Understanding the difference between risk and uncertainty is crucial in every aspect of investing. A decision involving risk lends itself to statistical analysis and econometrics, particularly if the opportunity or idea is common, and the event re-occurring.

On the other hand, an uncertain decision is when you do not have a good sense of the odds and pay-offs or are not able to calculate them.

What I am articulating is an investor’s distinction between speculation and gambling.

Basis risk

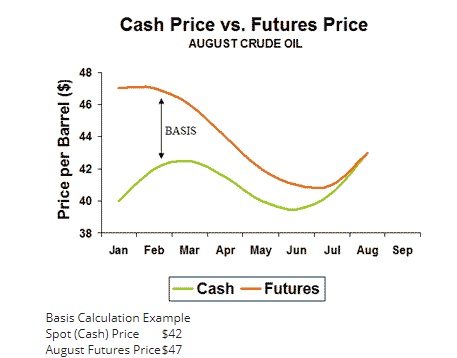

“Basis risk” is the risk that future price movements may not track the assumptions that we used to predict future price movements before.

This particular risk is a source of headaches for many corporations that seeks to hedge certain risk exposure that their business faces, only for their hedging instrument to inadequately insure them for the risk they wished to avoid.

For example, take a corporate treasurer who wished to hedge their exposure to oil price fluctuations as an input cost to their business.

If the current market price of oil is trading at $42/barrel, they may sell futures contracts to hedge their exposure. However, the futures contract (a financial derivative) is trading at $47/barrel, indicating a $5 difference (the basis risk).

What we can see from the below chart is that this basis risk does not hold constant. It does not hold constant in commodity markets, interest rates, equities etc. and corporate hedgers or speculators may be over-paying, under-paying or mis-evaluating their risks because of these changes in assumptions.

Source: Optionsguide.com

And this is just one made-up hypothetical.

The consequences are much greater when we talk about entire economic trajectories, labour forces, manufacturing industries, and the global service economy.

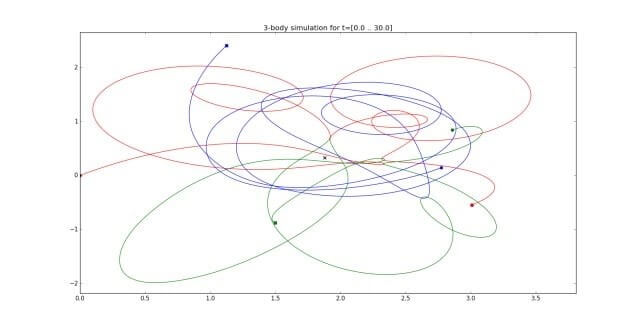

A Three Body Problem

A Three Body Problem is a famous example where a system or forecasting method has no statistical power to predict observable results (i.e. when there is mathematical answer to turn basis risk uncertainty into risk evaluation).

Imagine three massive objects in space, such as Earth, the Sun and our Earth’s moon. They are all in the same system and affected by each other’s gravity by various degrees and can’t escape each other’s gravitational pull. We can calculate their position, their mass, their speed and vector. We also know how gravity works, meaning we can perceive the force that is being impacted upon each of the three objects, and their affect upon each other.

In 1887, Henri Poincare proved that motion of celestial objects (bar a few special cases) is “non-repeating”. Meaning that in a closed-body system, the historical pattern of object positions has zero predictive power in forecasting where the objects will be in the future.

Source: Visual Basic

The next best thing

While no algorithm can define the future value of the three objects, we can use computers with an enormous amount of processing power to perform the calculations quick enough to predict where the objects will be one second from now, and then one second from then, and then another second after that, etc.

With enough processing power, you can calculate where these objects will be years into the future, even though it is impossible to solve for this outcome.

And this is how computing advances have revolutionised the statistical analysis and measurement of risk in investment management, by allowing what were once uncertain decisions to become risks that may be measured.

More than Three Body Problem

What we have right now is a multi-body problem. I do not believe a computer has the power to evaluate – nor humanity the knowledge to perceive – what the answers mean.

Our service industry has been decimated by social imposed and government-imposed lockdowns and it is uncertain when we will sociologically begin to normalise behaviours that may rekindle the services industry.

Meanwhile, central bank intervention has been the largest ever, and their ability to wind-back these current policies is uncertain.

Government “stimulus” or “life support” policies have increased disposable incomes around the globe, for portions of society with the highest measurable propensity to consume. While this income has been held as savings for now, there is an uncertain point in time where the savings may be invested or spent.

Furthermore, global trade issues are a more common occurrence, with tariffs being proposed in the middle of a recession – something that was done in the US that exacerbated the Great Depression (read: Smoot Hawley Act).

Global trade and “outsourcing” were contributory to the disinflationary environment of the last 30 years, where higher domestic wages were not a contributor to price increase as manufacturing was offshore. So even if no further tariffs are enacted, “protectionist” trade policies may see higher domestic inflation.

However, the “working class” or the bottom two quintiles of earners in developed economies will be the last to see any form of economic recovery. This is physical labour and primary industry that can’t “work from home” as tertiary industry can. These are people that are having to deal with no work, a possible “fiscal cliff” when government support ends whilst a slow protracted return from unemployment as the economic recovery will be slow and re-hiring uncertain.

And lastly, both entrepreneurs and technology will be transformational for economy after the crisis. Those with capital and entrepreneurial spirit will be able to build new business out of old, and possibly glean new industry that arises from this crisis that never existed before.

As well, technology is already transforming our lives with or without COVID-19. Elon Musk just launched and landed a massive rocket, a very visible sign of the technological advancements happening around the world. Quantum computing, virtual reality, cloud computing, AI, “internet of things”, blockchain etc all may change the way the way we conduct our daily lives.

And hey, maybe quantum computing may help compute these multi-body problems and help us assess future risks from uncertain events!

The views expressed in this article are the views of the stated author as at the date published and are subject to change based on markets and other conditions. Past performance is not a reliable indicator of future performance. Mason Stevens is only providing general advice in providing this information. You should consider this information, along with all your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.