history is compared to our past.

What this means is that the past does not provide context for what we’re experiencing, and this isn’t a cyclical aberration.

If you’re wondering why interest rates are at record lows, it’s not because of central banks.

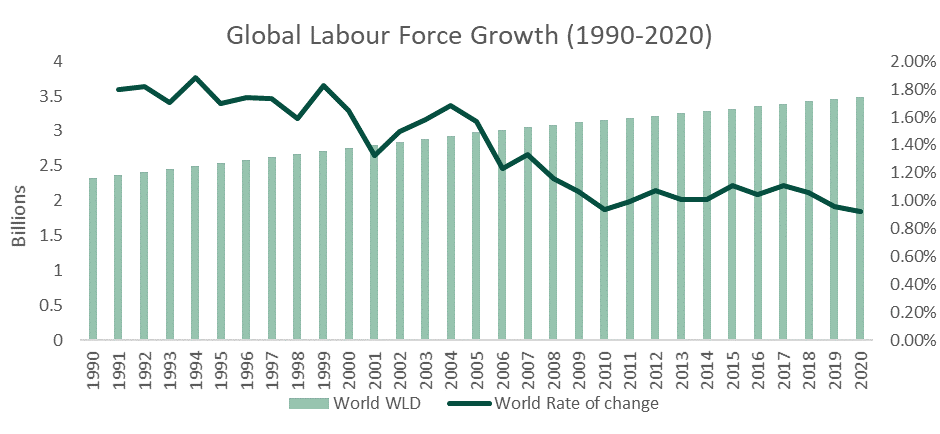

Central banks enacting ultra-low interest rate policy is a symptom reflecting long-term structural forces, such global labour supply.

If we think about it objectively, global central banks are mandated to achieve full employment.

Because of the influx of workers to the global labour market, it has become increasingly impossible to achieve this mandate by virtue of global labour being cheaper than domestic labour (i.e. think outsourcing to China or India vs. Australia, where Australia’s labour market is continually running below our potential.

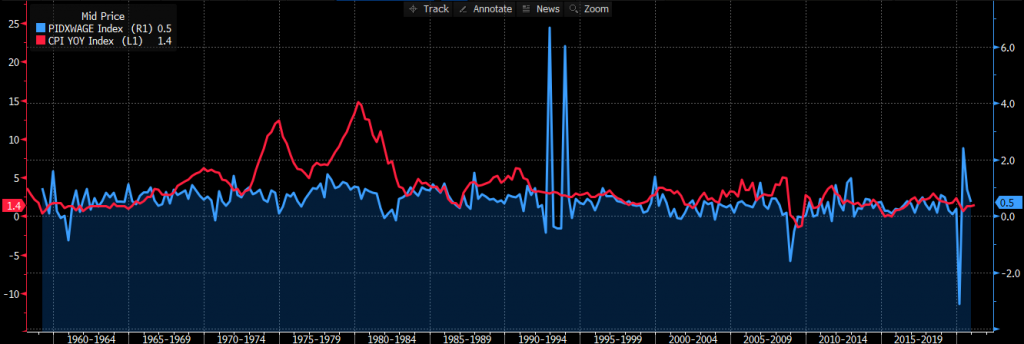

This deluge of new employees into the global labour supply has created a positive supply shock, whereby employee wages have grown at a rate lower (blue line) than price inflation of goods and services (CPI in red), a net decrease in household disposable income.

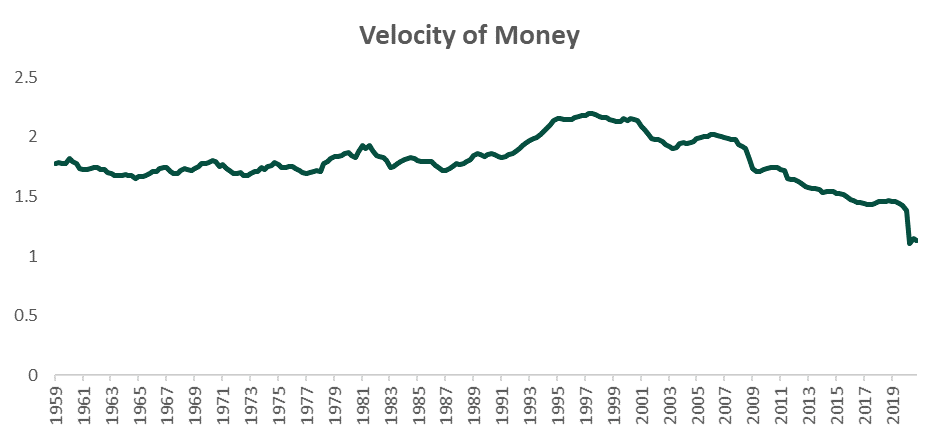

This lower than historical wage growth results in less money circulation, measured by velocity of money, where the demand for goods and services is depressed to historical growth, with less inflation likely to occur.

