For close to seventy years, fixed income – specifically bonds issued by sovereign nations – provided satisfactory levels of income, at relatively low levels of risk, that served as the ballast for diversified portfolios.

This rise in popularity was closely tied with Harry Markowitz’ work in “Modern Portfolio Theory”, a concept so novel that his doctoral advisor and renowned economist, Milton Friedman, argued should not be considered part of “economics”.

Portfolio Construction 101

In a recent note introducing our factor investment series, we published the guiding definition of an asset class we utilise:

“a stable aggregation of investable units that is internally homogeneous and externally heterogeneous, that when added to a portfolio raises its expected utility without the benefit of selection skill and can be accessed cost effectively in size.”

– Turkington, Kinlaw, Kritzman, (2017)

The pertinent part to today’s note is that we add assets to portfolios only when we expect the portfolio to have a higher utility with that asset included.

In essence, this means that we only add an asset if:

#1 it provides higher return without disproportionally increasing risk

#2 it provides lower perceived risk or volatility, without disproportionately reducing return

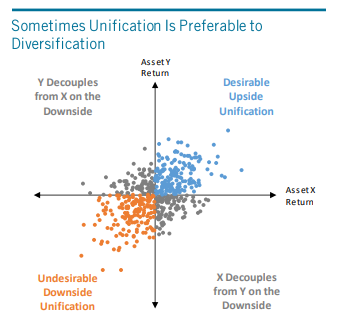

On March 29th, we wrote about strategies and techniques to try and achieve this, where we’re attempting to build portfolios that have desirable upside unification, but avoid undesirable downside unification.

Said otherwise, we want assets that are correlated when rallying, but diversified when markets sell off.

Role of Fixed Income

In terms of fixed income, I believe we’re all well aware that government bonds do not provide the levels of income that a large swathe of investors demand.

This was acceptable in past decades as the declining yield environment saw yields lower and bond prices higher. This allowed investors to still receive decent returns from bonds, though less and less of this was derived from income, and more from capital returns.

In turn, this increased the sensitivity of investment portfolios to capital price volatility (market risk), because a greater portion of the holdings were included based on perception of capital price performance, rather than passive paying income.

At present, this is the current yield of global 10-year government bonds (far right column):

Let’s be honest, buying 10y US Treasury bonds at 1.56% yield to maturity (YTM) or 10y Australian Commonwealth Government Bonds at 1.63% YTM doesn’t cut the mustard for a lot of investor’s portfolios anymore.

Moreover, the downside protection these bond prices exhibit is asymmetric, as there’s limited scope for yields in many of these nations to move materially lower.

Sure, our benchmark Australian 10y govie could rally and see the YTM decline towards 1%, which would see its capital price increase about 6% gross.

That is definitely plausible, but then there’d be a probable reality that the yield increases from there and the coupon remain low (as it is fixed at primary issuance of the bond).

In this case, the benchmark Australian 10y govie has a coupon of 1.0% p.a., where the YTM is 1.63% because the bond’s capital price is at a discount to par (about 93c to the dollar).

Either way, we’re evaluating a world where government bonds are providing less utility for portfolios, and investors are looking at alternatives.

Alternative Investments – Credit Bonds

The first solution that comes to mind is a solution that is similar to government bonds but provides higher income in return for less liquidity and more exposure to corporate profitability.

We’re talking about credit bonds, referring to bonds issued by corporates that provide a credit premium (higher yield) compared to government bonds because of lower liquidity and slightly higher default (credit) risk.

For example, we’ve established that we can buy a 10y govie at 1.63% YTM.

If I can buy a hypothetical Westpac issued 10y bond at 3.63% YTM, that would imply a 2% p.a. credit premium for buying a Westpac bond instead of a government issued bond.

This becomes a nuanced way to build a diversified portfolio as the underlying credit risk – the corporate default risk premium – has varying correlation with equity positions within the same portfolio.

To take our hypothetical slightly further, if we’re buying Westpac 10y corporate bonds AND we own Westpac equity (ASX: WBC), then we have a very similar risk profile.

There are also different types of corporate bonds, which we covered in greater detail in our note on 8 March.