Geopolitical Elements

On the other hand, geopolitical imperatives are beginning to shift and may see an end to the above disinflationary/deflationary regime – or in specific industry areas.

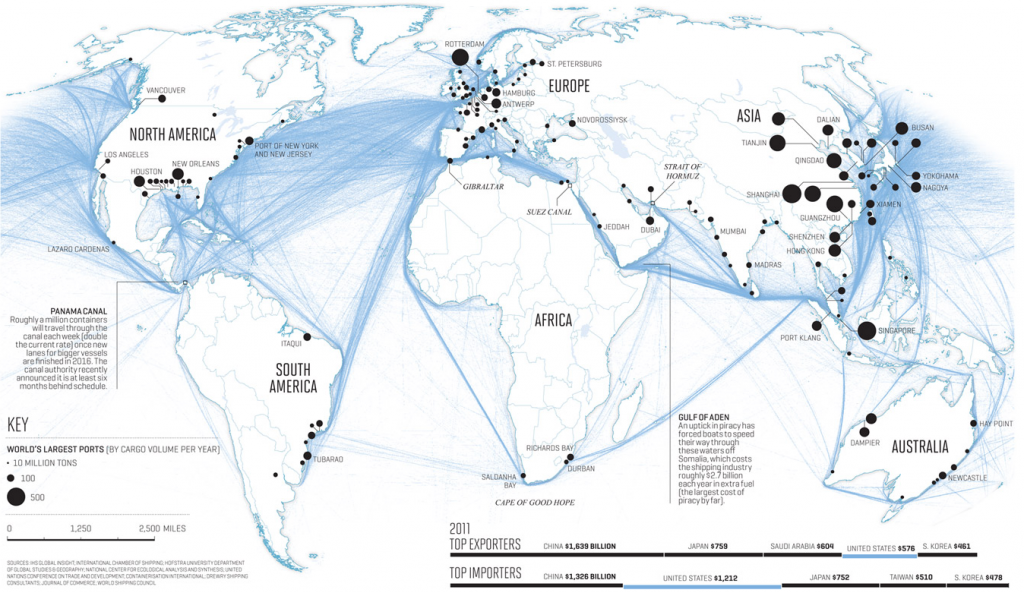

Australia is at the heart of this, as it has both benefitted and lost due to globalisation practices.

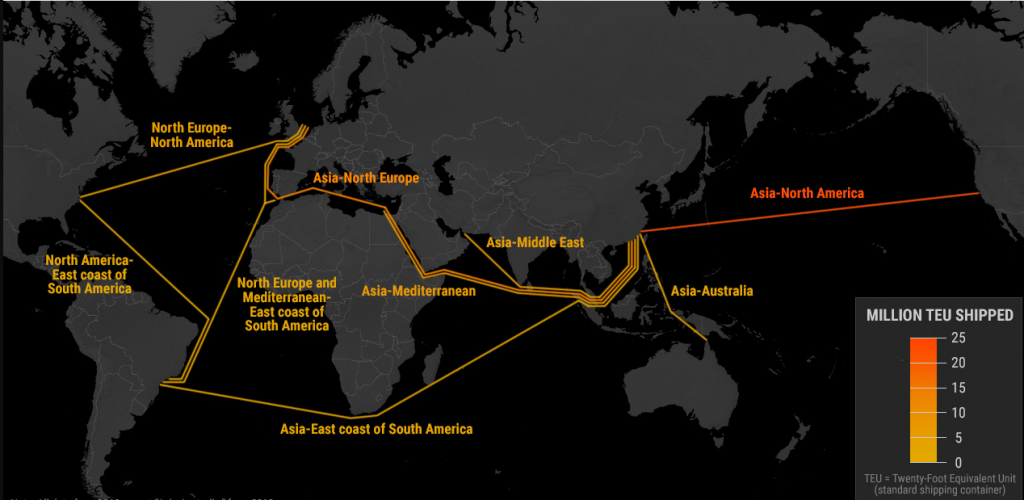

Post WWII, Australia has achieved broad access to global shipping routes through various alliances with the US, UK, Japan, India, New Zealand etc. to ensure regulated and fairly free access to oceans.

For us, one of the busiest routes is shipping cargo north from Australia into Southeast Asia, China, South Korea and Japan.

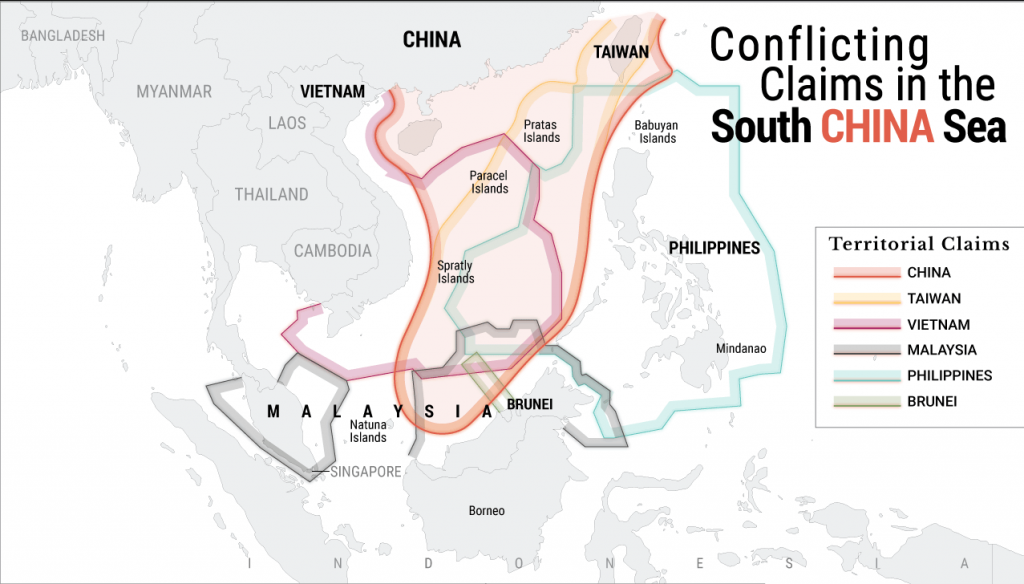

This route is slowly becoming less accessible as China asserts its territorial claims over the South China Sea, where many of the geographic locations are hotly contested by other nations.

This dynamic is worth being aware of as redistribution of supply chains away from China – a net exporter of labour supply – may see more inflationary impacts over the coming decade.

Cyclical Factors

Short- to medium-term factors play their part in influencing investment portfolios as well.

Examples of these include:

- COVID infection rates

- Fiscal policy and economic growth

- Economic mobility

- Interest rate differentials

- Supply chain logistics

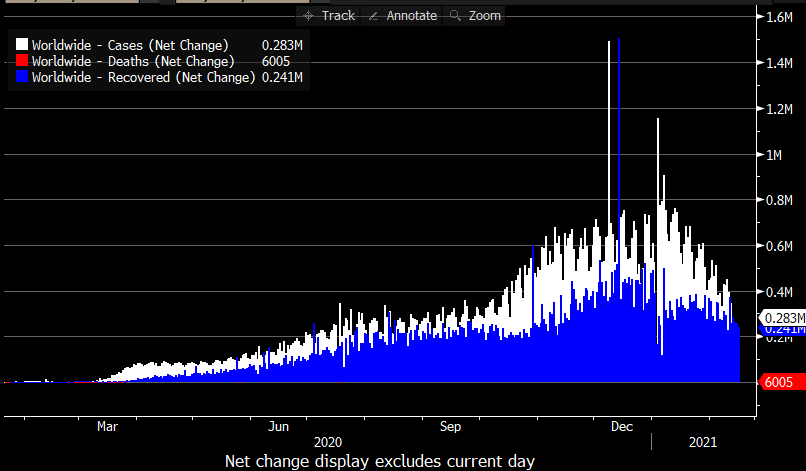

Of this, COVID-19 has to be the main focus over the last year, as infection rates informed risk-on versus risk-off binary investment decisions.