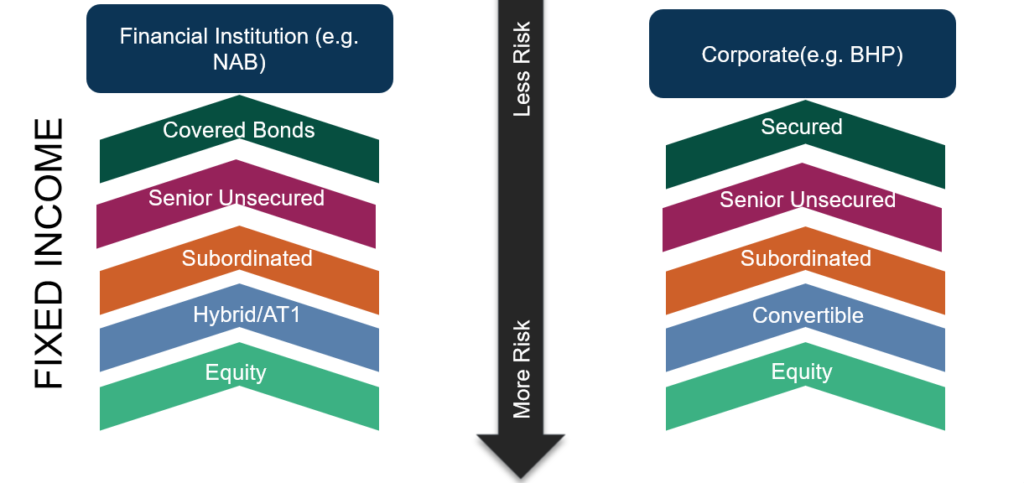

In particular, corporate bonds can have different coupon types paying floating rate, fixed rate or inflation-linked rates of interest, but can also have different “capital status” depending on the seniority (repayment ranking) of the debt within the corporate’s capital structure.

For example, a large corporate like Westpac can issue covered debt (AAA rated), senior debt (AA- rated), subordinated debt (BBB+ rated), junior subordinated debt (BBB- rated), and potentially more in-between.

For a number of years already, Australian investors have enjoyed the higher income associated with owning ASX-listed hybrid debt, such as CBAPD, ANZPF, WBCPI, BENPE etc, because of the perceived stability of the Australian financial system, and low chance these hybrids are required to be converted into equity.

If you are after more detail in regard to credit bond investments, please get in contact with your Mason Stevens representative, as we have an extensive global credit market footprint and suite of products available.

Alternative Investments – Private Credit

There may be opportunities in “private credit” markets as well.

This sub-category of credit investing is distinct from credit bonds as the investments aren’t tradeable in open markets, where there’s an associated illiquidity premium and also complexity premium in some cases, where additional expertise is required to gauge the risk and return of the private credit investment.

Examples of these are Metrics Credit Partners, La Trobe Financial or Moelis’s Secured Real Estate Income Fund.

Looking internationally, there are also avenues for private credit investment in US and European markets too.

Alternative Alternatives

Then there’s what I personally call alternative alternatives: these are hedge fund strategies that are almost asset class agnostic, that derive returns from trading assets based on manager skill, rather than risk premia associated with the underlying asset.

For example, Australian based investors have access to Ardea’s Real Outcome Fund, or Coolabah Capital’s Smarter Money Long-Short Credit Strategy.

In both cases, the funds seek to provide returns distinct from the underlying fixed income investments, taking advantage of market inefficiencies through statistical and regulatory arbitrage.

Regulatory arbitrage is rife within fixed income markets, where many of the large institutional buyers of bonds are regulated entities such as central banks with low price sensitivity, or large banks and insurers, who are required by law to buy a specific portion of government issued bonds.

This creates the opportunity for investors to continually receive complexity premia by navigating these market inefficiencies.

Closing Remarks

Looking to the future, it’s hard to suggest that government bond yields will meaningfully move higher, causing a spike in debt servicing costs, which would lead to lower corporate earnings and lower government spending.

Because of this, yields will remain anchored at low levels – maybe a little higher than present, but not by too much.

As such, alternatives will continue to grow in prominence and popularity as assets that provide additional expected utility to multi-asset portfolios, for years and even decades to come.

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.