These infection rates are declining as mobility has been restricted both voluntarily and government imposed, and as vaccinations roll-out across the globe.

Globally, we have less than 300k new infections per day, well below the trend of ~600k in November and December last year.

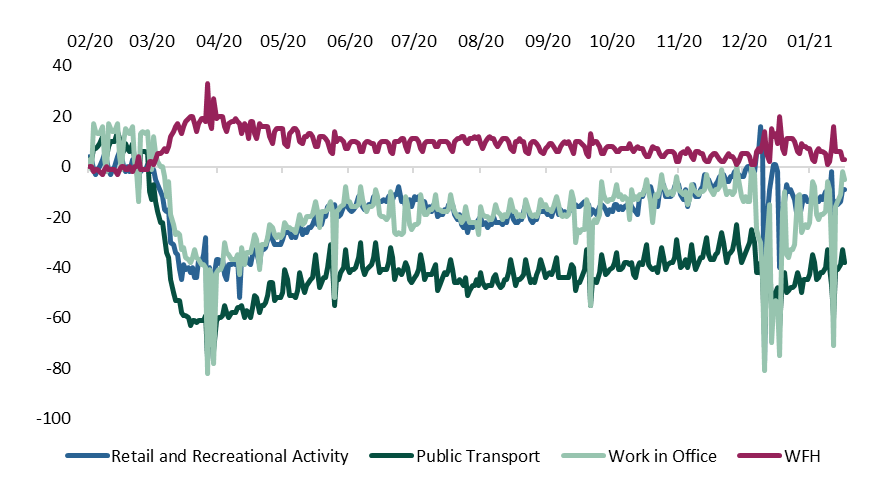

This is seeing higher consumer spending and customer mobility; which Google Trends tracks through user data. The following is our charting of the Australian data series, where we compare pre-COVID (Feb 2020) and the resulting trend of reduced mobility.

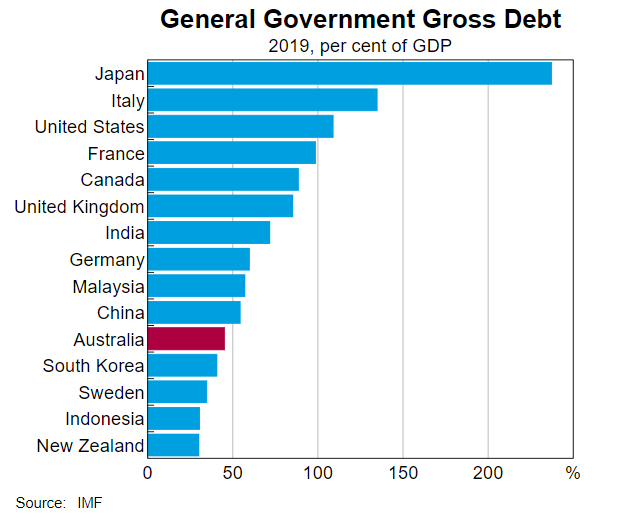

Having influence over our economic trajectory was the starting point for government debt.

Countries with lower debt to GDP ratios at the start of COVID-19, have had better opportunity to realise budget deficits to fund stimulus and relief programs, where those with the higher debt/GDP ratios are already exacerbated.

This high government indebtedness further anchors yields at low levels, where central banks can not increase cash rates and other interest rates to pre-COVID levels, lest the debt expenses detract from future economic expenditure.

Which brings us back to supply chains and geopolitics.

If central banks are hamstrung by high public indebtedness, they may be unable to contain inflationary pressures from the redistribution of global supply chains.

These supply chains centre on East Asia, where China, Taiwan, South Korea and Japan have become integral to global manufacturing of primary, secondary and tertiary goods.

Any further shift in global trade, away from the current globalisation trend, may well see inflation occur in specific goods and/or services, where manufacturing costs may be passed onto consumers, further detracting from household incomes with no wage increases in sight.

Closing Remarks

It is important to remember the primary drivers of investment performance, historically long-term structural factors such as political stability, taxation, borrowing costs, demographics, inflation etc.

Because these prime ordinances are occurring silently in the background, they remain out of focus, despite being critical in alignment of investor objectives and portfolio construction.

However, short-term cyclical factors will impact market timing, as well as play a larger role in market psychology over the short-term as starting points can dramatically alter end points.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.